Logica Capital commentary for the month ended May 2020, titled, “While The City Sleeps.”

Q1 2020 hedge fund letters, conferences and more

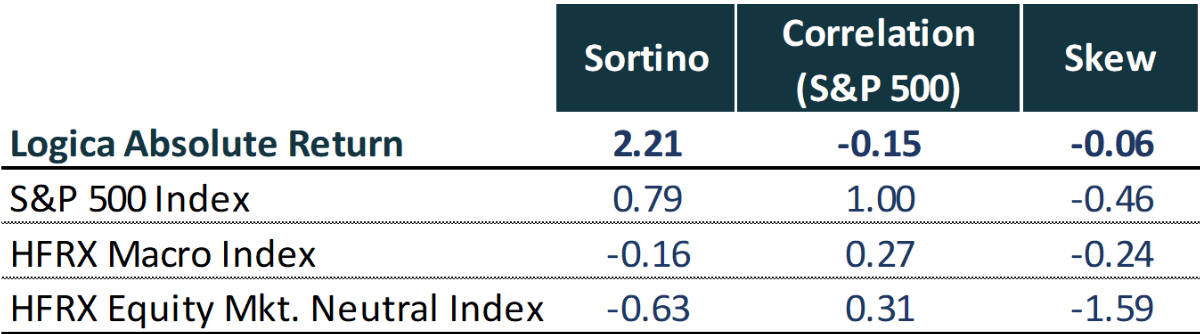

Logica Absolute Return – Up/Down Convexity – No Correlation

Logica Tail Risk – Max Downside Convexity – Negative Correlation

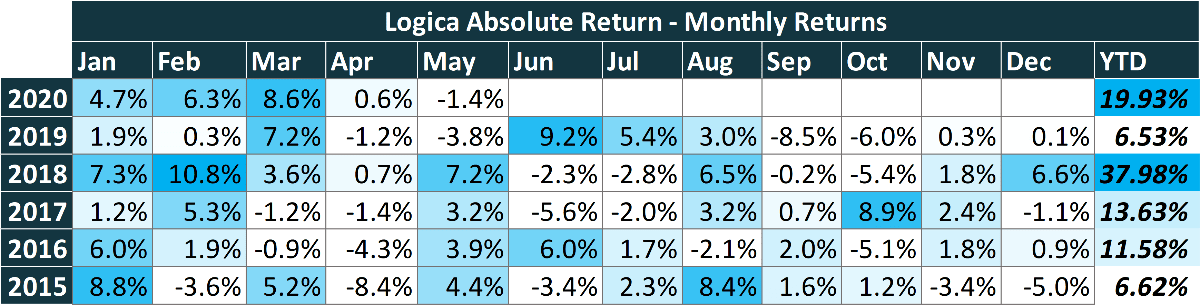

May 2020 Performance

- Logica Absolute Return -1.38%

- Logica Tail Risk -2.57%

- S&P 500 +4.76%

- VIX -6.64 pts

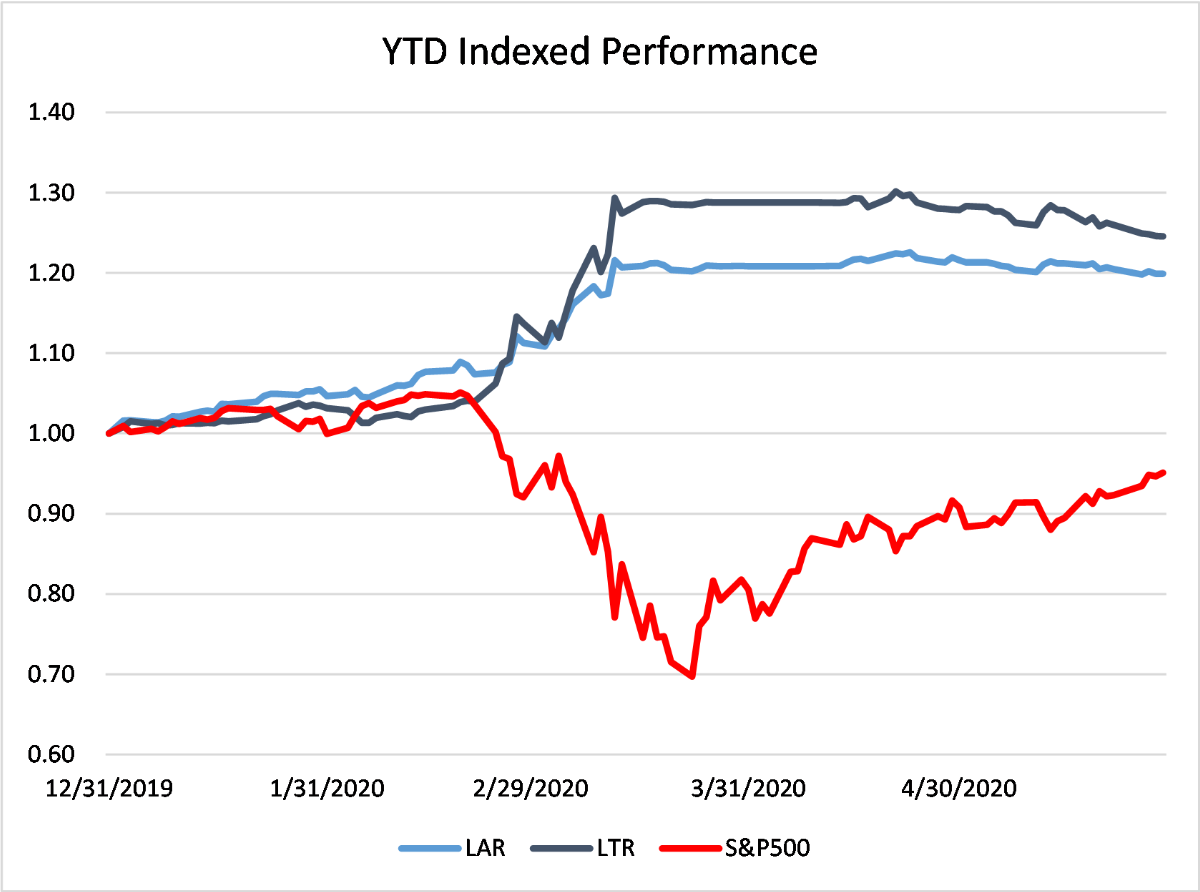

Year To Date Performance

- Logica Absolute Return +19.93%

