Silver Ring Value Partners letter to investors for the fourth quarter ended December 31, 2020.

Q3 2020 hedge fund letters, conferences and more

Dear Partners:

Happy New Year! I hope that you are staying healthy and safe. 2020 was a good year for the partnership, even though it was a hard year for all of us in many other ways. As I have said in the past, the more irrational other market participants are in response to news and events, the more our rational, disciplined value investing process has a chance to shine.

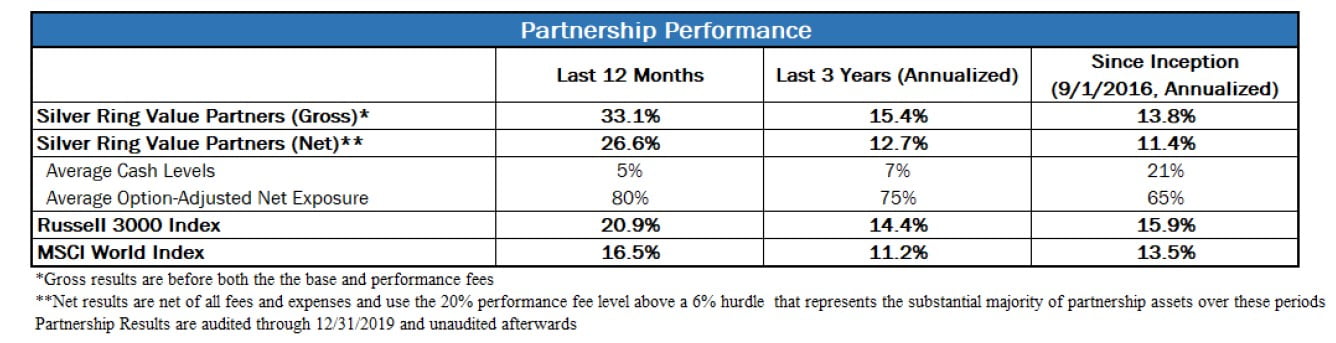

Despite the market heavily favoring high-priced growth stocks of the kind outside of my circle of competence, the partnership was up by 33% gross and by 27% net of all fees for the year. This was accomplished by investing in deeply undervalued companies following the process that I described to you in the Owner’s Manual and in prior letters, not by suddenly changing approaches to try to do what seems to be favored by the market in the moment. So much for the death of value investing!

Throughout my letters I have always attempted to focus your attention on the inputs to the process rather than on the short-term outputs. After all, whether the partnership was going to be up or down in 2020 based on year-end security prices wasn’t really up to me, but rather up to the other market participants. All I could, and did, control was how well I followed my process. If anything, it is of that that I am proud, not of the somewhat arbitrary number that I am reporting to you for the year.

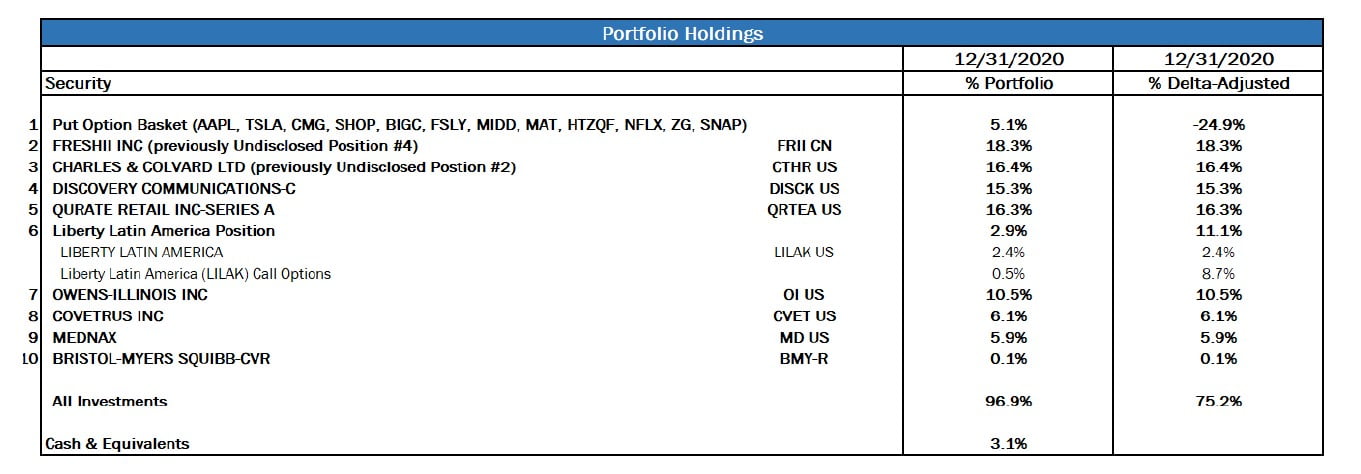

What’s more exciting to me than last year’s performance is the fact that at the end of year the portfolio was very attractively priced, with the Price to Base Case value ratio at 60%. This is what makes me excited about the opportunity for future returns. The portfolio had 10 investments, cash at 3% and option-adjusted net exposure at 75% at the end of the year. The ratio of Price to my estimate of Normalized EPS was 7x for a collection of businesses that I expect to grow profits at low-single digit rates on average over the long-term.

