Whitney Tilson’s email to investors warning to beware of Moderna and reports of value‘s death may be greatly exaggerated.

Q1 2020 hedge fund letters, conferences and more

Beware Of Moderna

1) Only two months after stocks experienced their sharpest decline in history, they’ve ripped higher. So it’s no surprise that pockets of foolishness are emerging… which my team and I are tracking so we can warn you about things to avoid.

In that spirit, I asked Empire Financial Research Senior Analyst Steve Culbertson to identify some stocks that appear to have soared far above what their fundamentals justify (to be clear, these are not short recommendations). Here’s the first of a series that I’ll be sharing:

Moderna Inc (NASDAQ:MRNA)

Investors have gotten excited about companies developing treatments for COVID-19. Moderna is a high-profile candidate for a vaccine based on its mRNA technology. But many years ago, SARS taught us that coronaviruses, which mutate quickly, pose unique challenges to vaccine developers. What’s more, Moderna faces stiff competition in its pursuit.

Its stock skyrocketed after the company released news of supposed positive results in its Phase I trial. But careful reading showed a limited study with real concerns. Worse, we learned that insiders began selling a lot of stock after it popped.

The only way Moderna can justify its sky-high valuation, exceeding $22 billion, is if it creates a very large and profitable business – perhaps one that rivals GlaxoSmithKline’s (GSK) vaccine division. We think that’s highly unlikely. Shares are down 34% since peaking on May 18, but they could go much lower. Don’t jump in to catch this falling knife.

Value Investing’s Death Exaggerated

2) Following up on Friday’s e-mail about how cheap small-cap value stocks have become, here’s another study showing that, based on one measure of price-to-book ratio, value stocks are the cheapest relative to growth stocks that they’ve ever been, going back to 1963: Reports of Value’s Death May Be Greatly Exaggerated. Excerpt:

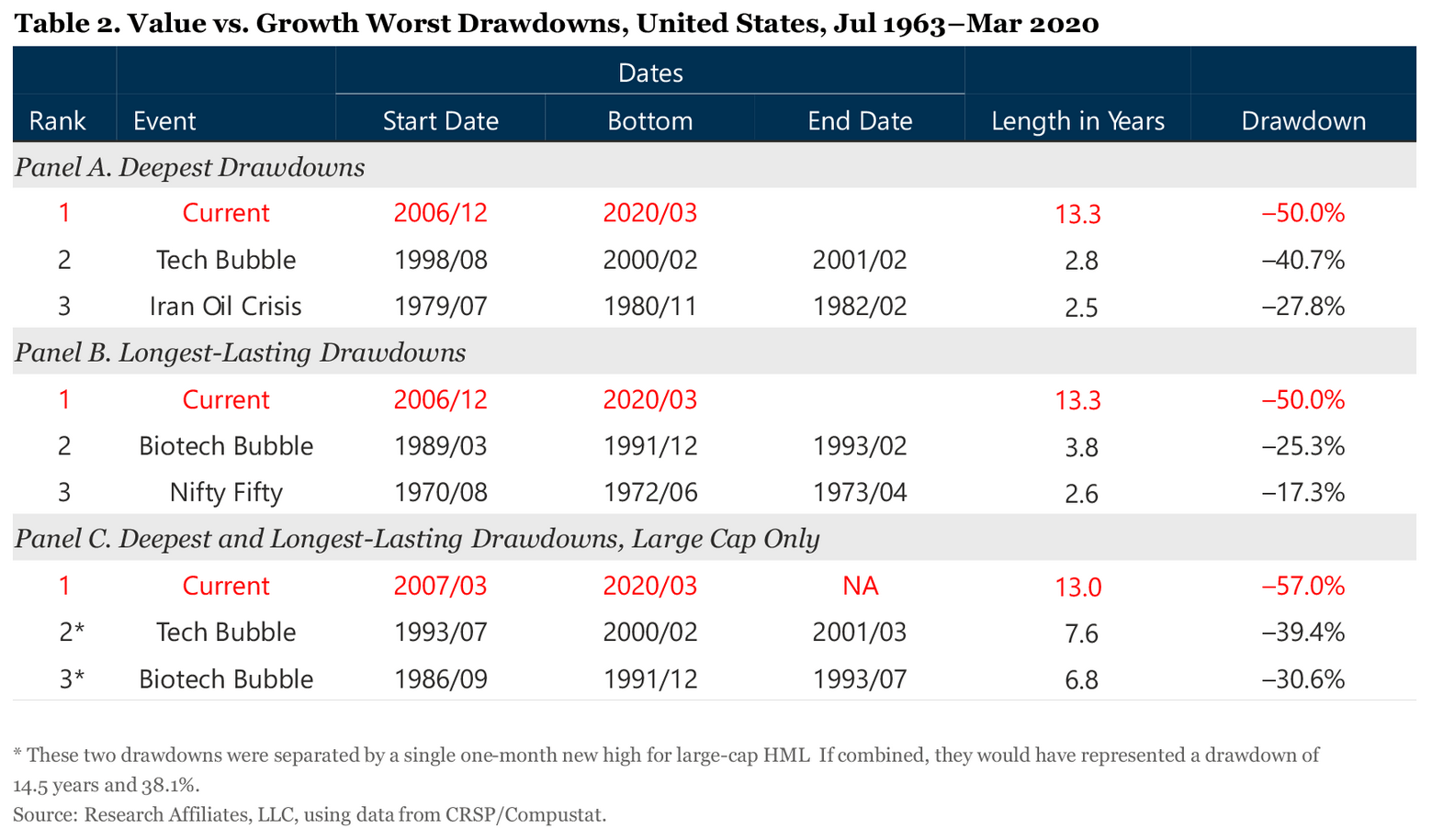

- Value investing has underperformed relative to growth investing over the last 13.3 years. The authors examine several popular narratives to explain this relative underperformance, including technological revolution, crowded trade, low interest rates, growth of private markets, and traditional measures of value that ignore internally generated intangible assets. These narratives purport to explain why “this time may be different” and why value’s poor relative performance may be the “new normal.”

- The authors demonstrate that the primary driver of value’s underperformance post-2007 was growth stocks getting more expensive relative to value stocks.

- The authors explore whether book value is the right denominator for value. In today’s economy, intangible investments play a crucial role yet are ignored in book value calculations. They show that a measure of value calculated with capitalized intangibles outperforms the traditional price-to-book measure, particularly post-1990.

- With today’s value vs. growth valuation gap at an extreme (the 100th percentile of historical relative valuations), the stage is set for potentially historic outperformance of value relative to growth over the coming decade.

This table from the study shows that the current 13.3 years of value underperforming growth is both the longest and deepest such period in history:

The post Beware Of Moderna; Value Investing’s Death Exaggerated appeared first on ValueWalk.