It’s never a good idea to try and predict contra-trend moves in a strong equity bull market, because the benefit of the doubt always goes with the prevailing trend. If false moves develop, they have a strong tendency to develop on the downside. That said, several key indexes and indicators have fallen back to levels that have got my attention. These indicators need to hold; otherwise, further downside testing will likely take place.

Chart 1 features the NYSE A/D Line and the common stock A/D Line. Both are trading well above their 200-day MAs, which tells us that the main trend is positive. However, the A/D Line itself has just bounced from a 5-month up trendline, which could prove to be the opening shot in signaling a correction in the event that it is violated. The Common Stock line has not yet broken its trendline, but is obviously at a critical point. None of this says that a new bear market is underway. However, if we do get further weakness in the Common Stock A/D Line, it will definitely add to the weight of the evidence favoring an extension to this week’s setback.

Chart 1

Chart 1

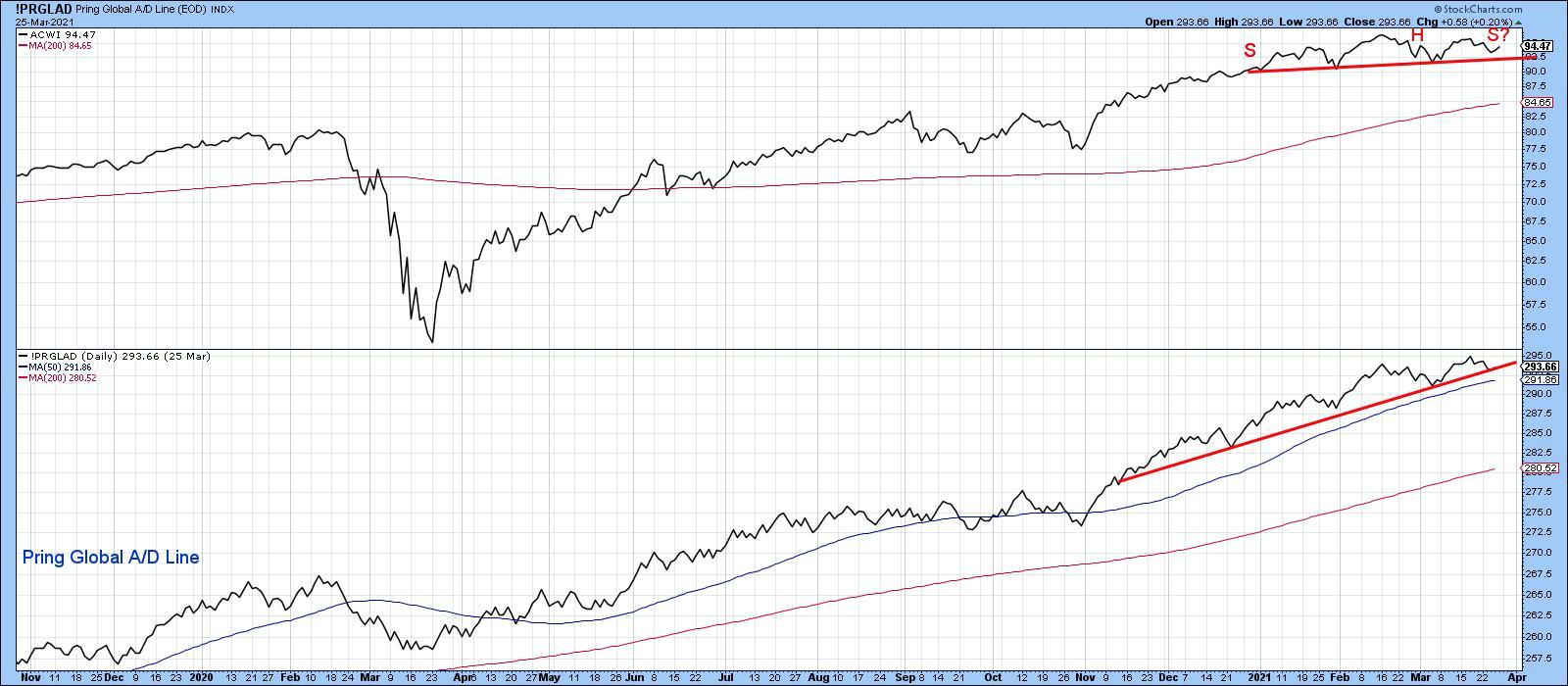

Chart 2 features the MSCI World Stock ETF (ACWI) together with my Global A/D Line, constructed from a universe of country ETFs. The ACWI itself may be in the process of tracing out a head-and-shoulders top, which would occur with a decisive daily close that can hold below $90.75. That’s not happened yet, so we should not jump the gun. However, if it does, the A/D Line would likely crack its November/March up trendline, thereby signaling further global weakness.

Chart 2

Chart 2

NYSE Composite at Key Support

Chart 3 compares the NYSE Composite to the 10-day MA of the number of NYSE issues trading above their 50-day MAs. The first thing to notice is that the NYSE is struggling to remain above its March 2020-21 up trendline. The good news is that it’s a fairly steep line and those kind of violations are normally followed by a consolidation rather than a reversal move. In other words, if it is decisively violated, we are likely to see a sharp but quick shakeout prior to a renewal of the bull market. Note the extended green trendline that joins the 2018 and 2020 highs. If a correction does take place, it’s likely to provide strong support.

Chart 3

Chart 3

The second thing to note is the fact that the oscillator in the lower window has been diverging negatively with the index since the beginning of the year and is also right at an up trendline. The numbers on the chart represent three previous instances where a trendline for both the price and oscillator were more or less simultaneously violated. The three examples were all followed by a correction of some kind.

Chart 4 compares the NYA to a 10- and 20-day MA of the NYSE Common Stock McClellan Volume Oscillator. The good news is that it is rapidly approaching an oversold reading. However, at the most recent high in the Index, the indicator was barely above its equilibrium level, which, when confirmed, is a sign of weakness. Two previous examples in late 2018 and January 2020 have been flagged by the dashed arrows. The confirmation came from two solid up trendline violations. The NYA is currently resting on a third line, but has not yet decisively violated it.

Chart 4

Chart 4

NASDAQ Leading the Way?

Chart 5 shows that the NASDAQ violated its 2020-21 up trendline some time ago and also experienced a break in a similar up trendline for its Bullish Percentage Index. The latter is now resting on the shallower dashed up trendline, further pointing up the critical nature of the short-term technical picture.

Chart 5

Chart 5

Clearly, none of these indicators have yet broken to the downside. However, these setups are so numerous that, if the breakdowns do materialize, a lot of traders could be temporarily caught on the wrong side of the market.

This is an updated version of an article previously published on Thursday, March 25th at 11:45am ET in the member-exclusive blog Martin Pring’s Market Roundup.

Good luck and good charting,

Martin J. Pring

The views expressed in this article are those of the author and do not necessarily reflect the position or opinion of Pring Turner Capital Group of Walnut Creek or its affiliates.