SYSCO Corporation (NYSE:SYY) markets and distributes a range of food and related products primarily to the foodservice or food-away-from-home industry in the United States, Canada, the United Kingdom, France, and internationally. It operates through three segments: U.S. Foodservice Operations, International Foodservice Operations, and SYGMA.

Q1 2020 hedge fund letters, conferences and more

A Dividend King

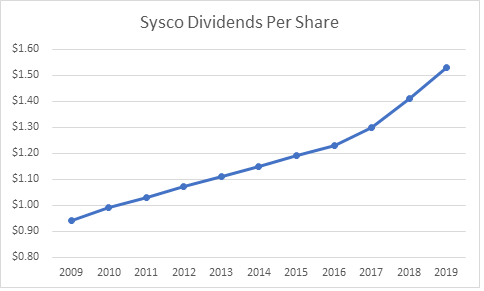

The company is a dividend king with a 50-year history of annual dividend increases. During the past decade, SYSCO Corporation has managed to boost dividends at an annualized rate of 5%.

The last dividend was in November 2019, when Sysco hiked quarterly dividends by 15.40% to 45 cents/share

Between 2009 and 2019, Sysco Corporation has managed to boost earnings from $1.77share to $3.20/share. Growth wasn’t even, as most of it occurred in the past five years. The first five years were largely flat in terms of earnings per share growth. The company was expected to earn $3.79/share in 2020, before Covid-19 hit. Now, earnings are expected to hit $2.07/share in 2020 and $2.38/share in 2021.

The company has solid competitive advantages in the distribution business, due to its scale of operations. This lets it sell each unit to customers at a lower per unit cost – because it gets to spread costs over a larger base.

In addition, it has some scale in purchases, which also result in better prices, and higher margins. Being the largest distributor, and being closer to clients can lead to better margins that competitors.

In addition, Sysco has tried to focus on cost containment, process improvement in order to improve competitiveness and increase margins. Some examples of cost containment include centralizing purchasing for its distribution centers, eliminating 10% of corporate workforce.

The company is also trying to grow through acquisitions in the US and abroad. While it won’t have the same scale and competitive advantage abroad as it does in the US, this is still a good start. Getting new customers is also something it is trying to achieve, and it tries to offer services and consulting to clients that smaller scale distributors cannot do. Sysco also has half of its orders placed electronically by customers, which frees some time for the sales team to do value added services and look for new business opportunities.

The company distributes private label products and branded products to customers. The private label ones carry better margins for Sysco.

Risks To Investing In Sysco Corporation

There are risks to investing in Sysco of course, notably labor shortages, food inflation, and recessions. It is difficult to find qualified truck drivers, which compresses margins. In addition, food inflation may make it difficult to quickly pass costs to customers, which may depress margins. A decrease in the economic activity may results in less of a demand for Sysco’s distribution of goods. Integrating acquisitions could also turn out to be more costly than expected.

The largest risk today is that a lot of their customers are having difficulties, due to Covid-19 related shutdowns. It is possible that many of their customers may not survive. The ones that are adaptable however, should be able to weather the storm.

Sysco may also benefit, because some of its smaller and less capitalized competitors may not survive, which could result in the opportunity to further consolidate its market position, and make it even stronger.

The company has been actively repurchasing shares during the past decade. The number of shares outstanding has been reduced from 596 million in 2009 to 523 million in 2019. It looks like the reduction in shares outstanding was more pronounced in the past five years, which is probably one of the reasons behind the growth in earnings per share during the period as well.

The dividend payout ratio increased from 2009 to 2015, before falling to a more reasonable 48% in 2019. Based on forward earnings, the forward dividend payout ratio is at 87%. This is high, but if you believe that this crisis is relatively temporary in nature, it may be a good time to review the stock.

Sysco’s Stock Multiple

The stock is selling for 27.50 times forward earnings and yields 3.50%. There will be an earnings hit in 2020, which means that the stock multiple looks high. Based on prior year’s earnings, Sysco Corporation looks like a steal. If you believe that there will be a recovery in the restaurant industry, and that this health crisis will dissipate soon, today may be a good time to start reviewing the company. There is a pent-up demand, where customers will want to go out, and treat themselves to a meal prepared by someone else, in an environment that is not their home.

However, if this turns out to radically change how everyone does business, leading to a wave of closures, and a reduction in demand, Sysco Corporation may end up earning less money and its dividend may be in danger. As usual, the stock price can always move lower, which is a risk particularly when fundamentals are on a shakier ground due to specific industry risks that Covid-19 is causing to Sysco.

Relevant Articles

- Dividend Kings For 2020

- 36 Dividend Aristocrats On My Shopping List

- Nine Dividend Growth Stocks With Growing Yields on Cost

- Best Dividend Stocks For The Long Run – 10 years later

- Dividend Aristocrats List for 2020

Article by Dividend Growth Investor

The post SYSCO Corporation (SYY) Dividend Stock Analysis appeared first on ValueWalk.