- Logica Tail Risk +24.48%

- S&P 500 -5.45%

“I’ll have what she’s having…” – Estell Reiner, When Harry Met Sally (1989)

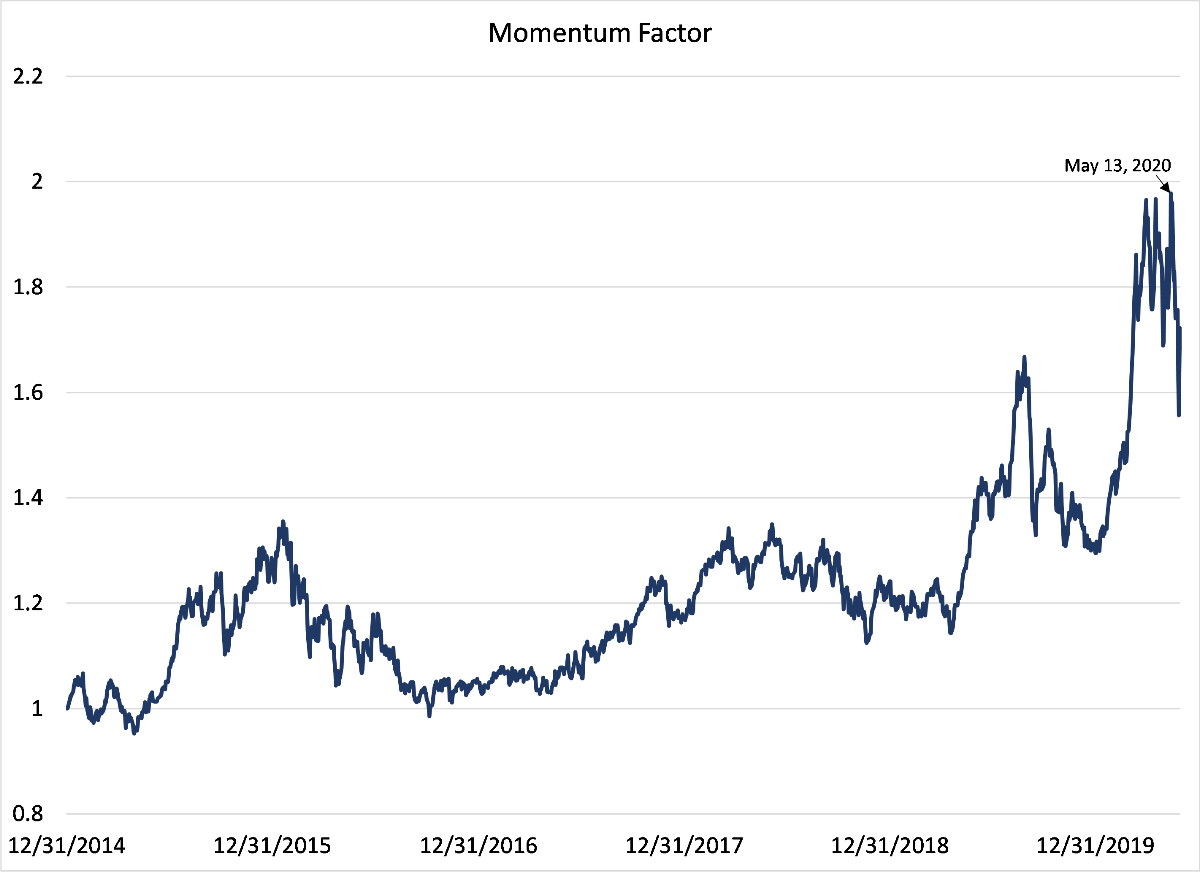

Momentum Reversal – Fake it Till You Make It

“Unfortunately, the volatility crush manifests itself as a headwind, but with a similar volatility crush impossible to replicate, we look forward to a more conducive environment in May.” – Logica April 2020

Well, that didn’t work so well. The month of May continued to add to the “interesting” developments in 2020 as we saw one of the strongest momentum reversals of the past decade.

