Stocks had the perfect excuse to decline based on Fed’s guarded tone and no yield curve control around the corner – but apart from the late Wednesday selloff, they didn’t. Yesterday’s early U.S. session selling pressure aided by weak new unemployment claims, didn’t last long – and the bears didn’t muster enough strength to come back and try mightily again.

Q2 2020 hedge fund letters, conferences and more

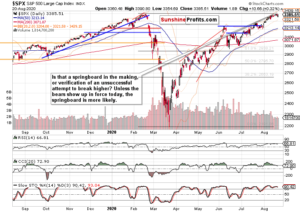

The chart clues favoring a daily S&P 500 downswing, didn’t usher it in, That’s telling in and of itself.

Such were my words at the onset of European trading earlier today:

(…) The S&P 500 didn’t waver towards the closing bell, and neither in the overnight session. The tendency of post-Fed moves to carry over to the next day didn’t work out this time, and the short-term swing structure makes it justified to expect stocks to go on with their slow grind higher as the bull market isn’t over by a long shot.

A few more thoughts on the short-term swing structure and the bearish overtone mentioned in the preceding Stock Trading Alert. These offer odds for a move to continue, to reassert itself after a brief appearance – and that can happen via an intraday or late-day reversal.

That didn’t happen, and the selling pressure at the entry to the European session is likely to fizzle out just as the attempts during second half of yesterday’s trading did.

So, if stocks couldn’t just slide and scare out the bulls, they’re likely to meander sideways to higher next. Those question marks, non-confirmations and tensions all around that result in lower volume behind each print of higher stock prices, needn’t derail the bull at all.

Sure, it means lower credibility of higher prices, weaker internals and occasional bear raids (are we seeing it arriving in today’s premarket?) – but unless things in the real world take a catastrophic turn, market participants are likely to be adding to their existing (long) positions, and despite the challenging situation on the ground (what an understatement!), the bears will be under pressure to throw in the towel until elections start to really bite.

How likely is that?

S&P 500 in the Medium- and Short-Run

I’ll start with the weekly perspective (charts courtesy of http://stockcharts.com ).

Such were my comments on the weekly chart almost 2 weeks ago:

(…) Bullish price action for many recent weeks on volume that isn’t yet inviting increasing participation of the sellers. This fact alone bodes well for higher stock prices in the medium-term, but the buyers will meet a set of two key resistances shortly.

It’s the Feb all-time highs that are drawing nearer day by day, and the upper border of the rising black trend channel.

The buyers met these resistances, yet the bears didn’t step in (please see this and many more charts at my home site) – and that fits the ongoing slow grind higher hypothesis, which has been working for weeks and months.

The caption says it all – and the bears don’t appear to be at their strongest exactly. Window of opportunity to strike is increasingly more closing down.

Let’s check the credit markets next.

The Credit Markets’ Point of View

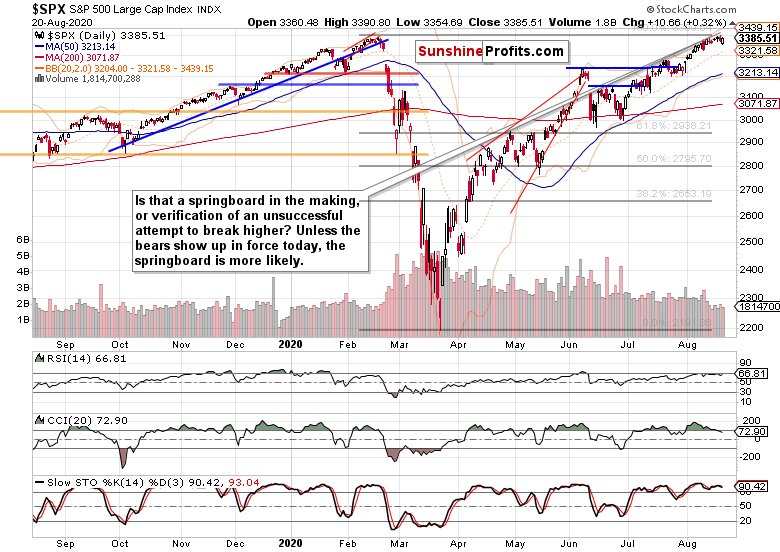

High yield corporate bonds (HYG ETF) have turned higher yesterday, and did so on volume that didn’t lag behind. That’s a reason for cautious optimism among the bulls – especially since it was mirrored by stabilization in investment grade corporate bonds (LQD ETF).

