Marram Investment Management commentary for the fourth quarter ended December 31, 2020.

Q4 2020 hedge fund letters, conferences and more

Dear Investors,

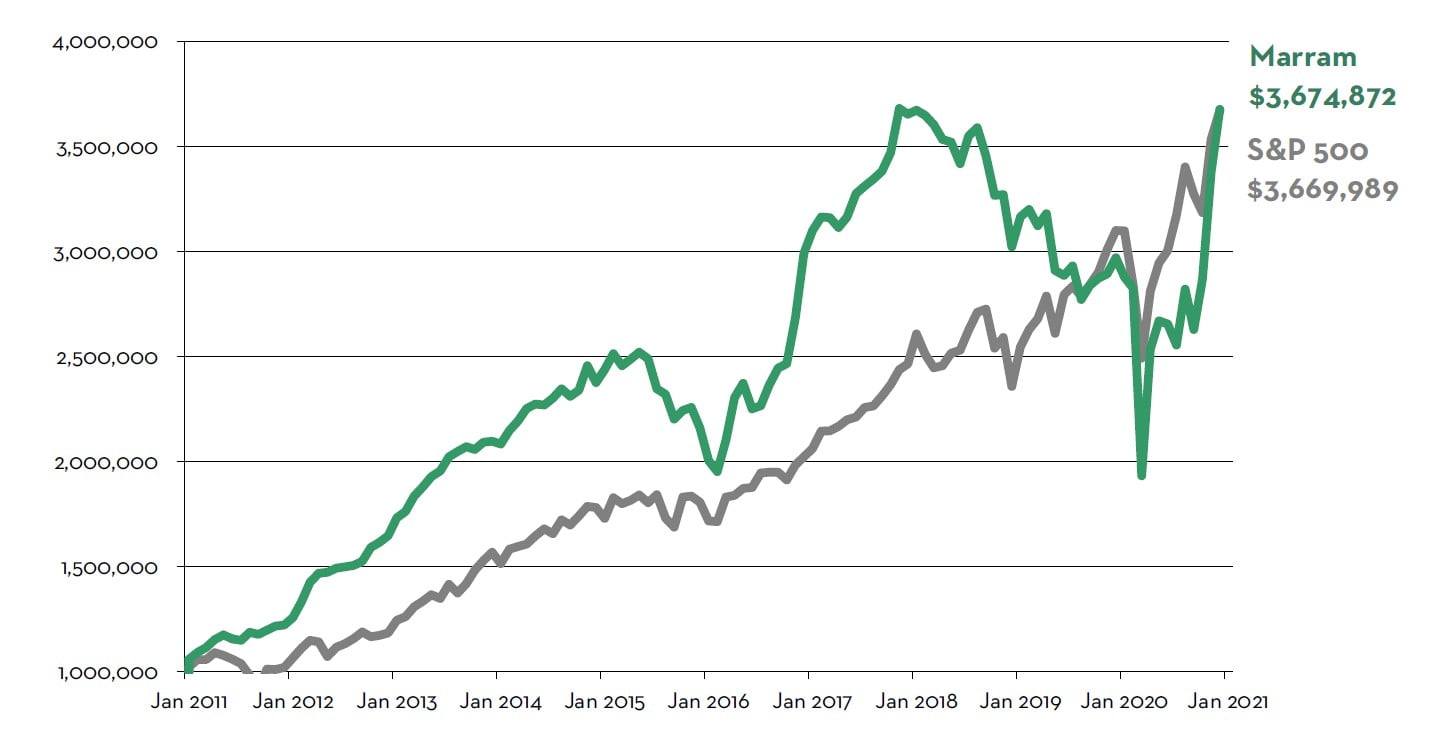

The Portfolio* returned +23.7% (net) in 2020. During this same period, the S&P 500 returned +18.4%.

Since inception, Marram has generated +267.5% cumulative return and +13.9% annualized return, net of fees, versus +267.0% and +13.9% for the S&P 500, respectively.