I am grateful to you for being excellent partners. No one questioned performance in the middle of the year as the markets were swooning. Several of you added capital when the opportunity set was outstanding. A few of you were kind enough to offer your advice and insights in your areas of expertise to help me reach better decisions. We had one new partner join us in January, and another add capital, allowing us to continue to grow in a measured way.

Executive Summary

At the end of Q4 2020 the portfolio was very attractively priced, with the Price to Base Case value ratio at 60%. The portfolio had 10 investments, cash at 3% and option-adjusted net exposure at 75% at the end of the quarter. My investment decisions are driven by bottom-up considerations, and cash is a residual of that bottom-up investment process. I do not seek to time the market, and I continue to rigorously stick to my criteria for quality and discount to intrinsic value.

Investment Activity

I made the following changes to the portfolio during Q4 2020:

- Started a small, 5%, position in Mednax (MD)

- Exited the position in Fox (FOX)

- Added to positions in Discovery Communications (DISCK) and Freshii (FRII CN, previously Undisclosed Position #4)

- Reduced the position in Covetrus (CVET)

- Converted the Qurate Retail (QRTEA) position to all equity from equity and call options

- Converted the Owens Illinois (OI) position to all equity from equity and call options

- Converted the Liberty Latin America (LILAK) position to more equity and less call options

- Rebuilt the put options basket to consist of put options on Tesla (TSLA), Apple (AAPL), Chipotle (CMG), Netflix (NFLX), BigCommerce (BIGC), Zillow (ZG), Fastly (FSLY), Mattel (MAT), Middleby (MIDD) and Snap Chat (SNAP)

- White: thesis is tracking roughly in-line with my base case

- Orange: thesis is tracking somewhat below my base case

- Red: thesis is tracking significantly below my base case

- Dull Green: thesis is tracking somewhat better than my base case

- Bright Green: thesis is tracking significantly better than my base case

- The portfolio is attractively priced at 60% of Base Case value

- Option adjusted net exposure is at 75%, reflecting option-based hedges Operational Update

- I am again hoping to have your K-1s to you by March 15th. One unfortunate side-effect of the extreme price volatility during 2020 is that it has resulted in large realized short-term gains. This is unusual given the partnership’s typical long-term holding period (one that I expect to be the norm in the future), but I didn’t see a good way to avoid it and stick to my risk management parameters given the rapid increase in the prices of several of our investments.

- I continued posting educational investing videos on my YouTube channel

- I wrote several articles on general investing-related topics at the Behavioral Value Investor, a publication of Silver Ring Value Partners, including:

First a “Thank You”

I wanted to thank Patrick Brennan of Brennan Asset Management for forcing me to do the work on Qurate Retail (QRTEA), which ended up being one of the partnership’s most profitable investments this year. When it was first mentioned to me, my mind immediately shut down. “A structurally declining retailer,” I thought. I dismissed arguments that it was cheap, thinking that it wasn’t at all uncommon to find a cheap retailer that is experiencing or is on the verge of a substantial decline in sales under the pressure of the e-commerce onslaught.

Patrick didn’t let me off the hook that easily. His arguments were persuasive enough to get me to do a deep dive, which led me to conclude that it was substantially undervalued, with management’s capital allocation actions serving as a catalyst that could close some of the gap between price and value. Thank you Patrick! Incidentally, when I attempted to pay it forward by mentioning the idea to three of my friends in the investment business, I couldn’t get much past the “it’s a broken retailer, who cares that it’s cheap” response.

I realize that it’s unusual for an investor to praise another in such a public way. Many managers use these letters to show how smart they are to current and potential clients, so complimenting a competitor would never enter their mind. However, Patrick is not a competitor, but a friend. He is a terrific investor with deep domain expertise in his area. Arguably, he is the world’s most knowledgeable investor on any company having to do with John Malone and the Liberty family of companies. Importantly, through many conversations with Patrick over the last few years, it has become clear that he has the temperament of a great investor. I admire his tenacity in sticking to his disciplined value investing approach despite a very inhospitable market environment. I and the partnership are better off for my friendship with him.

Portfolio Update

Investing Environment

While I like the prospects of our current investments, it is difficult to find new ones that meet my criteria. That, far more than any top-down indicator, tells me that the market is in a dangerous state. Over my 20 years of professional investing, difficulty finding new ideas has been a good indicator of an over-extended market.

This doesn’t mean that we should expect an imminent market collapse, or a collapse at all. However, the implied expectations in securities are for most things to go right. For interest rates to stay low for a long time without accelerating inflation. For an economic recovery. For a calm geopolitical environment.

