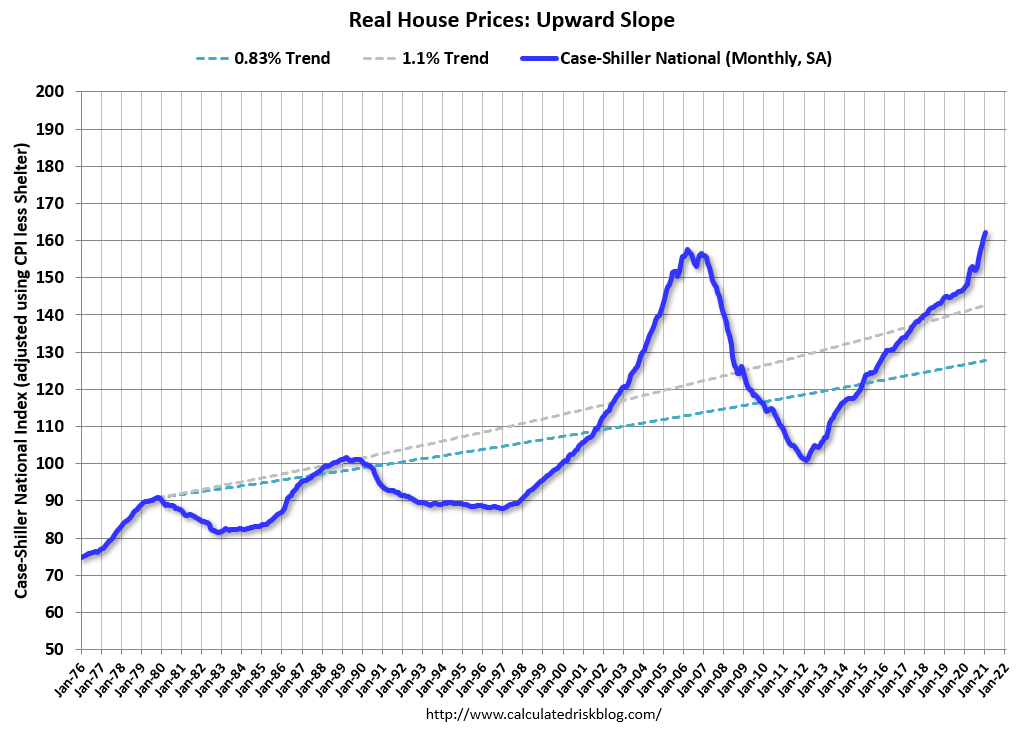

In 2012, housing economist Tom Lawler dug through some data and calculated that real prices increased 0.83% per year (See: Lawler: On the upward trend in Real House Prices)

Click on graph for larger image.

Click on graph for larger image.

This graph shows there have been four surges in real prices since the early ’70s. One in the late ’70s, one in the late ’80s, the housing bubble, and the current surge in prices.

It is important to note that nationally nominal house prices did not decline following the surges in the ’70s and ’80s. However, there were regional declines.

Since homeowners are concerned about nominal prices (not real prices), I wasn’t concerned in December 2018, when Professor Shiller wrote in the NY Times: The Housing Boom Is Already Gigantic. How Long Can It Last?

During the housing bubble, the difference between a slight upward slope in real prices (0.2% per year according to Shiller’s index) and a slightly larger increase in real prices using other indexes (probably between 1% and 1.5% per year) didn’t make any difference; there was obviously a huge bubble in house prices. But when comparing price “booms” over time, there is a huge difference.

If we use 1.5% per year for real price increases, the current “boom” in prices would be the fourth largest since the 1970s (and only about half the size of the late ’70s and late ’80s price boom), and if we use a 1.0% real increase, the current “boom” is on the same order as the late ’70s and ’80s price booms.

No big deal, and definitely not a “gigantic” boom in house prices.

Since I wrote that post in 2018, house prices have increased 16% nationally (from November 2018 to January 2021) according to the Case-Shiller index. Prices in Phoenix are up 25%, and in Seattle and San Diego, up about 20% since that Shiller article was written.

Now, I’d argue house prices are too high based on historical real prices. Prices are also too high based on price-to-rent measures, and price-to-income.

I wouldn’t call this a “bubble” because of the lack of both speculation and loose lending (see: Is there a New Housing Bubble?). But I am becoming concerned about fundamentals:

Maybe prices are too high based on fundamentals (due to extremely low supply and record low mortgage rates), but there is very little evidence of speculation (not like the loose lending of the housing bubble).

…

The lack of wild speculation doesn’t mean house prices can’t decline, but it means that we won’t see cascading declines in prices like what happened when the housing bubble burst.

…

We might see some price declines, especially in some 2nd home areas that saw a surge in demand at the onset of the pandemic, but the recent buyers are all well qualified, and some price declines will not lead to forced selling. So there is no threat to the financial system with widespread defaults.