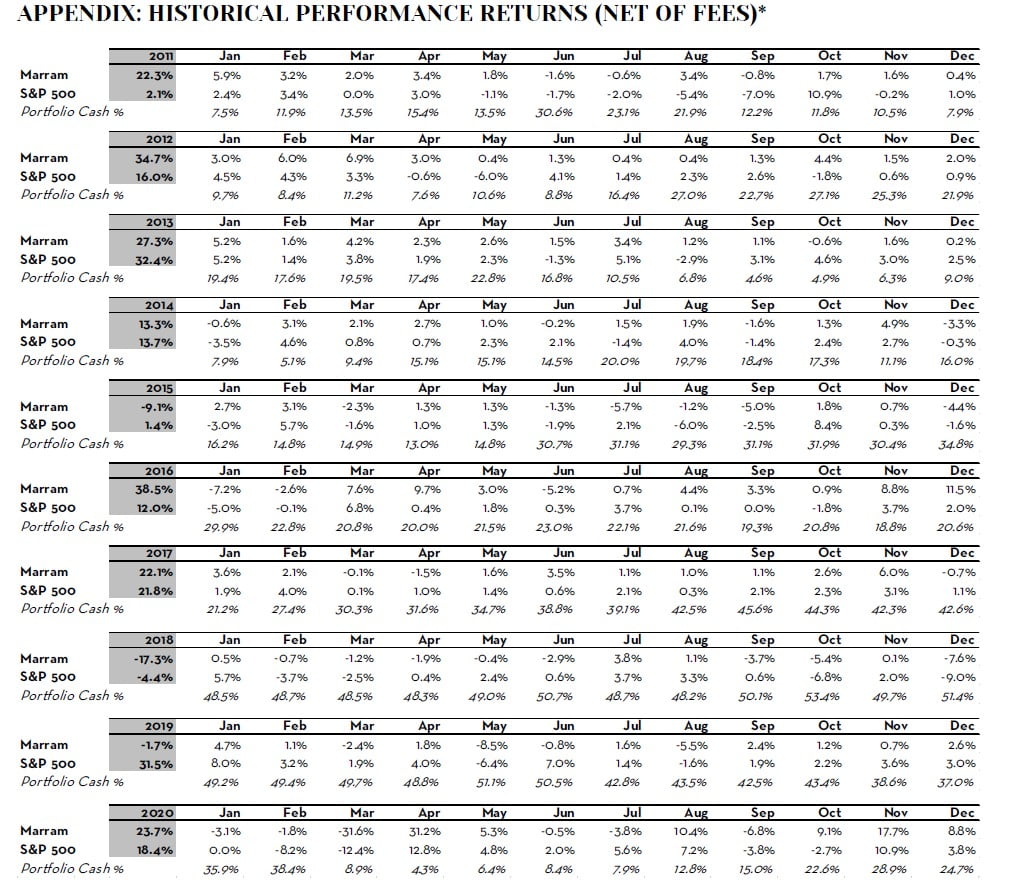

For monthly details, see Historical Performance Returns* at the end of this letter. Also, please refer to your separate account statement for exact account return figures.

$1,000,000 Investment in Marram vs. S&P 500 (Net Return, Inception to 12/31/2020)*