From the May 13th peak in the momentum factor, we’ve seen a significant reversal with 12 month laggards up 20.4% in twelve trading sessions, while trailing winners were “only” up 4.8%. Annualizing to 4800% per year, this momentum reversal is only rivaled by the 20.9% gain in 15 sessions from August 27, 2019-September 16, 2019 as the US 10y-2y yield curve inversion reversed and the world jumped to the conclusion that the yield curve prediction of a recession in 2020 was clearly wrong. That didn’t work out so well in early 2020, but unfortunately many “rational” market participants are suffering intense pain as the market narrative of buying technology stocks that benefited from Shelter-in-Place while shorting consumer cyclicals and transports gave way to the day-trading armies of El Presidente, Dave Portnoy:

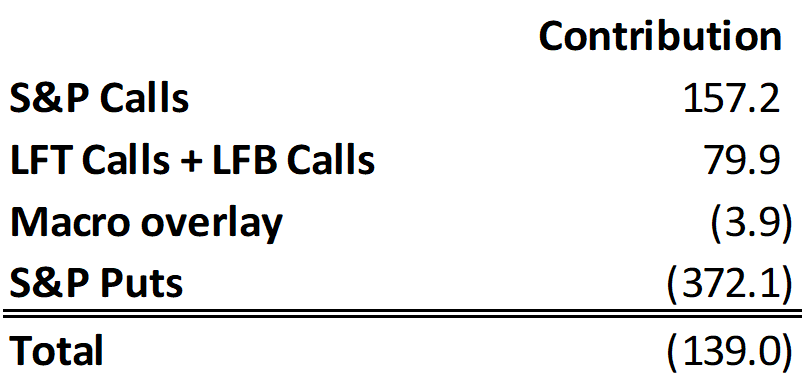

Unlike 2019, this momentum reversal has accelerated into the month of June, with the Momentum Shorts up a staggering 56.9% in eighteen days (5470% annualized). And with this fantastic recovery, broader market volatility has continued to compress further. While our long volatility positioning wasn’t able to completely overcome the headwind created by this still high and compressing volatility and a momentum reversal, for the month of May the performance of our newly introduced “anti-momentum” module (discussed in the April monthly letter and referred to internally as “LFB”) continued to save the day and keep losses contained. As a reminder, while long volatility, LAR will always contain both up-capture and down-capture exposure, mimicking a straddle payout. For the month, both our traditional up-capture module (“LFT”) and the more recently introduced LFB module contributed positively for the month alongside our S&P calls. On the negative side, modest losses in our macro overlay (largely rates) and, of course, long S&P puts were not the ideal instrument to own in such an upward accelerating market:

Because the Night

“Because the night belongs to lovers

Because the night belongs to lust”

– Because the Night, Patti Smith 1978

Unfortunately, the important charts in this section require a warning. For your own safety, we have placed the most dramatic ones on the next page. Be certain that you are sitting, have removed all beverages from your hands, and if you are in possession of a firearm, please make sure it is safely secured by a third party before turning the page.

