Strong Liquidity Should Help Social Housing Providers Remain Resilient, Report Says

Q3 2020 hedge fund letters, conferences and more

Social Housing Providers Will Remain Resilient

LONDON (S&P Global Ratings) Dec. 8, 2020–S&P Global Ratings believes that its ratings on social housing providers (SHPs) will remain largely resilient in 2021 following a temporary weakness in performance in 2020, largely because of losses in rental income linked to increasing unemployment. That said, we consider that central governments’ fiscal responses to the COVID-19 pandemic, such as job support schemes, have lessened the impact. Furthermore, as noted in a report published today on RatingsDirect, liquidity remains strong and has strengthened in some regions over the last 18 months (see Outlook 2021: Strong Liquidity Should Help SHPs Remain Resilient).

Over the next few years, we expect the social housing providers we rate to increase both capitalized and expensed maintenance spending to address delays to development schemes and repair and maintenance during 2020 due to national lockdowns, to meet enhanced building safety regulations, and to align to green agendas. “However, we believe the sector is well placed to face these pressures over the next 12 months, backed by cost-saving strategies, strong liquidity, and favorable debt markets,” said S&P Global Ratings credit analyst Karin Erlander. “That said, partly debt-funded investment requirements into the existing stock are in our view the main challenge to the sector over the next few years,” she added.

Capitalizing On Record-Low Interest Rates

To cater to an increase in investment in existing assets, while continuing to develop affordable homes, we expect SHPs to capitalize on record-low interest rates and obtain external financing. We therefore expect an increase in leverage in many countries, especially for social housing providers that operate in jurisdictions that do not have access to favorable levels of government grant funding. “Therefore, managing higher levels of debt, supported by stable and predictable cash flow, and strong liquidity positions are important for the SHPs to maintain stable creditworthiness over the next 12 months,” Ms. Erlander added.