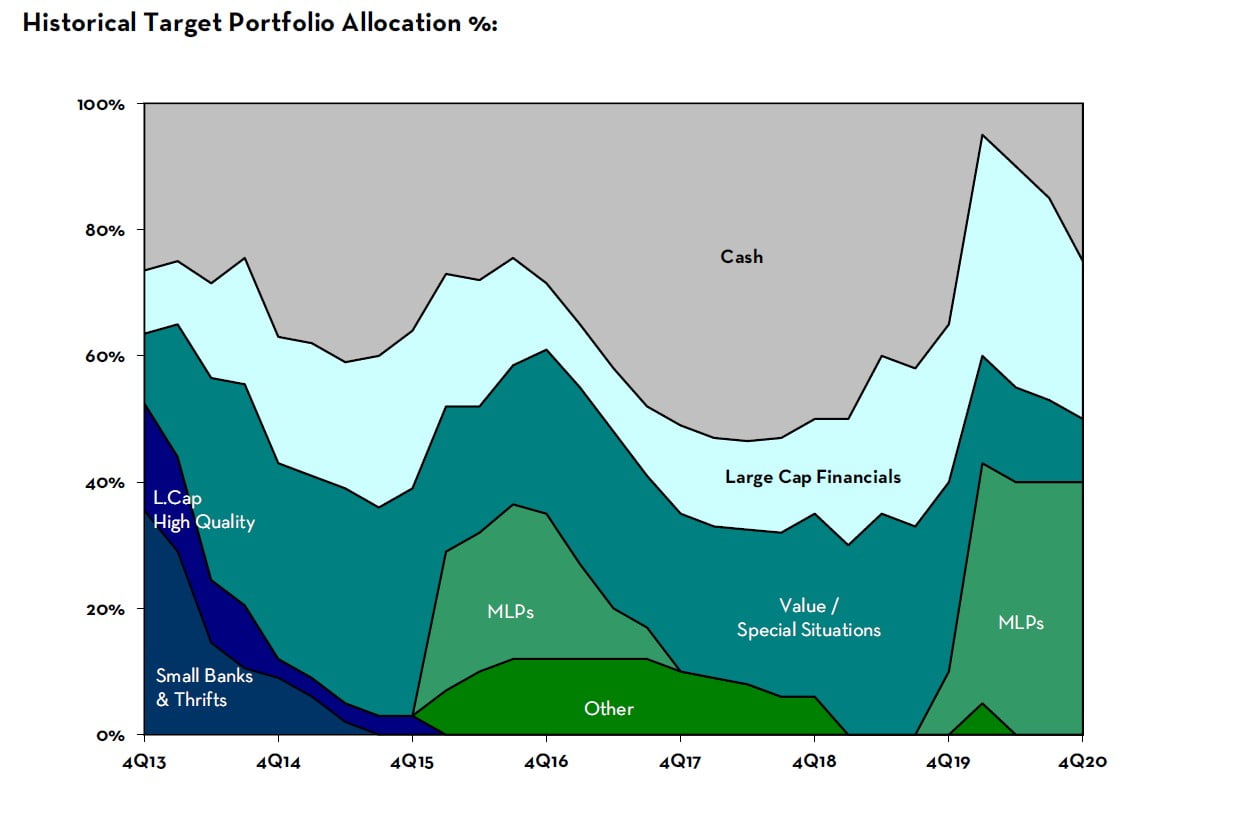

Marram’s Portfolio Allocations

Below is the target portfolio allocation – the optimal allocation as of the writing of this letter. Investor separate accounts may differ from this allocation due to changes in asset prices, availability to acquire/divest securities in the marketplace, margin & trading capabilities, tax considerations, etc. Over time, all investor separate accounts converge upon the target portfolio allocation.

-

Energy Infrastructure / Master Limited Partnerships (MLPs): 40% NAV

Energy infrastructure companies with assets indispensable to the smooth function of modern society. Commodity price volatility, shareholder turnover, forced selling, and uncertainty related to the long-term demand of fossil fuels have driven prices to extremely attractive levels. We have compiled a diversified basket of MLP securities valued on average at 9% NOI and 21% Cash on Cash, paying dividends averaging ~10% per year. See our 2019 4th Quarter Letter for a detailed discussion of our MLP investment thesis.

-

Large-Cap Financials: 25% NAV

Financial infrastructure companies whose services are essential to the smooth function of modern society. In recent months, investors (incorrectly) fearing a repeat of the Great Financial Crisis (“GFC”) of 2008-2009 fled the sector, driving prices down precipitously. We took the opportunity to increase our allocation. Strong capital ratios and high-quality loan portfolios mean we will not witness a repeat of the GFC. Annual normalized earnings of large banks will remain robust at ~11-12+% ROE even with low or negative interest rates, with additional uplift possible through adoption of technology and automation (lower personnel and real estate occupancy costs). Because we paid bargain prices averaging ~74% of book value (excluding CIT, which we divested during the quarter post sale announcement), we expect this basket will return ~14-16%+ annualized for many years into the future. See our 2020 2nd Quarter Letter (The Case For Large Banks) for a detailed discussion of our large bank investment thesis.

-

Value / Special Situations: 10% NAV

Public securities undergoing spin-offs, recapitalizations, restructurings, liquidations, etc. The share price performance of securities in this category are often not correlated with general market activity, but instead tied to the unique circumstance(s) embedded in each position. Because circumstances such as business strategy decisions take time to implement, and market participants require time to process the implications of these decisions, the timeframes necessary for securities to move from our purchase price to where we believe they are truly worth can range from months to multiple years, making for attractive but lumpy expected returns.

-

Cash & Cash Equivalents: 25% NAV

This category will fluctuate depending on attractive investment opportunities available in the marketplace. The weighted average dividend yield of our portfolio is ~4.5%, which will regularly replenish our cash balance.

Portfolio Return* Analysis & Future Positioning

The Portfolio* returned +39.8% (net) and +23.7% (net) during the 4th Quarter and in 2020, respectively.

In early 2020, as fear and panic dominated the marketplace, volatile price swings created incredible bargain opportunities. While others panicked, we were well-prepared and aggressively deployed our excess cash, purchasing durable, high-quality businesses trading at extremely discounted prices. Our portfolio cash balance shrank quickly from 35% of NAV at 12/31/2019 to less than 5% on 3/31/2020. Around that time, we sent two updates (on March 11th and April 23rd) urging investors to invest additional capital with Marram. Kudos to those who heeded our call! Since then, the portfolio has rebounded significantly, appreciating +37.4% in the 2nd quarter, flat in the 3rd quarter, then appreciating another +39.8% in the 4th quarter. In 2020, trough to peak, the portfolio rebounded approximately +90%.

