Follow my logic:

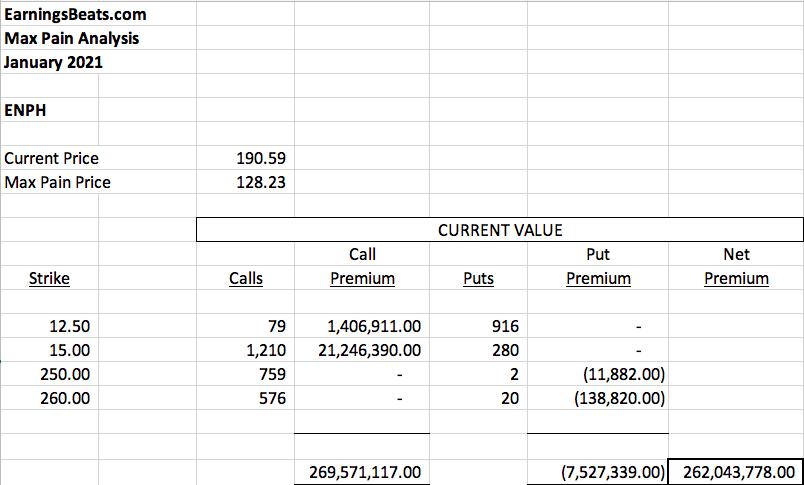

You expect ENPH to go higher, so you buy 10 calls at XX strike price on ENPH. The market maker that sells you those 10 contracts employs a covered call strategy and buys 1000 shares of ENPH. (This protects the market maker as ENPH’s stock price rises). Thousands of other traders do this same thing – buying ENPH calls like crazy. As we approach January options expiration, there’s a TON of ENPH “in-the-money” calls as a result of this continuing practice on a rapidly-rising stock. At the Thursday price high, ENPH traded at 216.22 and here was the calculation of ENPH’s net in-the-money call premium:

Couple things. First, note that the “strike” price jumps from 15.00 to 250.00 and that the columns don’t add up. I “hid” many rows on my spreadsheet so that I could show you the net call premium based on current price vs. max pain price. Second, the “Max Pain” price of 128.23 is the price at which all of ENPH’s call value and put value would net to zero. Next, since ENPH is trading well above 128.23, there is a tremendous amount of “net in-the-money call premium”. My estimate is $360 million. This is just one stock, mind you. Now, if ENPH were to finish Friday’s trading at 216.22, market makers would not lose $360 million. That’s important to understand. Remember, their covered call strategy entails owning the stock. So yes, they lose on the increased value in those net calls, but they’ve benefited by an equal amount by owning the stock.

But here’s the kicker.

What if, on Friday option expiration day, market makers began selling their long positions, possibly even shorting ENPH to drive the price lower temporarily. What would that look like? Well, they’d be cashing in their massive profits on the long side. They’d then potentially profit by the short-term downside because they’re now on the short side. AND….they’d save MILLIONS of dollars of net call premium.

It’s a WIN, WIN, WIN!

Now let’s discuss what actually happened. ENPH lost 18 bucks on Friday (worst performing stock on the S&P 500 – what a coinky dink!) and closed at 190.59. The net call premium fell to $262 million, saving nearly $100 million in option payouts!

Now let’s look at the ENPH chart. While this thievery is taking place in the market, technicians might simply chalk this up to “needing to fill the gap back to 181” or profit taking down to the 20 day EMA.

Many will look at this as normal behavior, but I know better and so should you. In fact, since many holding in-the-money call options likely exercised their options and bought ENPH stock, market makers become short sellers at that time. That could put more pressure on ENPH to the downside as we begin a new week on Tuesday.

I discuss many interesting market concepts in our FREE EB Digest newsletter, published 3x per week, on Mondays, Wednesdays, and Fridays. There’s no credit card required and you may unsubscribe at any time. CLICK HERE to sign up with your name and email address.

Lastly, I’m hosting a “Sneak Preview – Q4 Earnings” this afternoon at 4:30pm ET. It’s free to the public and you may join using the following room link (the room will open at approximately 4:00pm ET):

https://us02web.zoom.us/j/89207646261

Tom Bowley, Chief Market Strategist

EarningsBeats.com

“Better Timing. Better Trades.”