All of these things could happen. They might even be likely to happen. However, current security prices do no leave much room for anything to go wrong. They lack a margin of safety. Just like almost nobody could have predicted last year’s COVID pandemic and the ensuing damage that it has caused, we are just as unlikely to predict where or why the next set of problems will occur.

What is predictable is that when these challenges do occur, there is plenty of room for the currently optimistic security prices to decline.

So what is the best way to deploy capital in such an environment? Very carefully. It doesn’t follow that we should sell all of our investments and hold cash. That is not an approach that I know how to add value with. It does follow that we should keep the bar for new investments high and be vigilant to guard against permanent capital loss both at the security level and at the portfolio level.

Ultimately, we know that the market will over-react again, whether as a whole or with respect to individual companies. My job is to be prepared, mentally and in terms of our portfolio, to take advantage of the next set of irrationally priced investments, whenever they occur.

Portfolio Activity

Freshii (FRII CN, previously Undisclosed Position 4)

As Silver Ring has crossed the holding levels which necessitate a regulatory filing disclosing the position, I wanted to take this opportunity to explain the thesis on Freshii in-depth. I am including a separate report which I encourage you to read if you would like to understand how the investment process was applied and the full investment thesis. The short version is that the company is trading at a small premium to cash on the balance sheet despite being FCF-positive in the depth of the downturn, is run by a founder-CEO who has most of his net worth invested in the stock, and presents a very asymmetric risk-reward between limited long-term downside and substantial upside despite the near-term challenges facing the business.

Mednax (MD)

Mednax is a business that I have followed for many years. The crown jewel is the pediatric business, in which the company provides physician staffing to neonatal intensive care units (NICUs) and related specialties at various hospitals. It’s a business with a strong competitive advantage given the company’s dominant position, very inelastic demand and limited reimbursement risk.

The pediatric business has moderate organic growth characteristics, which the prior management supplemented with many tuck-in acquisitions over the years. These acquisitions leveraged the back office scale while allowing the local physician groups’ autonomy of operation.

Unfortunately, the company eventually ran out of meaningful acquisitions to make in this space, and the old management was unsatisfied with simply running a very entrenched, high ROIC and FCF business and returning capital to shareholders. Instead, they took on extra debt to pursue growth through acquisitions in what they considered to be adjacencies: first in anesthesiology and then in radiology.

Not surprisingly, these adventures outside the company’s area of core competitive advantage didn’t go well. Debt piled up far faster than profits. This led to an activist investor nominating directors to the board, and then the board replacing the CEO.

The new CEO was previously the CEO of Quality Care Properties. This was a company where he improved performance over this 2-year tenure and which he then sold at an attractive price. His first steps at Mednax were simple: sell off the non-core divisions and reduce debt.

I made the investment after the sales were completed, leading to a clean balance sheet and the company returning to its roots as a pediatric-centered company. This company doesn’t screen well to many investors since its historical financials are messy and are obscured by the old businesses (now sold) and the seemingly large debt pile (already reduced). This is a perfect set-up: the nature of the business is different than what most investors believe it to be based on a superficial assessment.

The new management is now focused on improving efficiencies and running the core business better. I would not be surprised if the ultimate plan were to sell the company in a few years at a nice profit. However, I am not banking on that, and would be equally happy if management just executes on its low-risk plan of running the business well within its area of competitive advantage.

I purchased the stock at less than 10x normalized EPS for a business that I believe is likely to grow mid-single digits long-term. I paid ~ 65% of my base case value with ~ 35% downside to my worst case. I believe the Business Quality to be Excellent (1 out of 5), Management Quality to be Above Average (2 out of 5) and Balance Sheet to be Above Average (2 out of 5).

In the short-term, birth-rates, a key driver of demand, are likely to be negative. This may create quarters where the company reports results lower than Wall Street expectations. I am not at all concerned or deterred by that. If anything, I would be happy to add to the position if such an event occurs and the market over-reacts given our long-term investment horizon.

Fox Corp (FOX)

I sold our investment in FOX during the quarter at a small loss and redeployed the proceeds into shares of Discovery Communications and Mednax. The main reason for my sale was a new competitive threat, which widened the range of likely company outcomes. Furthermore, it added a competitive threat to the existing threat of secular decline that the industry is already battling to overcome. The probability of being right on having two independent things work out for the company is much lower than of it overcoming just one problem.

Fox Corp gets a substantial majority of its profits from Fox News. This is a network with very inelastic demand which has appeal to the ~45% of the country with conservative political views. With President Trump having lost the election, he began to agitate his supporters to switch viewership to more right-wing news outlets that were being more supportive of him and his claims about the election. Furthermore, there has been talk of him launching or backing a competing network, fracturing the conservative audience.

It’s possible that I am over-reacting and that nothing will come of this threat. Fox has a strong competitive position and has contracts with key on-air talent. However, initial evidence showed a spike in viewership at previously fringe right-wing networks as Trump supporters began to switch in droves away from the (in Trump’s view) insufficiently loyal Fox News network.