By aggressively deploying cash at the depth of a panic into durable businesses at bargain valuations, we constructed a fortress portfolio that not only withstood the pandemic’s financial shocks, but also one that emerged profitable on the other side.

As the global economy recovers in 2021 with vaccination rollout and increased herd immunity, we expect greater human mobility, activity, and consumption. This will translate into higher profits for the businesses that we own. In other words, even after our strong performance in 2020, there remains a great deal of future upside potential in our portfolio of investments.

MLPs. With greater human mobility, activity, and consumption comes increased fossil fuel demand, supply production, and transportation volumes. Higher volumes, corporate cost rationalizations, and lower project capex mean our MLPs will generate higher cash flows and return more of it to shareholders in the years ahead. Our MLPs performed spectacularly in 2020, generating ~70% of 2020 gains. Even so, we continue to believe MLP prices are too low (the current valuation of our basket of MLPs average ~5x distributable cash flow), especially considering the tax-advantageous nature of MLPs (dividends are return of capital and not taxable until shares are divested).

Large-Cap Banks. We expect ultimate loan losses will be far less than 2020 provisions taken. Provision releases, cost rationalization, and scale advantages will boost earnings in 2021 and beyond. Our large banks also demonstrated the strength of their balance sheets by passing the Federal Reserve’s COVID-Scenario Stress Test with flying colors. In response, the Fed has lifted restrictions on return of capital. Buybacks have resumed. Most of the large banks we own have stated publicly that they have excess capital to return. We continue to believe large-cap bank valuations (currently ~1.0x book value) are too low given operating fundamentals.

RICK. All restaurants and many clubs are now open for business; some locations are hitting record sales volumes despite COVID. RICK is generating excess cash flow for either share buybacks, acquisitions, or organic buildout. The Company recently signed its first franchising agreement for Bombshells, a fast-growing bar & restaurant segment that has benefited from the closure of local competitors. Thanks to the superior ability of management to maneuver deftly through the storm, COVID may ultimately have a positive effect on RICK’s long-term ability to grow free cash flow per share – like the lone working shrimp boat after a Gulf hurricane in the movie Forrest Gump.

We had purchased more RICK shares at rock-bottom prices in March. The share price has since quadrupled from those lows, and we are actively trimming RICK to keep it a manageable size within our portfolio.

AINC. As we shared last quarter, although no longer a large position in our portfolio (currently ~3% of NAV) due to price decline, AINC was once a large position, and therefore deserves an update. Pre-COVID, AINC’s was steadily growing free cash flow per share. The onset of COVID has decimated worldwide travel and hotel demand. As a provider of services to the hotel industry, AINC’s operating fundamentals and share price experienced a severe setback. However, we have not sold our AINC shares. In fact, we have been actively purchasing more ~$5/share. At this price, the risk-reward is uniquely attractive. AINC is essentially an asymmetric call option, without an expiration date, on the recovery of the travel and hotel industry. Once an effective therapeutic/vaccine for COVID is widely available, hotel demand will rebound quickly as people and groups make up for lost trips, gather to celebrate postponed events (conferences, weddings, reunions, etc.), and corporations allocate office rent savings toward travel and teambuilding budgets to gather employees now working remotely.

Future Uncertainties

We usually refrain from macroeconomic commentary. However, that does not mean we are not aware of macro influences and entertain various future possibilities/risks when selecting investments and constructing our portfolio. After all, all investments, public and private, are legal ownership entitlements to profits and cash flows, and part of a larger interdependent social and political ecosystem. Any changes in government policies (monetary, fiscal, and regulatory) can have powerful consequences, and introduce new uncertainties into the economy, markets, and investment frameworks.

In our 2020 1st Quarter Letter, we predicted that “Idle hands are the devil’s workshop. Fearful, unemployed, and bored citizens are dangerous to incumbent governments.” Throughout history, mob formation is highly correlated with widespread unemployment and discontent with existing government policies. Hence, we were not surprised when protests erupted across the country this summer, and continue to this day.