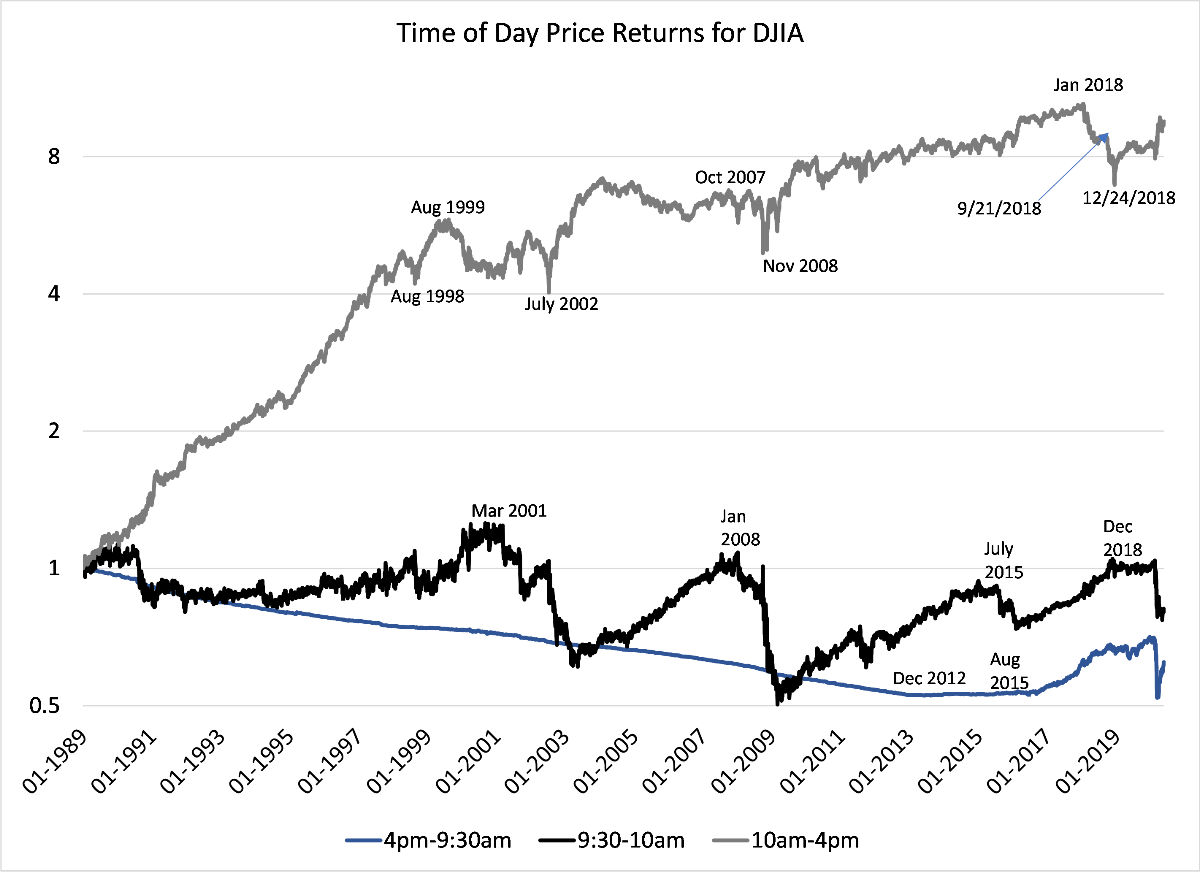

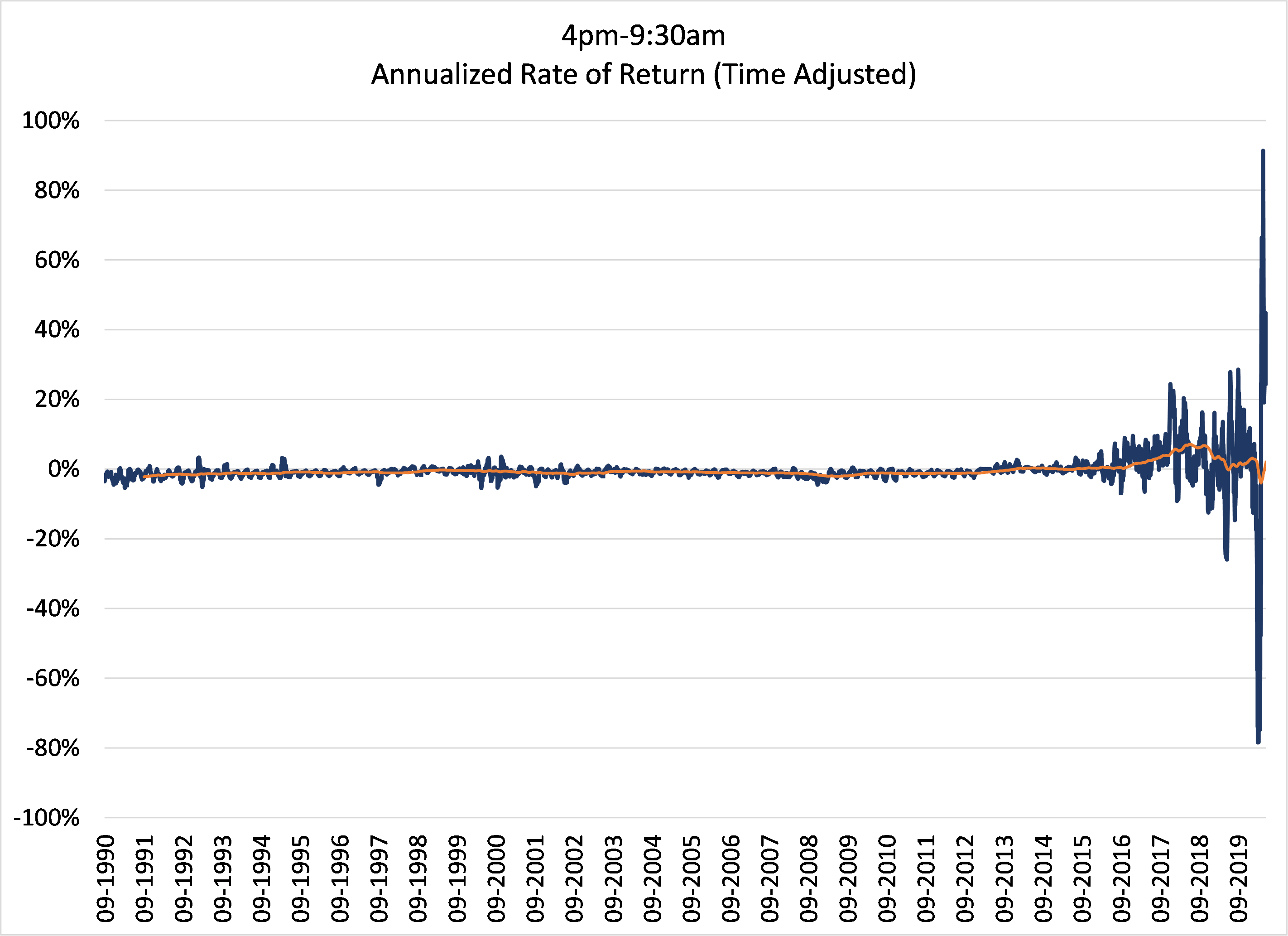

While we have discussed the momentum reversal and its impact on portfolios, the staggering reality is that this unprecedented move occurred almost exclusively in the overnight hours. While it is uncertain what is driving this phenomenon, since the middle of April we have seen the return of a pattern that began in 2015 and has not received enough attention – an unrelenting bid for US equities in the overnight session.

Historically, the overnight session was sleepy, with virtually no volatility. Negative price behavior was realized as stocks went ex-dividend after hours, resulting in dividend adjusted prices trading the next morning at lower levels. We can match the negative slope of the above blue line (overnight session) with dividend yield until roughly 2012 when the pattern began to change and overnight prices began to rise. This accelerated in Q4-2015, and during 2019 the majority of the gains occurred in the overnight session. Conversely, in 2020 (through April 7th) 100% of the net losses occurred in the overnight session. Since then, returning to the prior trend, 100% of the gains have occurred overnight. This increase in volatility is not just seen clearly, it’s screaming at us. Somebody is awake in the middle of the night and buying US equities:

While tempting to call out conspiracy theories of Central Bank manipulation (BoJ, SNB, ECB, Fed, BoC… take your pick), there appears to be a simpler explanation. Following the Chinese devaluation in Q3-2015, outflows from Asia have accelerated. Courtesy of Simon Ogus at DSGAsia, we can see this acceleration matches up with the changed behavior of US indices. The form of these outflows is uncertain, but it appears they are associated with structured product issuance. If true, the credit market disruption in March and April would explain the sudden stop in support from this market and subsequent reemergence. While we have reached out to sell side brokerage firms for comments, insights from our investor base are welcome.