I don’t know how this will play out, but investing is not about answering tough questions, but rather about finding easy ones to answer. This would be a tougher decision if the choice were between continuing to own FOX and holding cash. However, I was able to redeploy the proceeds into two investments that were on average equally undervalued without the complexity of a looming competitive threat.

Portfolio Review

Being that this is the end of the year letter, I thought it would be timely to review the current holdings in the portfolio. Fortunately, that is manageable given our concentrated approach. I can only imagine doing this for a traditional mutual fund with 30-300+ investments!

I thought the best way to proceed would be to combine a quantitative assessment with a qualitative assessment of each holding. Since 2020 saw a lot of turbulence in the economy with depressed levels of demand for most businesses, I thought a good way to look at our holdings quantitatively would be to see how the companies held up during the 3rd quarter of the year (the 4th quarter results are not yet out). This was a quarter heavily impacted by the COVID-related downturn and represents a real-world “stress test” to each business. By focusing on just the numbers I hope to minimize the behavioral biases from any narrative that my mind might want to put around the reasons for them.

If the quantitative exercise seems way too short-term to you for a long-term investing approach, bear with me. For the qualitative review I focused on my qualitative vision for each company’s future 5 years out. No numbers allowed. The approach is for me to articulate what each company looks like in 5 years if things go according to plan, and then highlight some potential stumbling blocks that might keep it from getting there. This is somewhat akin to how players think in chess – rather than focusing on the next move, imagining a desired position and then working backwards.

My hope is that by combining these two approaches I can clarify my thinking on each company as a long-term investment while at the same time grounding that vision in the reality of how each company did during an abrupt recession. Neither of these are meant to replace my usual 5-Step Research process, but rather to provide a complementary lens on our investments.

Quantitative Portfolio Review

For each of the companies that we own, the table that follows displays:

- Q3 Organic sales growth y/y – How was the demand for the company’s goods/services influenced by the recession and shutdowns?

- Q3 EBITA growth y/y – How did the company’s sales growth/decline combined with operating leverage and any cost actions translate into profit growth/decline?

- Trailing 4 Quarters FCF % end of year market cap (net of excess cash) – How does the company’s FCF generating ability during a 12-month period which is arguably well below mid-cycle in terms of the economy compare with what the market is valuing the company at?

One can take issue with these specific metrics and add or modify metrics in a number of ways. However, I find these to be sufficient to give us a quantitative snapshot of how our companies held up in the throes of the crisis and the implied expectations in the stocks.

Qualitative Portfolio Review

Freshii

Business Vision in 5 Years: The company has strengthened its franchise system. Its focus on consistent execution, menu innovation and franchisee selection has led to a healthy ecosystem and a stronger brand. This has led to sustained grown in same-unit sales as well as a measured, consistent expansion in a number of locations in the U.S. and Canada. The consumer product division has ramped up and is a meaningful contributor to the business, with a full rollout at current partners and healthy growth in new partners. Management has been able to balance the two businesses without one cannibalizing the other, nor the partner business hurting the Freshii brand. Additionally, the company has added a digitally-ordered and company-delivered food business as a third leg of growth. This has been done in a way that partners with franchisees where practical and supplements them from company-owned central kitchens in ways that doesn’t make franchisee economics unattractive.

What Can Prevent It From Getting There:

- Management mis-execution and turnover

- Franchisees never recover from a shift in consumer work habits given Freshii’s current reliance on the lunch business

- Company damages its brand in the partner business by offering food that is neither as good nor as fresh as promised

- The company’s new initiatives compete with the franchisees, causing strife between them and the company and a negative spiral with the best franchisees leaving the system

Charles & Colvard

Business Vision in 5 Years: Moissanite gains wider acceptance among young consumers. The company strengthens its brand and expands its awareness to a much larger universe of potential customers. It transitions from being primarily a maker of moissanite jewelry to a broader brand that appeals to young consumers. Charlesandcolvard.com becomes the main channel through which the company does business, with the retail channels carefully curated to offer differentiated products to attract new consumers to the brand. The company is no longer reliant on paid search or mainstream paid-social as customer acquisition channels, and instead develops a strong word of mouth plus low-cost social media approach that allows it to acquire new customers cost effectively. Management is able to substantially increase the repeat-purchase rate among its customers, creating a loyal, recurring source of demand.

