There are trillions of dollars of loan and derivatives contracts tied to The London Interbank Offered Rate (LIBOR), which is scheduled to be phased out by the Bank of England in 2021. As capital market participants evaluate their LIBOR exposure and search for an alternative, here is a primer on AMERIBOR, its advantages over LIBOR and other benchmarks, and AMERIBOR’s methodology.

Q1 2020 hedge fund letters, conferences and more

Background

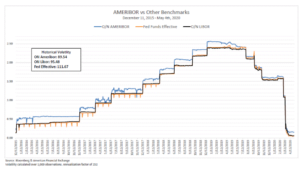

AMERIBOR is an interest rate benchmark created by the American Financial Exchange. AMERIBOR is an interest rate benchmark that reflects the actual unsecured borrowing costs of over 1,000 American banks and financial institutions.

LIBOR is currently the dominant benchmark for determining interest payments on adjustable rate financial products. The Federal Reserve Bank created the Secured Overnight Financing Rate (SOFR) as one alternative benchmark. It is a broad measure of the cost of borrowing cash overnight collateralized by Treasury securities.[1]

If a bank does not own U.S. Treasury securities, they are more likely to use AMERIBOR benchmark to fund their balance sheets. It is a separate and distinct benchmark that reflects their actual borrowing costs.

The American Financial Exchange

The American Financial Exchange (AFX) is self-regulated exchange founded in 2015. With more than 185 members across the 50 U.S. states, AFX seeks to offer a suite of innovative products to improve transparency and efficiency in the current interbank loans marketplace. AFX also facilitates the determination of a market-based interest rate benchmark, AMERIBOR. AMERIBOR reflects the actual unsecured borrowing costs of more than 1,100 American banks and financial institutions. In addition, AFX’s AMERIBOR is in alignment with all nineteen Principles set forth by the International Organization of Securities Commission (IOSCO) for Financial Benchmarks.

Competitive Advantages of AMERIBOR®

- Market driven benchmark interest rate

- Stable reference benchmark interest rate

- Calculated based on executed transactions with time-stamped transaction ID numbers

- Contains a credit spread component based on unsecured loans in contrast to SOFR which is based on secured (i.e. collateralized) loans

- Facilitates loan origination at spreads to a benchmark that represents actual funding costs for many American financial institutions

- Optimizes asset-liability management; matches asset pricing & liability costs to a single benchmark

- Adheres to IOSCO’s 19 Principles for Financial Benchmarks; reviewed and audited by an independent third party

AMERIBOR Methodology

AMERIBOR is calculated as the transaction volume weighted average interest rate of the daily transactions in the AMERIBOR overnight unsecured loan market on the AFX. AMERIBOR is an interest rate expressed on an Actual/360 Day Count and Following Business Day convention that is rounded to the fifth decimal place. AMERIBOR is calculated after the close of trading on the AFX and is published nightly by Cboe under ticker symbol AMBOR. The AMERIBOR overnight unsecured loan transaction data underlying the AMERIBOR interest rate benchmark is published in real-time on www.ameribor.net and is available through subscription.

In the event of market disruption including but not limited to insufficient or absence of data inputs, market stress or disruption, failure of critical infrastructure or Acts of God that prevent an orderly and smoothly functioning market, the prior day’s closing AMERIBOR rate will be published as the closing AMERIBOR interest rate.

The Committee for Benchmark Oversight is defined in the AFX Rulebook (Section 2.4.2) and is responsible for providing independent oversight of the AMERIBOR interest rate benchmark and calculation methodology. AFX also solicits feedback from stakeholders. Proposed changes to the AMERIBOR Methodology are reviewed by the Committee on Benchmark Oversight. Proposed changes that have been approved by the Committee on Benchmark Oversight are tested in advance of dissemination and best efforts are made to provide advance notice of such approved changes at least 30-days prior to implementation. In the event the Committee for Benchmark Oversight should decide to cease calculation and dissemination of the AMERIBOR interest rate benchmark due to market, data input or other factors, the Committee on Benchmark Oversight will make best efforts to publish such intent to AMERIBOR interest rate benchmark stakeholders at least ninety (90) days in advance of the planned cessation of publication and dissemination in order to provide stakeholders with adequate time to settle or unwind positions that reference the AMERIBOR interest rate benchmark.

Conclusions

Market innovation after Libor will spur additional products and choices. We are already seeing that with the CME One-Month SOFR (“SR1”) futures and Three-Month SOFR (“SR3”) futures which debuted a year ago. More recently, Cboe Global Markets, Inc. (Cboe: CBOE) launched futures on the AMERIBOR interest rate benchmark on Cboe Futures ExchangeSM (CFE). We will launch AMERIBOR® interest rates in June 2020.

One lesson that economics teaches is that it’s better to have a choice. And choice, in this instance, will have tangible benefits. Because banks can select among multiple benchmarks, they may be able to borrow funds at lower rates or lend at higher rates. All market participants will benefit from increased transparency, as benchmarks reflect financing activity in real time. The lending markets after LIBOR will be less monolithic, but that will lead to more market efficiency, not less.

AMERIBOR® is a registered trademark of the American Financial Exchange, LLC

[1] https://apps.newyorkfed.org/markets/autorates/SOFR

The post Understanding AMERIBOR: An American Interest Rate Benchmark appeared first on ValueWalk.