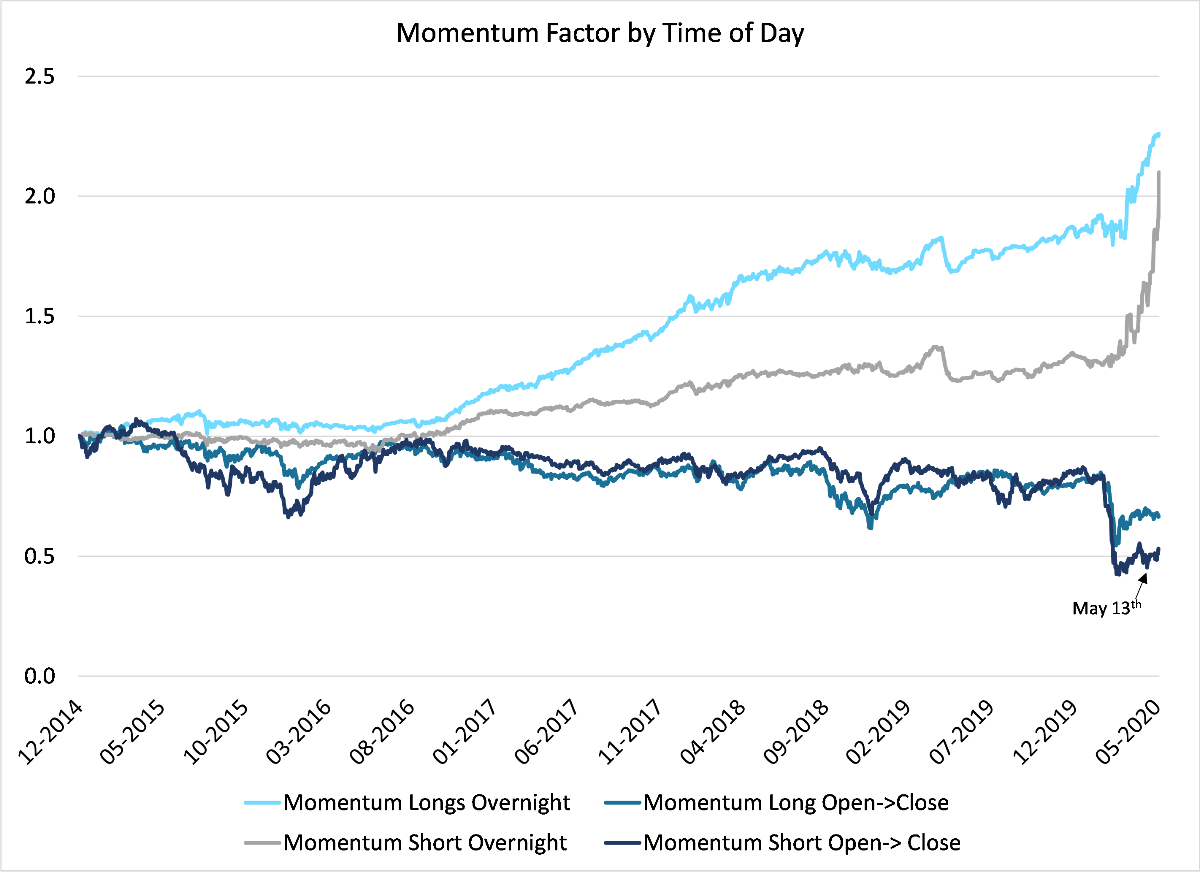

While the emergence of overnight volatility has been well telegraphed, it is in the momentum reversal that it takes its greatest form. Looking at the Morgan Stanley Momentum indices, long and short, and separating their returns into time of day generates one of the most exponential charts we have ever seen. In the overnight session, the Momentum Shorts (gray line) are up a staggering 63% since March 9th (the day US 10 year bonds hit the record low of 31bps) after languishing for nearly 5 years. Since May 13th (the beginning of the momentum reversal), overnight strength has been joined by intraday short-covering as hedge funds run for the hills.

Paycheck Protection Program

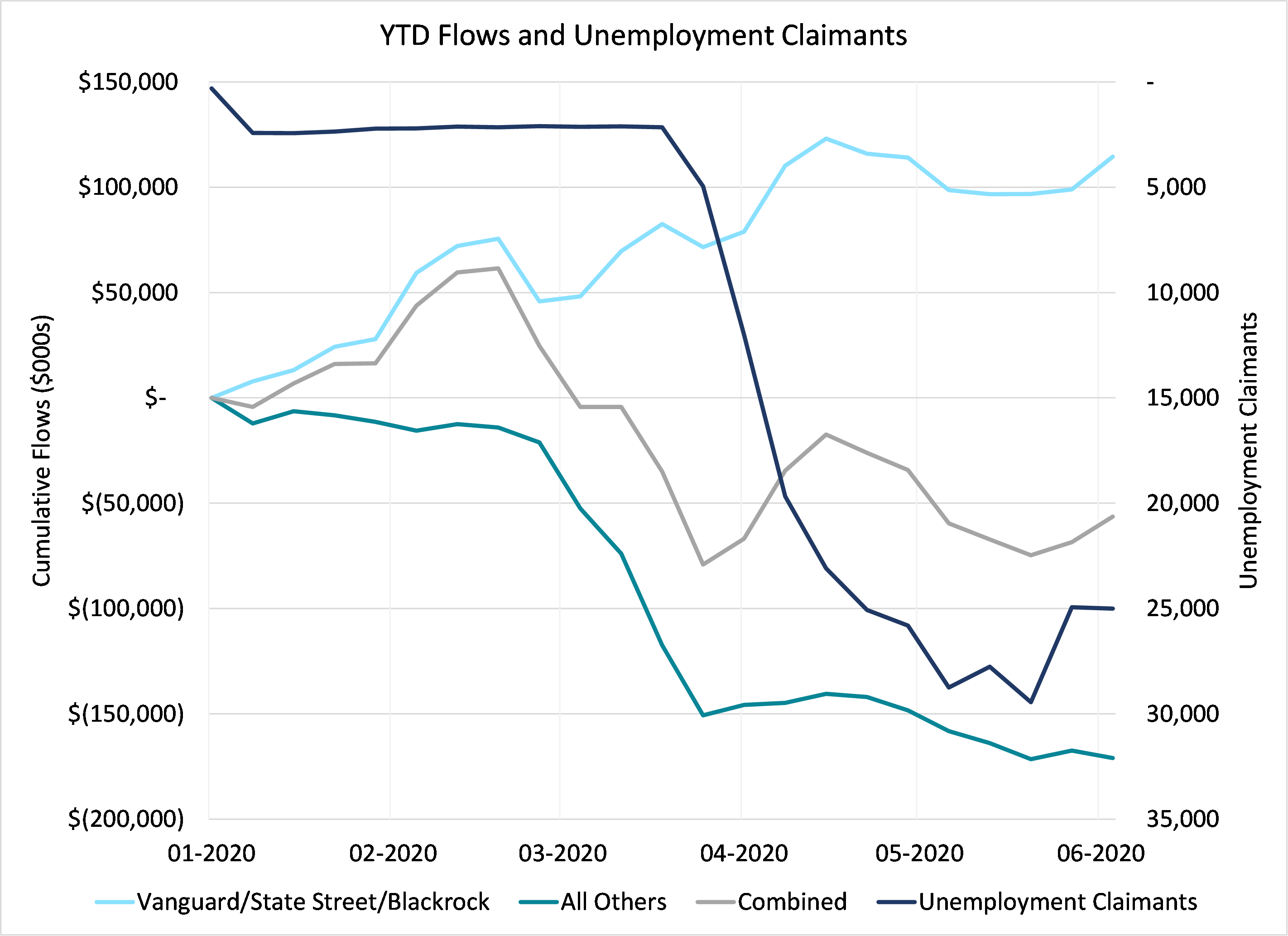

As we highlighted in our Pandemics piece, no one knows anything in an environment as volatile as we are currently experiencing. Reported in early June, the May payroll surprised dramatically to the topside and the June 4th release of investment fund flows revealed that the flows again turned positive with passive investment vehicles benefiting most. There were clues that this was occurring as PPP made rehiring and payroll maintenance a critical source of business cash flow; retail participation has also accelerated alongside short covering. These reversals were critical to sustaining the equity rally in late May. As discussed in our March letter, the inflows into passive vehicles are expected to continue for demographic and regulatory reasons, but came into question with the significant employment losses and widespread withdrawal of corporate 401K matching programs. It seems our concerns have been temporarily put on hold due to PPP. Whether the temporary support will be enough to offset eventual business shutdowns remains to be seen.