What Can Prevent It From Getting There:

- Low-priced Chinese competitors gain traction and market share as consumers don’t see the company’s products as sufficiently differentiated to command a premium

- Synthetic diamonds come down in price where they take share from moissanite and the company is not able to become a meaningful seller of non-moissanite gems

- Competitors box the company out from its customer acquisition channels and management is unable to successfully replace them with new ways of acquiring customers cost-effectively

- Management pursues acquisitions which distract it from executing, damaging the culture and diluting the brand instead of strengthening it

Discovery Communications

Business Vision in 5 Years: The company has successfully transitioned from being distributed primarily by cable and satellite companies to a combination of traditional distributers and direct to consumer streaming packages. Its brands have strengthened due to careful content curation and wider awareness. Its direct to consumer rollout made management realize that they have a large, inelastic audience that is happy to pay for its unique content in many markets. The decline in pay TV subscribers has ended as those who wanted to leave the ecosystem did and the remaining large portion of the population is happy to pay for a more streamlined bundle. The company is able to maintain and grow its advertising revenue stream while substantially increasing its distribution revenues.

What Can Prevent It From Getting There:

- Competing content from Netflix, YouTube and other internet sources weakens the company’s brands and makes its content less compelling to viewers

- The direct to consumer rollout makes management realize that there is only a small core audience that is willing to pay for its content directly in amounts that make the economics worthwhile

- The surge in streaming offerings to consumers precipitates a quick breakdown of the pay TV ecosystem, which is replaced by a direct to consumer model that only replaces a fraction of the old revenues

Qurate Retail

Business Vision in 5 Years: The company continues to benefit from the trend towards shopping from home. This allows the business to gain new cohorts of loyal repeat buyers. As traditional retailers struggle to fully recover from the dual pressures of growth in e-commerce and the COVID pandemic, Qurate benefits by offering a combination of shopping and entertainment to a growing universe of consumers. This leads to the company growing sales and profits not just in 2020/2021 but over the long-term.

What Can Prevent It From Getting There:

- The boost in demand from the COVID lockdowns proves transient, and the company resumes its prior sales declines

- Other companies, such as Amazon, are finally able to replicate some of what Qurate offers to its loyal shoppers, causing an accelerating erosion among that cohort

- Merchandizing mistakes that cause the company to lose relevance with its consumers

Liberty Latin America

Business Vision in 5 Years: The company successfully integrated the AT&T acquisition in Puerto Rico, leading to a much more profitable and competitively advantaged business able to seamlessly offer the “quad-play” (wireless, data, landline phone and TV). It has completed a few other deals, in each case paying careful attention to price and strategic fit. The low data penetration rates allowed the company to grow much faster than more mature U.S. and EU peers, especially after the COVID pandemic highlighted the importance of data to consumers.

What Can Prevent It From Getting There:

- Government regulation hurts the economics of its businesses

- Competitive intensity, especially in markets like Chile, with several competitors, flares up and competes away the benefit of market growth

- A prolonged recession in Latin America leads government to nationalize some of the businesses

Owens-Illinois

Business Vision in 5 Years: Glass containers have held their share of the market, resulting in the company’s business being moderately larger in U.S. and the EU and substantially larger in Latin America. The company’s MAGMA technology succeeded and allowed the business to grow in a more capital-efficient manner. Revenue growth has allowed margins to expand modestly. The company has resolved its outstanding asbestos issues for a sum consistent with management’s estimates.

What Can Prevent It From Getting There:

- Aluminum takes a large amount of share from glass containers

- The company loses share in the EU due to competitors out-innovating it and the company under- investing in its business

- Latin American growth slows or reverses due to a prolonged recession

- Asbestos claims are not settled in federal courts or are settled for a very large amount relative to management’s projections

Covetrus

Business Vision in 5 Years: The distribution business continues to grow at a moderate clip. The company’s Vets First Choice SaaS business both adds a substantial number of new vet practices and meaningfully increases the revenue per practice in the U.S. The company develops a growing business in Europe which is several years behind the U.S. in its maturity. These developments lead to an explosion in profits as the relatively high contribution profit margins from the SaaS business make Vets First Choice the more profitable of the two divisions.

What Can Prevent It From Getting There:

- Market structure changes so that vets give up on selling drugs to consumers, cede that business to others like Chewy’s, and increase prices for their services to maintain practice profitability

- Consolidating suppliers squeeze the economics out of the distribution business

- Vets prove more resistant to adopting Vets First Choice software and the majority never reach the revenue potential that it offers

Mednax

Business Vision in 5 Years: The company was able to cut costs without damaging the pediatric business. Revenues grow at healthy rates due to both the underlying growth in the number of births/reimbursement rates as well as management’s ability to cross-sell services to existing hospital clients. This leads to an improvement in margin to exceed the prior levels seen in this business.

What Can Prevent It From Getting There:

- The changes that management is making to costs and processes damage the culture, distract the physicians and cause attrition and revenue declines

- Unexpected negative reimbursement changes reduce the company’s pricing

Performance Discussion and Analysis

I encourage you to consider the results summarized below in conjunction with both the investment thesis tracker as well as the discussion of the individual companies in this letter. Any investment approach that is judged over less than a full economic and market cycle is liable to appear better than and worse than it really deserves at different points. Ultimately, it is the quality of the investment process and the discipline with which it is implemented that determines the long-term outcome. Therefore, I strongly encourage you to focus on process over outcome in the short-term.

