MDCA Partners Inc (NASDAQ:MDCA) memo for the month of January 2020, discussing MDCA’s proposed merger with The Stagwell Group LLC.

Q4 2020 hedge fund letters, conferences and more

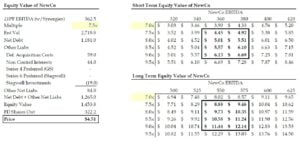

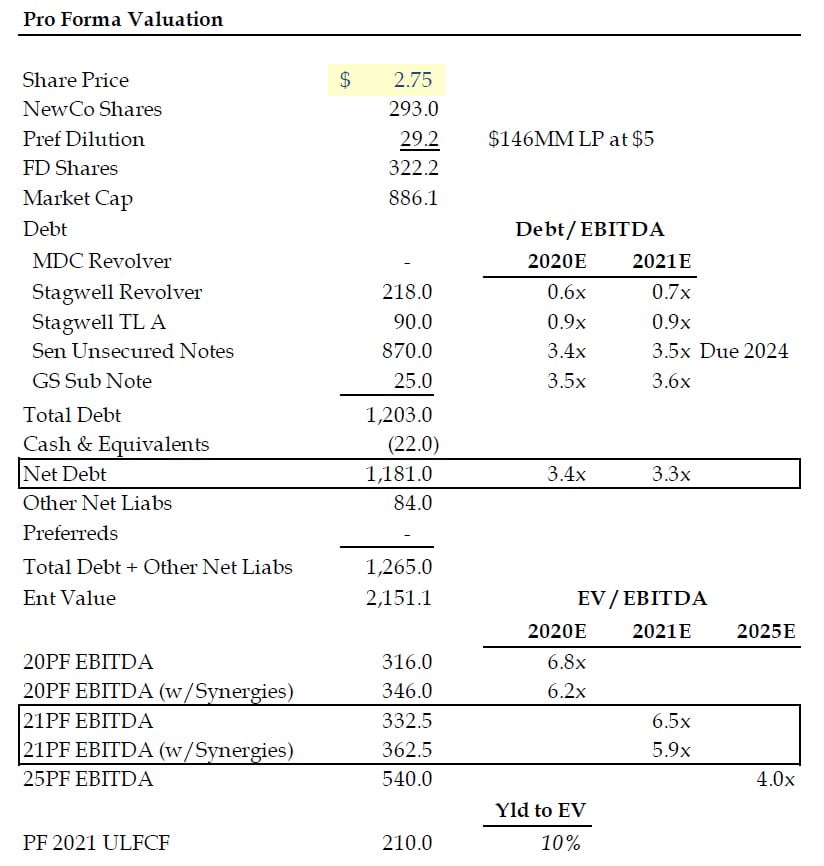

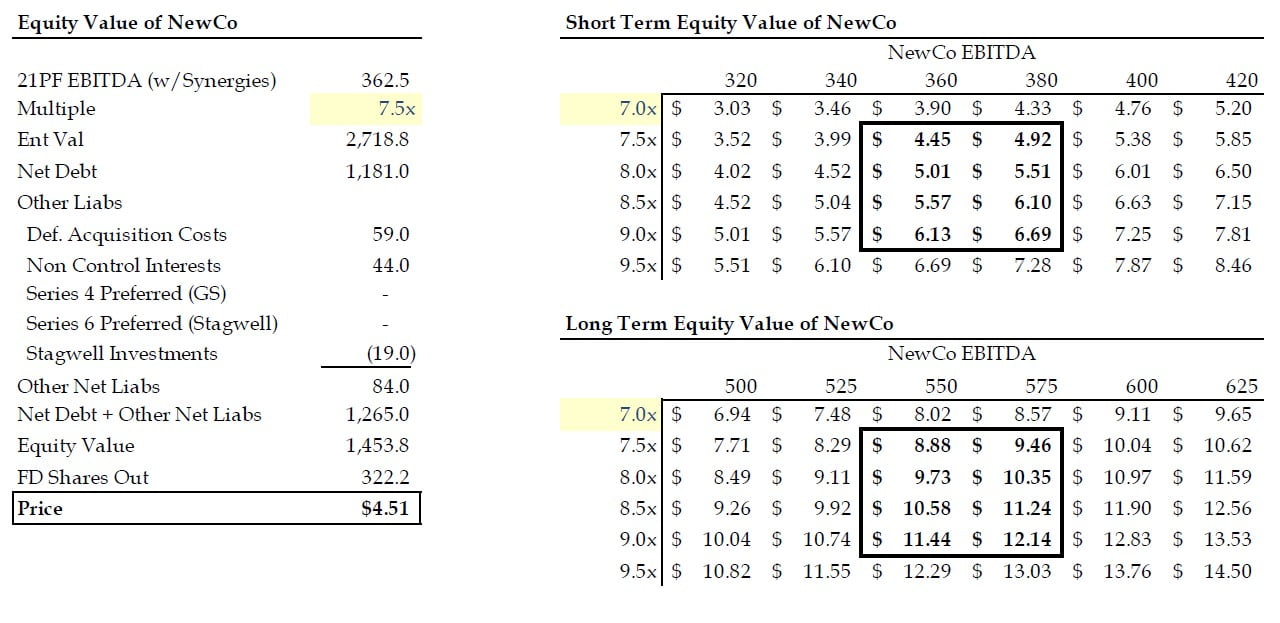

Price: $2.75

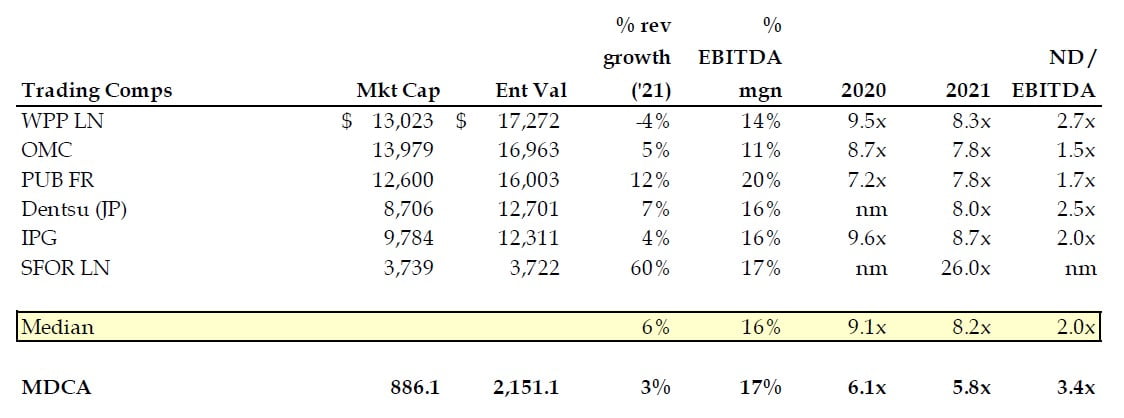

Mkt Cap: $ 866 MM

Ent Val: $ 2,151 MM

EV / Rev: 1.0x LTM and 1.0 fwd.

EV / EBITDA: 6.1x LTM, 5.8x fwd (incl synergies)

Price Target: $4.50-$5 (short term), $8-10+ (longer term)

MDCA’s Merger With Stagwell: Situation Analysis

MDCA Partners Inc. (“MDCA” or the “Company”) has been written up in the past which provides some good background of the Company. This write up focuses on the proposed merger of MDCA with The Stagwell Group LLC (“Stagwell”), a digitally focused holding company of marketing companies which also was the largest owner of MDCA shares prior to the proposed combination. Both Stagwell and MDCA are both run by Mark Penn, an experienced and accomplished marketing executive and former EVP of Advertising and Strategy at Microsoft.

MDCA is a marketing and communications holding company with several well-known global and domestic advertising and marketing properties. Stagwell was borne out of an anchor investment from Steve Ballmer who Penn worked with while he was EVP of Marketing at Strategy at Microsoft. In 2020, 42% of Stagwell revenue came from high growth digital transformation and marketing assets.

In early 2019, Penn made a $100MM investment in MDCA through Stagwell and assumed the role of CEO. Since his tenure as CEO of MDCA, Penn has taken meaningful structural costs ($40MM+ on EBITDA of ~$180-190MM) out of the business through real estate and G&A rationalization while refocusing the business by cross pollinating assets and leveraging internal resources that resulted in MDCA winning several significant new advertising mandates (Audi, BMW, Coca Cola, Budweiser, J&J consumer, Nike, etc).

