A few key points:

1) Existing home sales are counted at the close of escrow, so the June report was mostly for contracts signed in April and May. Some of the increase this month was probably related to pent up demand from the shutdowns in March and April. I expect a further increase in sales in July (July will be mostly contracts signed in May and June when the economy was much more open). However, with the high unemployment rate – and the recent surge in COVID infections, housing might be under some pressure later this year. That is difficult to predict and depends on the course of the pandemic.

2) Inventory is very low, and was down 18.2% year-over-year (YoY) in June. This is the lowest level of inventory for June since at least the early 1990s.

3) As usual, housing economist Tom Lawler was closer to the actual NAR report than the consensus forecast.

Click on graph for larger image.

Click on graph for larger image.

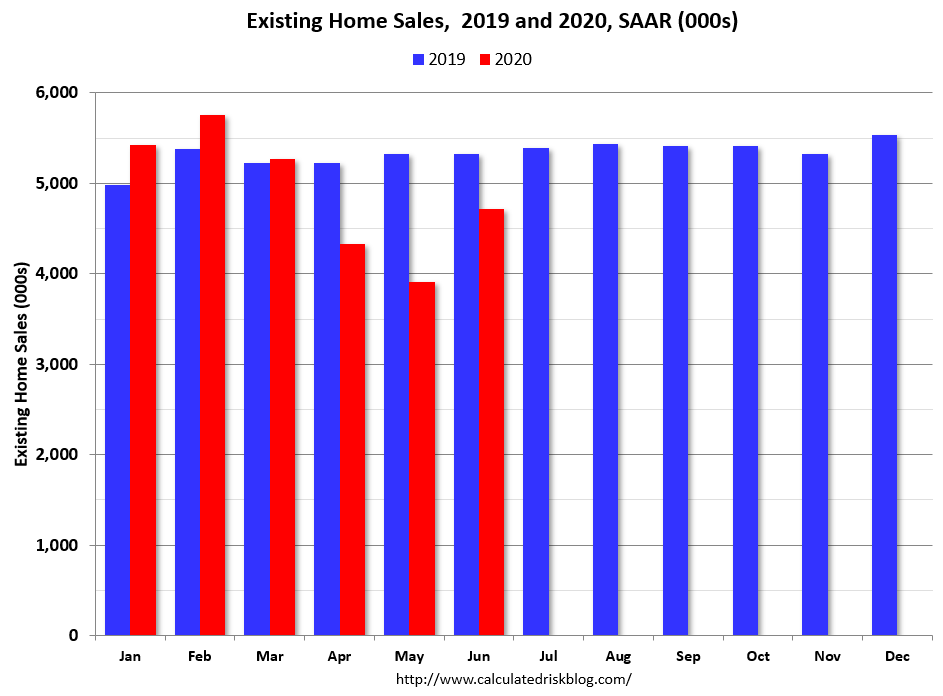

This graph shows existing home sales by month for 2019 and 2020.

Note that existing home sales picked up somewhat in the second half of 2019 as interest rates declined.

Even with weak sales in April, May, and June, sales to date are only down about 8% compared to the same period in 2019.

The second graph shows existing home sales Not Seasonally Adjusted (NSA) by month (Red dashes are 2020), and the minimum and maximum for 2005 through 2019.

The second graph shows existing home sales Not Seasonally Adjusted (NSA) by month (Red dashes are 2020), and the minimum and maximum for 2005 through 2019.

Sales NSA in June (510,000) were 3.4% below sales last year in June (528,000).