Your Questions

As I have committed to do in the Owner’s Manual, I will use these letters to provide answers to questions that I receive when I believe the answers to be of interest to all of the partners. This quarter I received one question that I thought it would be helpful to address in this letter. (Please keep the questions coming; I will do my best to address them fully.)

What makes you comfortable having a micro-cap stock like Charles & Colvard be such a large position?

In the Owner’s Manual I discussed my position sizing guidelines as a function of business quality, downside to the worst case value estimate and the expected return to my base case value estimate. Market cap was intentionally not a factor.

However, this is a fair question, since micro-cap companies usually have some or all of the following characteristics:

- Higher share-price volatility

- Low stock liquidity

- More fragile business models

I am not at all concerned with the first of the above, higher stock volatility. You shouldn’t be either. In the long-term, such volatility will only serve to our advantage, as it gives us the option to occasionally add to our position at far more advantageous prices than we would find with larger stocks.

Low liquidity pairs well with our long-term time horizon. Approaching investing from the perspective of business value 3-5+ years out rather than stock prices a few quarters out doesn’t require high liquidity. That’s where you, my partners, also add substantial value to the partnership via your patient capital and long-term time horizon. Funds lacking these are not likely to want to have even the most promising small companies as too big a position.

Managers frequently avoid making very attractive small-cap stocks large positions for business reasons, not because of the underlying investment considerations that they would have if managing his or her own capital. I make no such distinction and manage your money the same way I would if I were managing only my own family’s capital. It is also important to make a distinction between having a large micro-cap position or two and having the whole partnership invested in such as way. Liquidity can be handled at the portfolio level and does not preclude us from having a large position in a micro-cap security when appropriate.

The last point is the most potentially concerning. It would be a mistake to make a fragile business a large position, even if the security were very cheap. Normally such an investment would be relegated to the small, 5%, position tier if made at all. Let’s look at the two specific cases where this has been relevant recently, Charles & Colvard (CTHR) and Freshii (FRII CN).

In the case of the former, I made it a medium, or 10%, position when the stock was around 70c per share. At that time there was approximately 50c of excess cash per share, no debt, positive FCF and over $1/share of inventory. If we were to assume the cash were perfectly safe and would not decrease, in this scenario it would be very hard to lose a meaningful portion of our investment even if the business proved to be worthless.

Is there a difference between a 10% position in a company with 70%+ of its market cap in net cash and a combination of 7% cash and a 3% position in the underlying business with no net cash? Yes. In the latter we have control over the 7% cash while in the former scenario the management and the Board does. So if they were to deploy this cash poorly, we could see our margin of safety decrease or dissipate. That, incidentally, is why I took an activist stance and wrote a letter to the company’s Board of Directors (discussed in last quarter’s partnership letter) when the company announced that they are considering making acquisitions with our cash.

In short, I judged the probability of losing a substantial portion of our 10% as very low given the circumstances. Would I make CTHR a 10% position if it had no cash to protect our downside? No.

I made Freshii (FRII CN) a large, 15%, position in the middle of 2020 when the stock was trading for around the cash value on the balance sheet. The business had no debt, is an asset-light business model that doesn’t require much capital, and was generating positive FCF even in the thick of COVID. We also have a founder-CEO who has most of his wealth invested in the company.

So even if the business were to prove worthless (highly unlikely), we wouldn’t lose our money unless the cash was wasted. That’s not impossible, but I judge it to be unlikely.

Are there risks? Sure. For example, management could in theory perform some take-under maneuver where they take the company private for a small fraction of its true worth. However, that scenario, whatever its probability, would make it unlikely for us to lose money. Rather, it would cut off our upside from the investment (still not a great outcome). So to lose a meaningful amount of the partnership’s capital, we would need the business to be worthless and the cash wasted, or management acting extremely unscrupulously in somehow taking actions to depress the public market perception of the business value, tanking the stock, followed by a low-ball takeout offer. In short, it would be very hard to lose a meaningful portion of the partnership’s capital from the levels where I made the stock a 15% position in 2020.

The bottom line is that what made these two investments appropriate candidates for a medium and a large position size respectively is the excess cash protecting our downside. These are the exceptions that prove the rule. You should not expect average or worse businesses to be large investments in the partnership unless there is some sort of asset-based downside protection, as was the case in these two situations.

Portfolio Metrics

I track a number of metrics for the portfolio to help me better understand it and manage risk. I track these both at a given point in time, and as a time series to analyze how the portfolio has changed over time to make sure that it is invested in the way that I intend for it to be. Below I share a number of these metrics, what each means, and what it can tell us about the portfolio. As time passes, you should be able to refer to these charts and graphs to help you gain deeper insight into how I am applying my process.