Under Penn’s tenure, top line growth was reinvigorated and MDCA generated significant cash flow. However following COVID-19, MDCA’s top line was hit considerably with Q2 organic growth down 26% (rebounding 9% sequentially in Q3). Given the variable nature of costs in the business, management responded swiftly to the pandemic and offset 86% of the revenue decline with 110% of cost reductions and remained solidly profitable.

With the stock down to a low at $1.10 at the end of June 2020, Stagwell proposed an offer to combine with MDCA offering an implied value of $4.25 a share for MDCA shareholders. While getting to $4.25 a share of value was a bit of contorted calculation, the stock shot up to the high $2s on the announcement.

After the initial offer, the board formed a special committee and retained an investment bank to review the transaction. In late December, a cleaner, revised, and superior offer was presented to shareholders.

This write up will detail the proposed transaction and provide a valuation framework we feel justifies a value for MDCA significantly higher than where the stock is currently trading ($2.75).

We have been impressed with Penn’s tenure as CEO since he took over the Company. With the end of year timing of the deal announcement and a current lack of sell side coverage, we view MDCA shares as substantially mispriced.

We see a unique opportunity to own shares in a financially stronger company with accelerating growth from digital marketing initiatives led by an accomplished CEO with fully aligned interests to create material shareholder value.

We think that in short term MDCA shares are worth $4.50-5 (~60%-80% higher). With the longer-term plan management has laid out we think the stock easily can be worth $8-10 (190% – 260% higher).

Transaction Summary

Press Release: On December 21, 2020 MDC Partners and Stagwell Media LP announced they have entered into a definitive transaction agreement to combine their respective businesses, uniting the award-winning talent of MDC with the advanced technology platform of Stagwell to create the transformative marketing company that today’s marketplace demands.

Existing MDCA shareholders (including Stagwell) will receive 26% of the common equity of the combined company. Stagwell will receive share consideration equal to 74% (excluding Stagwell’s pre-trxn holdings of MDCA and without giving effect to any conversion of outstanding preference shares). Stagwell and affiliates are expected to own 79% of the common equity of NewCo following the transaction.

- MDCA stand alone: 2020E: $1.2BN revenues, $180MM of EBITDA in 14 countries with 4,900 employees.

- Rev split: 59% advertising, 16% marketing communications, 9% digital services.

- Key assets include 72andSunny, Anomaly, Crispin Porter Bogusky and Doner.

- Stagwell LP stand alone: 2020E: $.9BN revenues, $138MM of EBITDA in 20 countries and 3,775 employees.

- Rev split: 42% digital services, 40% marketing communications, 13% research and insights, 5% content and media.

- Key digital assets include Code and Theory, Emerald Research, Finn, ForwardPMX, Harris.