Both leading credit market ratios – high yield corporate bonds to short-term Treasuries (HYG:SHY) and investment grade corporate bonds to longer-dated Treasuries (LQD:IEI) – rose yesterday The longer they keep the sideways-to-bullish bias, the better the likelihood of their renewed move higher in earnest, and by extension, for stocks too.

Both stocks and the HYG:SHY ratio have kept as extended as they have lately been. As a result, no hint is coming forward from this chart alone.

Long-dated Treasuries (TLT ETF) are trading with still rising yields, which sends a signal about the bond market taking the economic recovery story seriously.

The stocks to all Treasuries ratio ($SPX:$UST) still remains in an uptrend – I can’t call it to have rolled over. Not with a qualifier of “just yet”, but at all – the higher highs and higher lows are clearly visible, and a textbook definition of an uptrend.

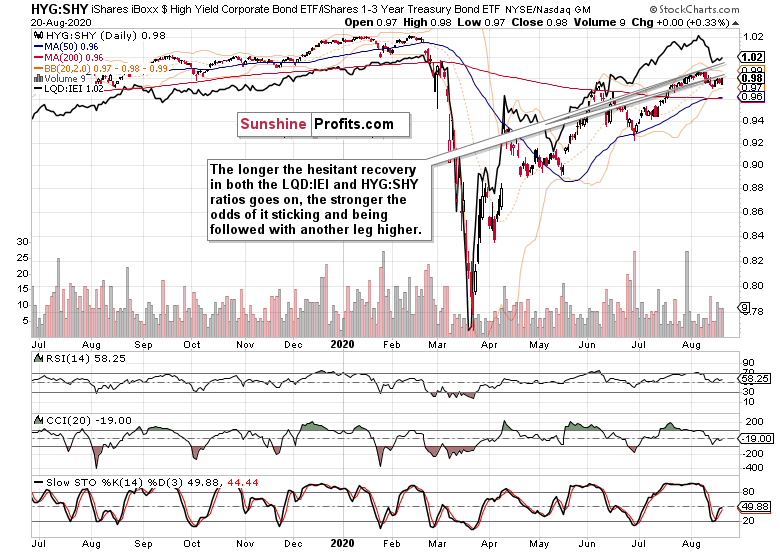

S&P 500 Market Breadth

The short-term view isn’t very clear, but I lean in the direction of the advance-decline line’s lackluster recent performance as being likely to eventually resolve with a move higher, rather than with ushering in a stock downtrend.

S&P 500 Downswing Delayed – Summary

Summing up, the S&P 500 refused to decline more when it had quite a few good reasons to do so yesterday. Today’s premarket S&P 500 downswing has taken it approximately to yesterday’s opening levels, and odds are that this dip will be bought again.

That’s true regardless of the weakening Russell 2000, which however doesn’t appear to be under distribution – not by a long shot. Emerging markets almost managed to close their yesterday’s bearish gap, and technology still continues to lead irrespective of weak semiconductors. The rotation theme in the recovery story remains on, and credit markets will shine light as to when stock strength would return.

Thank you for reading today’s free analysis. I encourage you to sign up for our daily newsletter – it’s absolutely free and if you don’t like it, you can unsubscribe with just 2 clicks. If you sign up today, you’ll also get 7 days of free access to the premium daily Stock Trading Alerts as well as our other Alerts. Sign up for the free newsletter today!

Thank you.

Monica Kingsley

Stock Trading Strategist

Sunshine Profits: Analysis. Care. Profits.

All essays, research and information found above represent analyses and opinions of Monica Kingsley and Sunshine Profits’ associates only. As such, it may prove wrong and be subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Monica Kingsley and her associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Ms. Kingsley is not a Registered Securities Advisor. By reading Monica Kingsley’s reports you fully agree that she will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Monica Kingsley, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

The post S&P 500 Downswing Delayed by One Day? Probably Not. appeared first on ValueWalk.