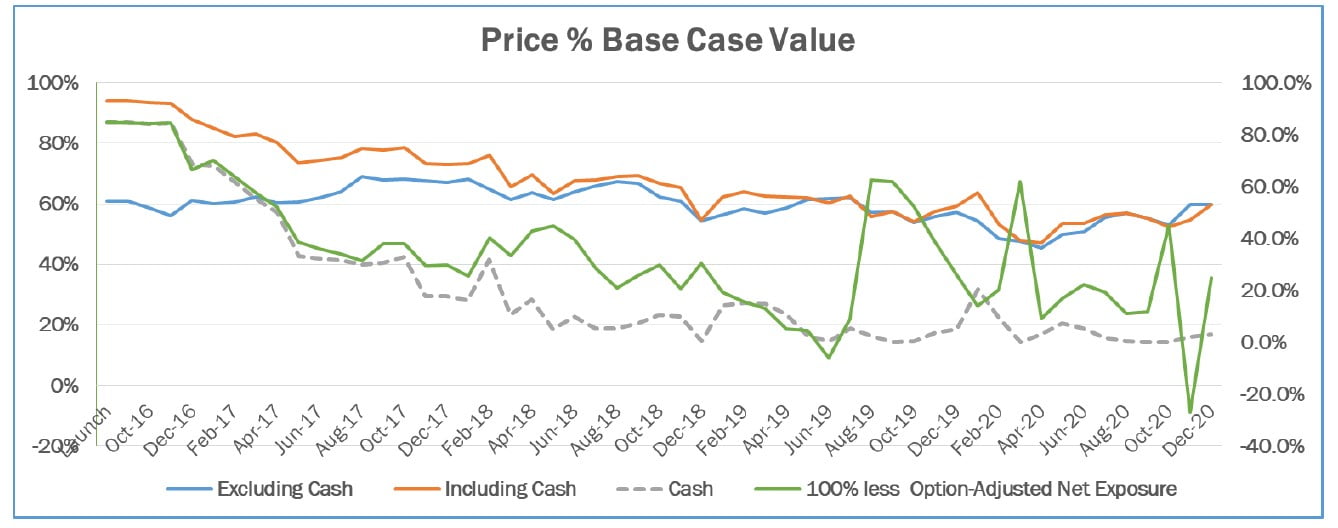

Price % Base Case Value

This metric tracks the portfolio’s weighted average ratio between market price and my Base Case intrinsic value estimate of each security. This ratio is presented both including cash and equivalents, which are valued at a Price to Value of 100%, and excluding those. All else being equal, the lower these numbers are, the better. Excluding cash and equivalents, a level above 100% would be a red flag, indicating that the portfolio is trading above my estimate of intrinsic value. Levels between 90% and 100% I would characterize as a yellow flag, suggesting that the portfolio is very close to my estimate of value. Levels between 75% and 90% are lukewarm, while levels below 75% are attractive.

Quality Quintiles

As outlined in the Owner’s Manual, I evaluate the quality of the Business, the Management and the Balance Sheet as part of my assessment of each company. I grade each on a 5-point scale with 1 meaning Excellent, 2 Above Average, 3 Average, 4 Below Average and 5 Terrible. The chart that follows presents the weighted average for each of the three metrics for the securities in the portfolio.

Portfolio at Risk (PaR)

I estimate the Portfolio at Risk (PaR) of each position by multiplying the weight of each position in the portfolio by the percent downside from the current price to the Worst Case estimate of intrinsic value. This helps me manage the risk of permanent capital loss and size positions appropriately, so that no single security can cause such a material permanent capital loss that the rest of the portfolio, at reasonable rates of return, would not be able to overcome. I typically size positions at purchase to have PaR levels of 5% or lower, and a PaR value of 10% or more at any time would be a red flag. The chart below depicts the PaR values for the securities in the portfolio as of the end of the quarter. Positions are presented including options when applicable.

Normalized Price-to-Earnings (P/E) Ratio

I supplement my intrinsic value estimates, which are based on Discounted Cash Flow (DCF) analysis, with a number of other metrics that I use to make sure that my value estimates make sense. One of the more useful ones is the Normalized P/E ratio. The denominator is my estimate of earnings over the next 12 months, adjusted for any one-time/unsustainable factors, and if necessary adjusted for the cyclical nature of the business to reflect a mid-cycle economic environment. The numerator is adjusted for any excess assets (e.g. excess cash) not used to generate my estimate of normalized earnings. One way to interpret this number is that its inverse represents the rate of return we would receive on our purchase price if earnings remained permanently flat. So a normalized P/E of 10x would be consistent with an expectation of a 10% return. While the future is uncertain, it is typically my goal to invest in businesses whose value is increasing over time. If I am correct in my analysis, our return should exceed the inverse of the normalized P/E ratio over a long period of time. The graph below represents the weighted average normalized P/E for the equities in the portfolio.

Conclusion

I was teaching my oldest son probability using a deck of cards. My youngest, Jacob, who was almost 4 at the time, saw us. “Can I play too??” he asked. I agreed.