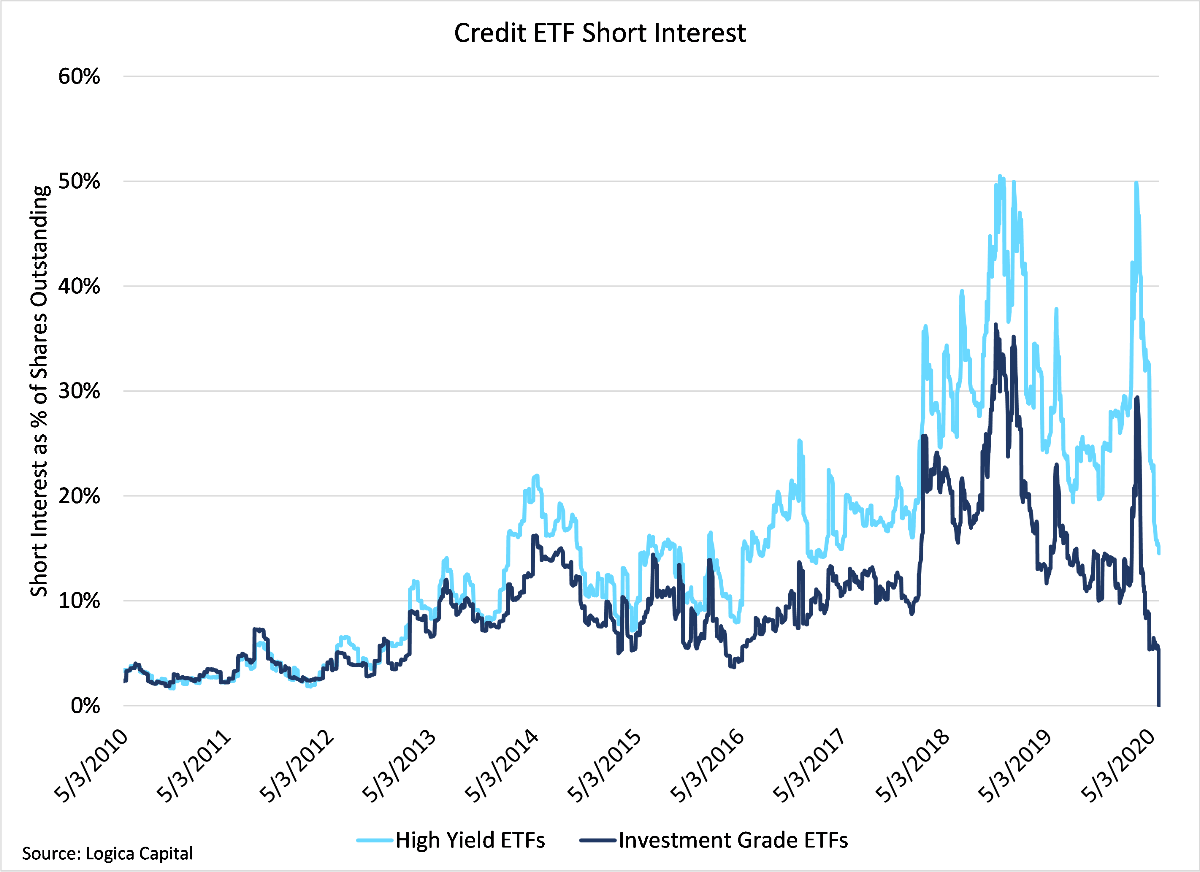

As in the equity markets, fears of Fed support for credit products has led to a wholesale collapse of short interest in Credit ETFs. Despite virtually no actual buying from the Fed so far, the fear of intervention has driven high yield credit markets (adjusted for defaults) to levels approaching the record peaks in early 2020. The rally in credit positively affected our portfolio through LFB (anti-momentum) as distressed equities rallied, but detracted via modestly negative macro contributions in our rates positions and declines in value of our S&P puts.

While we are always disappointed with a negative return, our focus is first on loss prevention and we would not strip our portfolio of downside protection. Given the extraordinary recovery outcomes in markets we are quite pleased that we have been able to hold the vast majority of our YTD gains while still accumulating a sizeable straddle position that should leave us positioned for gains from a sustained move in either direction. As always, we believe luck favors the prepared portfolio.

Action seems to follow feeling, but really action and feeling go together; and by regulating the action, which is under the more direct control of the will, we can indirectly regulate the feeling, which is not.

