The recovery from the COVID Crash has helped to boost lumber futures prices up to challenge the record high made in 2018. That peak in 2018 came about when the U.S. government imposed “softwood lumber” tariffs on Canadian imports, an action resulting from a long running complaint to the WTO, which that body decided in favor of the U.S.

This time, the rapid rise is happening because mills have experienced workforce shutdowns due to COVID, and a simultaneous increase in demand for new home construction. Part of that is the maturing of the “echo boom” generation of young adults who were born around the 1990 births peak and who now want to own their first home. Another part of the rise in housing demand is the flight of city-dwellers out of dense metropolises and toward the suburbs, where the COVID risk is supposedly lower and where they can hopefully find a home with space for a home office.

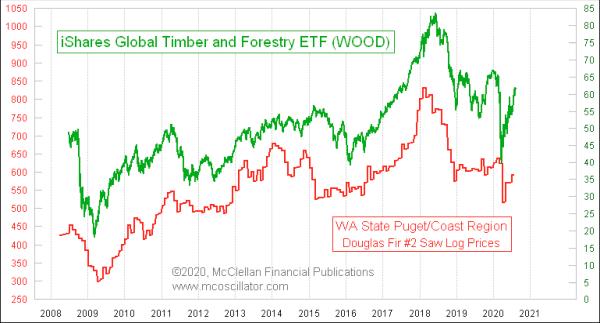

The curious insight in this week’s chart is that, even though lumber futures prices are zooming, the price of timber (i.e. unprocessed logs) is just barely back up to the lows it made in 2018-19. Data source: DNR.wa.gov.

The implication is that, even though the mills are getting paid handsomely for their finished product going out the gate, those mills are not bidding up prices for their own raw materials. There are reports that mills have plenty of inventory of logs to process, so they don’t need to scramble to get more logs in so that they can fill their orders. So it is a squeeze at just one end of the process, as opposed to a general boom time for the timber/lumber industry as a whole.

The spread between log prices and lumber prices shown in this week’s chart is great news if you are running a mill, but not so great if you own raw timberland. The tree farmers are not benefiting much (yet) from the big rise in lumber prices. It could be that timber’s response is just being delayed slightly and, eventually, it will catch up. But, generally speaking, the two price series move in unison and without a lag.

If you as an investor want to try to take advantage of this big spread between raw material and finished goods prices, all you have to do is buy a sawmill. If you do that, then you can also get the additional side benefit of broadening your understanding of all of the different federal, state and local laws about labor, inventory storage, environmental protection, OSHA, trucking and many other fascinating fields of study.

You could try to own a mill as just a shareholder, but unfortunately the opportunities for that in the U.S. stock market are pretty limited. Most of the major producers like Weyerhaeuser, Georgia Pacific or Canfor are fully integrated with both sawmills and timberland assets. There are almost no pure play sawmill company stocks for investors to pile into.

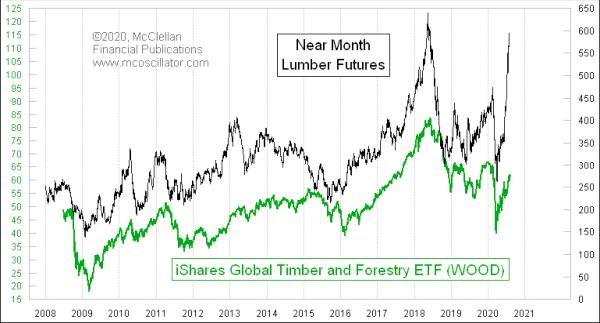

ETF investors can participate in this industry through products like WOOD (iShares) and CUT (Invesco). This next chart compares WOOD’s share prices to lumber futures.

It is clear that there is a correlation there, but it is not as good of a correlation as we might like. That is because most of the holdings of WOOD have exposure more to the timber production part of the industry than to the lumber processing end. We can see that better in this next comparison:

In this chart, it is pretty clear that the share price of WOOD moves in sympathy with timber prices and matches the magnitudes of those movements. That might still be what an investor wants if he thinks that the prices for timber and timberland holdings might rise in the future. But it is not a way to play the current large spread between log prices and 2×4 prices.