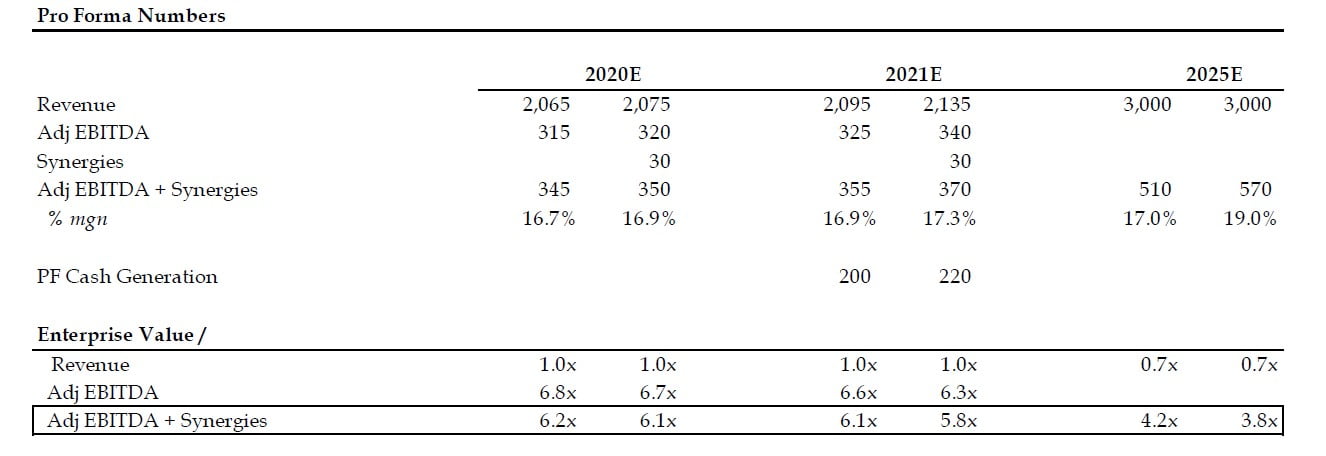

- NewCo: 2021PF: $2.0-$2.1BN revs, $355-370MM (including 30MM of 3-year cost synergies, 90% captured by year two)

- Pro forma will manage $4.4BN of media spend. $200MM+ of pro forma cash generation in 2021.

- 8,600 employees across 23 countries with 1/3 of revenues attributable to digital services (growing 10-15% annually).

- Pro forma net leverage ratio decreases from 4.2x to 3.4x (assuming full synergy capture).

- 2025E Revenue: $3BN from 9% ann. top line growth (5% organic, remainder from M&A and new products).

- $2.0BN 2021E => 2025E $2.6BN (organic) + 75MM new digital rev streams, $325MM M&A growth = $3BN of total revenues.

- 2025E EBITDA: $510-570MM assuming margins of 17-19% (Rubicon Capital assumptions).

What is of Value?

- Reasonable Pro Forma Valuation:

- Cheap on an absolute and relative basis: 10% FCF yield and at 6x EBITDA, two turns cheaper than trading peers. Transaction is deleveraging. Pro forma cost synergies seem quite reasonable at ~8% of EBITDA. Highly free cash flow generative out of the gate ($200MM+ in 2021E).

- Outsized Opportunities for Growth:

- Recovery off depressed levels should provide revenue tailwinds into 2021/2022.

- Pro forma estimates do not include revenue synergies between the two companies. Mgmt. thinks the combination could generate $90-150MM of incremental annual revs over time.

- Penn has demonstrated this ability as CEO of MDCA by marrying traditional MDCA advertising with Stagwell digital assets to generate key client wins including J&Js consumer business taken from WPP after a multi-decade relationship with that firm.

- Experienced and Aligned Management:

- CEO Mark Penn has a strong track record of creating value with advertising and digital assets.

- Stagwell’s majority pro forma ownership ensures aligned incentives for all shareholders.

Valuation Considerations

- Analysis assumes full conversion of $196MM of pref. shares (held by Stagwell and GS) at $5 (~10% dilution).

- Short term estimates assume a modest recovery scenario in 2021 with close to full capture of synergies.

- Publicly traded comparable trade around 8x EV / EBITDA. We are assuming a 7.5x multiple.

- Long term management estimates contemplate 9% annual revenue growth (5% organic). Margin estimates are in line with near term projections and industry peers.

- Long-term equity value does not consider further deleveraging which could add approx. $1+ per share to equity value from annual free cash flow generation which will only accelerate with growth.

Risks and Considerations

- Economic Uncertainty: Business can be volatile due to economic / macro conditions as evidenced by what happened in 2020. As evidenced last year, management is adept and managing the business through economic cycles. Costs are largely variable and can be flexed depending on market conditions.

- Liquidity Considerations: Pro forma, Stagwell will own approx. 80% of shares outstanding. Stagwell’s prerogative however is not to manage this closely held like a PE firm but to serve as a platform operating company and be a liquidity provider of shares to the market. While this may hold back valuation initially, the stock should rerate as management proves out its operating plan and drives value.

Catalysts

- Filing of S-4 which is imminent.

- Recovery of advertising / marketing business. Political ad spend cycle in 2022.

- Acceleration of top line growth should give way to multiple rerating.

- Increased investor awareness, better understanding of higher growth heretofore private Stagwell assets, sell side coverage (numerous analysts covered MDCA pre-2019), analyst day, etc.

The post MDCA Partners January 2020 Memo: Merger With Stagwell [Valuation Analysis] appeared first on ValueWalk.