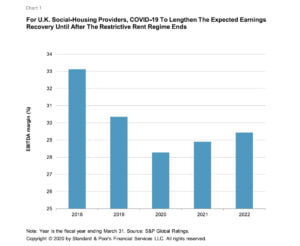

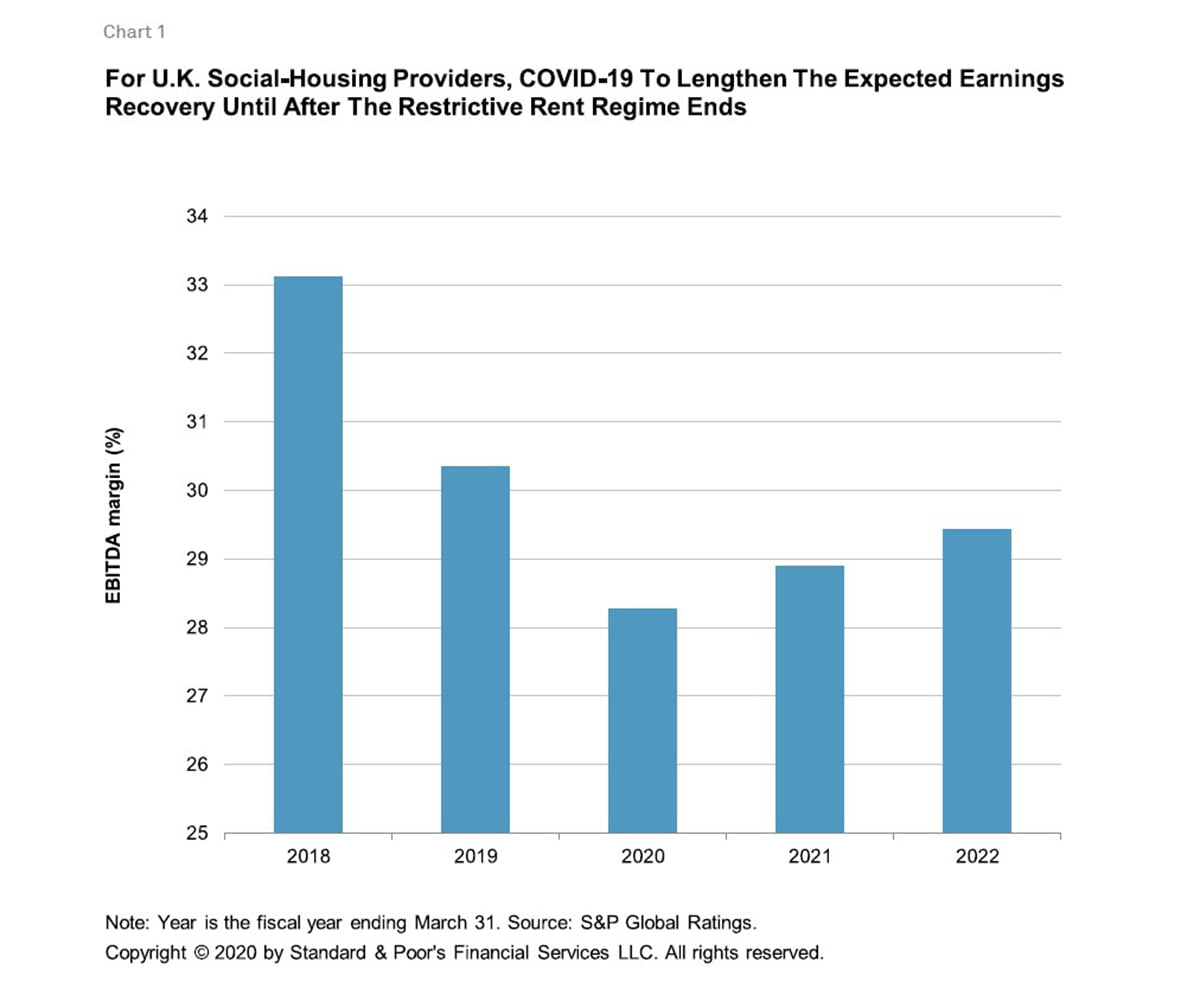

In England, we expect the recovery in earnings, which we had previously anticipated with the end of a restrictive rent regime, to be subdued. This delay in improving financial performance is mainly owing to increased spending in new and existing assets, but also due to the lower inflationary environment that constrains rent increases. A sluggish sale market attributed to the continued uncertainty about Brexit and COVID-19, more recently, have reduced cross subsidies from sales programs which, combined with relatively low grant funding, have resulted in increasing debt burdens. SHPs will have to balance increasing spending on maintenance and repairs, needed to meet higher standards for building safety and energy efficiency standards, with the ambition to continue to deliver affordable homes. At the same time, it would be important that debt service capacity remains solid even when the cross subsidies from market sales diminish.

Globally, social housing providers have proven their direct access to domestic and international capital markets for debt funding over the last 12-18 months, while also accessing the capital market via bond aggregators, such as MorHomes, THFC, and GB Social Housing in the U.K.; Kommuninvest in Sweden; and National Housing Finance and Investment Corp. (NHFIC) in Australia. SHPs in France, Canada, and Sweden may also rely on borrowings from state-related financial institutions, or directly from their owners. French SHPs can raise funds through Caisse des Depots et Consignations (CDC), which offers low-rate, regulated, long-term loans. Toronto Community Housing Corp. (TCHC), the largest SHP in Canada and the second largest in North America, expects to receive a large amount of loans and grants from the federal government over the next 10 years as part of its National Housing Co-Investment Fund. Municipal social-housing providers in Sweden largely benefit from low-interest loans from the cities that own them.

The report is available to subscribers of RatingsDirect at www.capitaliq.com. If you are not a RatingsDirect subscriber, you may purchase a copy of the report by calling (1) 212-438-7280 or sending an e-mail to research_request@spglobal.com. Ratings information can also be found on S&P Global Ratings’ public website by using the Ratings search box located in the left column at www.standardandpoors.com. Alternatively, call one of the following S&P Global Ratings numbers: Client Support Europe (44) 20-7176-7176; London Press Office (44) 20-7176-3605; Paris (33) 1-4420-6708; Frankfurt (49) 69-33-999-225; Stockholm (46) 8-440-5914; or Moscow (7) 495-783-4009.

The post Strong Liquidity Should Help Social Housing Providers Remain Resilient appeared first on ValueWalk.