Thus the sovereign voluntary path to cheerfulness, if our spontaneous cheerfulness be lost, is to sit up cheerfully, to look round cheerfully, and to act and speak as if cheerfulness were already there. If such conduct does not make you soon feel cheerful, nothing else on that occasion can. So to feel brave, act as if we were brave, use all our will to that end, and a courage-fit will very likely replace the fit of fear.

— William James, “The Gospel of Relaxation”, On Vital Reserves (1922)

Business Update – Logica Absolute Return Fund Launch

Our next subscription date is July 1st, 2020. Please contact Steven Greenblatt if interested in receiving subscription documents.

The charts in this monthly letter are only a summary of our thoughts. We have spoken with a few institutional investors about the implications of overnight trading and momentum reversals and how these events are likely to impact portfolios. If you are interested in expanded views on these macro events, please reach out to Steven Greenblatt who will arrange a time to connect via phone/Skype/Zoom.

Wayne and Michael had the chance to discuss markets and approach on RealVision. To watch the joint appearance, please follow the link: https://rvtv.io/2yVZ0sb

Logica Strategy Details

Note: We have comprehensive statistics and metrics available for our strategies, but only include a select few to highlight what we believe is our most valuable contribution to any larger portfolio.

- If you would like to learn more about our strategies, please reach out to Steven Greenblatt.

- If you would like to speak with Wayne or Mike on their views on Hedge Funds/Investing/Trading and trends they see shaping the industry, please contact Steven Greenblatt at greenblatt@logicafunds.com or 424-652-9520.

Follow Wayne on Twitter @WayneHimelsein

Follow Michael on Twitter @ProfPlum99

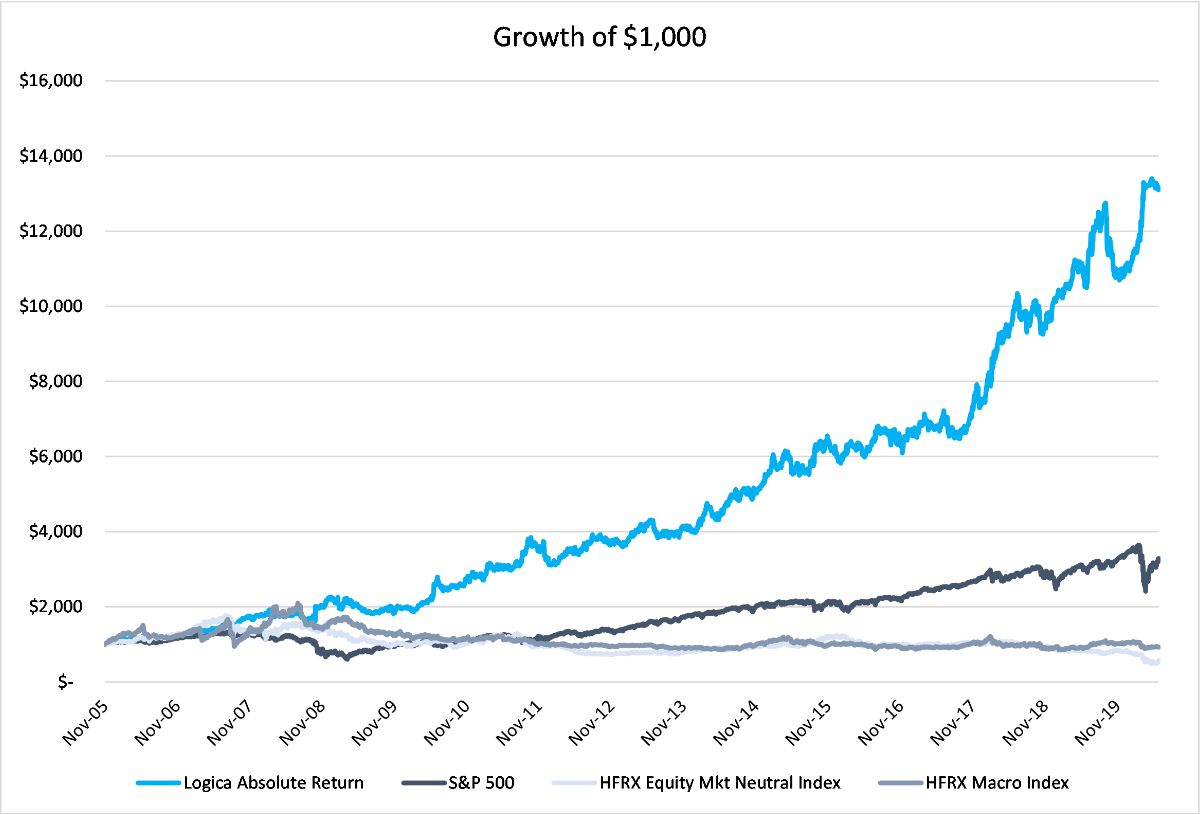

Logica Absolute Return

2015-2019 stats & grid, reconstitution of live sub-strategies

2005 to present growth of $1000 chart, simulation

Jan 2020 live with partner capital

The post Logica Capital May 2020 Commentary: While The City Sleeps appeared first on ValueWalk.