The game was simple: Each one of us would take turns guessing the suit of the next card. The one who got the most right when the deck ran out won.

The first game Jacob was on a roll. He out-scored me by a ratio of almost 2:1. His eyes lit up and there was a big smile on his face. “I am crushing it!” he exclaimed.

The second game went differently. Now he was the one who was behind on points. His look turned dejected, and his smile became a frown.

He didn’t understand yet at his age. The cards are random, and there is no way to “win”1 other than chance. It made me smile and reminded me of investors. The ones who look at daily, monthly and quarterly “returns.” Thinking they are “crushing it” or getting “crushed.” All of that time being fooled by the randomness of the market.

To illustrate the point, recall the letter that I e-mailed you in early November (enclosed as an Appendix to this letter) when performance wasn’t good on a then year-to-date basis. In it I said that I thought this was a great time to add capital given how attractive the portfolio was. I had no idea that the portfolio would go up meaningfully within weeks, and clearly it didn’t have to happen that way. I am focused on “crushing” what is within my control. The rest will play out as it may.

I am happy to answer any questions you have. Your feedback is important to me; please let me know how I can improve future letters. I greatly appreciate your trust and support, and I continue to work diligently to invest our capital.

Sincerely,

Gary Mishuris, CFA

Managing Partner, Chief Investment Officer Silver Ring Value Partners Limited Partnership

Appendix 1: Letter to Partners dated November 12th, 2020

Dear Partners,

I hope that you and your families are healthy and safe. As I write this, the partnership’s portfolio is up mid-single digits YTD, with November’s price movements more than offsetting October’s declines that you might have seen on your statements. By the time you read this, and certainly by the end of the year, the results will again change in ways that I cannot predict.

Let me be clear: these are bad results. I am not moving the goal-posts or making any excuses. The goal is still to beat the market over a full cycle while taking less risk of permanent capital loss. If I didn’t strongly believe that these results were achievable, I would not be doing what I am doing or have most of my family’s capital invested in the partnership.

I ask you to consider three things:

- I believe that the process that I have been implementing and sharing with you in my letters has been good. I am sticking to my value investing process and doing what I told you I would be doing in the Owner’s

- We are measuring performance at one of the worst possible points for value investing as a The four years since the partnership’s launch have definitely not constituted a full cycle.

- The portfolio is concentrated and trading close to 50% of my estimate of likely business It won’t take many of the investments that we own closing the gap between market price and value for the partnership’s results to look very different.

This brings me to my next point: I believe that now is a very good time to add capital to the partnership if your circumstances allow it. This is not a statement about the market. Rather, it is a bottom-up assessment that at current prices I have a number of investments that I could add new capital to at very attractive prices. Those partners who added capital in March and April allowed me to buy extremely undervalued investments for the partnership, a number of which have done quite well thus far for us.

I understand that it is unusual to ask for additional investments after a period of bad performance. The standard approach in the investment management industry is to ask for additional capital after a stretch of good returns. After a period of poor performance the usual approach is for the investment manager to lay low and hope that the clients don’t notice and stick around. However, when I started Silver Ring Value Partners, I wanted it to be a partnership in the true sense of the word. To me that means telling you what I would want to be told if our roles were reversed.

Value investing has had a long tough stretch, prompting some to question whether in a world of rapid technology and business model changes it still works. Despite my 20 years of investment experience, I am doing my best to continue to grow and evolve as an investor. My appreciation for business and management quality has increased over the years, and I am certainly not just blindly buying statistically cheap stocks with nothing else going for them. However, I am a value investor, I believe that value investing does work over time, and I have no intention of capitulating and changing my style drastically just because it is out of favor. I am sure there are good investors out there who can successfully invest in expensive growth stocks, but that is not within my circle of competence. I expect to evolve and improve as an investor over time, but I will not abandon my approach to try to catch up with the market.

To quote Winston Churchill: “Never give in, never give in, never, never, never, never -in nothing, great or small, large or petty – never give in except to convictions of honour and good sense.” He said these words in 1941, facing far greater peril than the pressure of financial results, but I believe the sentiment that he expressed is a good rule to live by in all parts of life.

I like and appreciate every one of you. This holds true, and will hold true, regardless of what you decide to do or not do with respect to your investment in the partnership. I am grateful for your trust and support over the years.

As we have not had a chance to have our annual partnership meeting this year, I would be more than happy to speak with you individually. Whether it is just to catch up or if you have questions about the partnership, just let me know if and when you would like to talk.

I hope that you and your families have a healthy and joyous holiday season. In these times of heightened uncertainty, I have found comfort in the company of family and friends and in relationships that I have built over the years. I wish you a healthy and happy holiday season.

Thank you in advance, Gary Mishuris, CFA

Managing Partner, Chief Investment Officer Silver Ring Value Partners

The post Silver Ring Value Partners 4Q20 Letter: long Mednax appeared first on ValueWalk.