To help put recent events into (historical) perspective, below are excerpts from a favorite book titled The Lessons of History by Pulitzer Prize-winning historians Will and Ariel Durant:

“Since practical ability differs from person to person, the majority of such abilities, in nearly all societies, is gathered in a minority of men. The concentration of wealth is a natural result of this concentration of ability, and regularly recurs in history. The rate of concentration varies (other factors being equal) with the economic freedom permitted by morals and the laws. Despotism may for a time retard the concentration; democracy, allowing the most liberty, accelerates it…In progressive societies the concentration may reach a point where the strength of number in the many poor rivals the strength of ability in the few rich; then the unstable equilibrium generates a critical situation, which history has diversely met by legislation redistributing wealth or by revolution distributing poverty.

In the Athens of 594 B.C., according to Plutarch, ‘the disparity of fortune between the rich and the poor had reached its height, so that the city seemed to be in a dangerous condition, and no other means for freeing it from disturbances…seemed possible but despotic power’ The poor, finding their status worsened with each year…began to talk of violent revolt. The rich, angry at the challenge to their property, prepared to defend themselves by force. Good sense prevailed; moderate elements secured the election of Solon, a businessman of aristocratic lineage, to the supreme archonship. He devaluated the currency, thereby easing the burden of all debtors (though he himself was a creditor)…he cancelled arrears for taxes and mortgage interest; he established a gradual income tax that made the rich pay at a rate twelve times that required of the poor…The rich protested that his measures were outright confiscation; the radicals complained that he had not redivided the land; but within a generation almost all agreed that his reforms had saved Athens from revolution…

After the breakdown of the political order in the Western Roman Empire (A.D. 476), centuries of destitution were followed by the slow renewal and reconcentration of wealth, partly in the hierarchy of the Catholic Church…the Reformation was a redistribution of this wealth by the reduction of German and English payments to the Roman Church…the French Revolution attempted a violent redistribution of wealth by Jacqueries in the countryside and massacres in the cities, but the chief result was a transfer of property and privilege from the aristocracy to the bourgeoisie. The government of the United States, in 1933-1952 and 1960-1965, followed Solon’s peaceful methods, and accomplished a moderate and pacifying redistribution…The upper classes in America cursed, complied, and resumed the concentration of wealth.

We conclude that the concentration of wealth is natural and inevitable, and is periodically alleviated by violent or peaceable partial redistribution. In this view, all economic history is the slow heartbeat of the social organism, a vast systole and diastole of concentrating wealth and compulsive recirculation.”

Pundits may blame left vs. right ideology, but American wealth inequality sits are the heart of what is eating away at social harmony. COVID will ultimately be remembered by future generations not for the tragic loss of life, but for broad public policy failures (and perhaps advances in medicine) that will reverberate for years to come. Lower income populations, already more likely to suffer from preexisting conditions like obesity and diabetes, experienced higher infection and mortality rates. They were also harder hit by job losses and disruptions to childcare access.1 The 2020 pandemic laid bare the realities of wealth disparity in America, which was accelerated in recent years fueled by the Fed’s massive monetary stimulus (quantitative easing) and corporate tax cuts in 2016, both disproportionately benefiting the wealthy existing owners of assets.

To be clear, we are not asserting that redistributive policies, aimed at addressing wealth inequality in America, are presently coming down the legislative chute. But American wealth disparity is an important theme that has, and will continue to influence future policy debates, with the potential to introduce great uncertainties into the economy, markets, and investment frameworks. (We sincerely hope the events of 2020-2021 will propel moderate elements and individuals with good sense off the sidelines and into public service, to take active roles in policy making at all levels of government: community, regional, and national.)

Come what may, our portfolio is well-positioned to weather future uncertainties:

- Our large-cap banks have operated (profitably) under heavy regulatory scrutiny for over a decade.

- The tax advantageous structure of our MLPs offers protection against corporate and personal tax rate increases.

- We own durable and profitable businesses trading at undemanding valuations.

- Our portfolio cash balance has been replenished by dividends and harvested gains.

We stand poised to strike should future uncertainties create new opportunities. We look forward to

continuing our capital compounding adventures in the years ahead.

As always, thank you for your trust. We wish everyone a happy and healthy 2021.

Yours very truly,

Vivian Y. Chen, CFA

Portfolio Manager

Marram Investment Management LLC

About Marram

Marram is an outsourced long-term investment solution focused on growing wealth for retirement or legacy purposes. We began as a service for a small circle of friends and family. Our investor friendly fee structure (lower than most hedge funds), terms (separate accounts, no lock-up), and high standards of care and excellence, reflect those origins. Our portfolio manager has the majority of her family’s liquid net worth invested in the same strategy – we eat our own cooking – ensuring that we shepherd your investment with the utmost care, as we would our own.

The post Marram Investment Management 4Q20 Commentary appeared first on ValueWalk.