Tenth District manufacturing activity continued to decline, but not as sharply compared to last month’s record low. Expectations for future activity rose, but remained slightly negative. Month-over-month price indexes remained negative again in May. Moving forward, District firms expected prices for finished goods to decline and prices for raw materials to increase in the next six months.

The month-over-month composite index was -19 in May, up somewhat from the record low of -30 in April, and similar to -17 in March

emphasis added

This was the last of the regional Fed surveys for May.

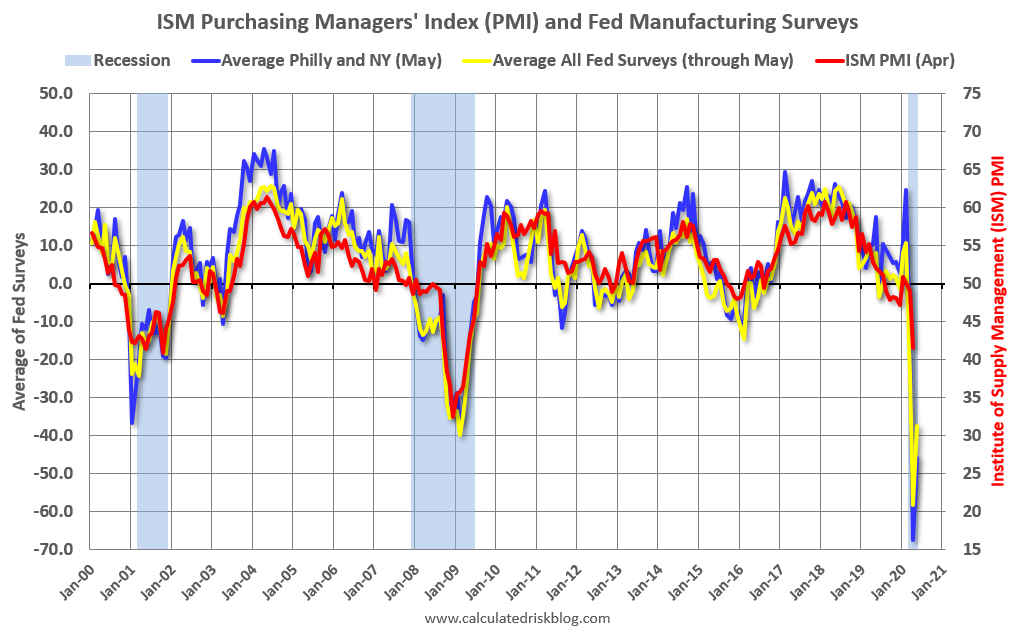

Here is a graph comparing the regional Fed surveys and the ISM manufacturing index:

Click on graph for larger image.

Click on graph for larger image.

The New York and Philly Fed surveys are averaged together (yellow, through May), and five Fed surveys are averaged (blue, through May) including New York, Philly, Richmond, Dallas and Kansas City. The Institute for Supply Management (ISM) PMI (red) is through April (right axis).

The ISM manufacturing index for May will be released on Monday, June 1st. The consensus is for the ISM to increase to 42.5, up from 41.5 in April. Based on these regional surveys, the ISM manufacturing index might even be lower than the consensus in May.