Logica Capital commentary for the month ended July 2020 discussing the S&P 500‘s announcement of dividend futures on the CME.

Q2 2020 hedge fund letters, conferences and more

Logica Absolute Return – Up/Down Convexity – No Correlation

Logica Tail Risk – Max Downside Convexity – Negative Correlation

July 2020 Performance*

- Logica Absolute Return -0.03%

- Logica Tail Risk -1.43%

- S&P 500 +5.89%

- VIX -5.97 pts

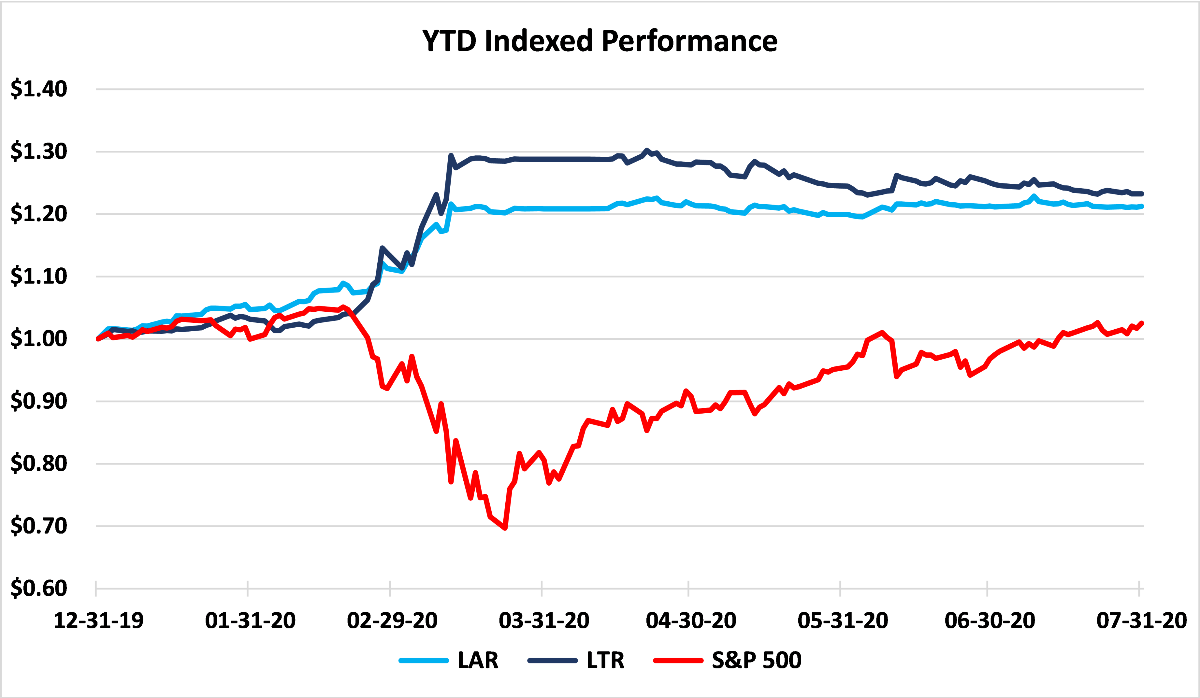

Year To Date Performance*

- Logica Absolute Return +21.25%

- Logica Tail Risk +23.15%

- S&P 500 +2.49%

*Returns are Gross of fees to illustrate strategy performance.

Logica Absolute Return Fund, LP returned -0.15% (net) for July 2020

“I’ll never be your beast of burden

My back is broad but it’s a-hurting”

– The Rolling Stones, 1978

The Burden of Carry…

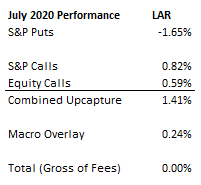

This month continued to be a challenging one for long volatility strategies as the term structure in equity volatility returned to one of the steepest levels (UX futures point spread) in the past decade and volatility contracted yet again. Ultimately this raises the carrying costs of equity options as they decay in both vega (implied volatility) and theta (option time decay) which collectively must be offset by manager generated alpha. We came very close this month, but ultimately the carrying costs of our downside capture ATM S&P puts offset gains in our Up Capture and Macro Overlay components, leaving us almost perfectly flat for the month:

The good news is that another month of aggressively negative conditions for long volatility has passed and our warehouse of downcapture options is slowly filling back up. We exited July with our “warehouse” roughly 75% full, increasingly ready for whatever shock comes next (election woes, anyone?).

Conditions in Place for Lower Volatility?

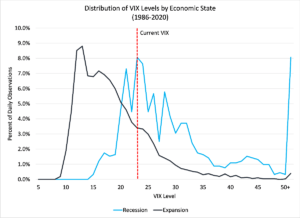

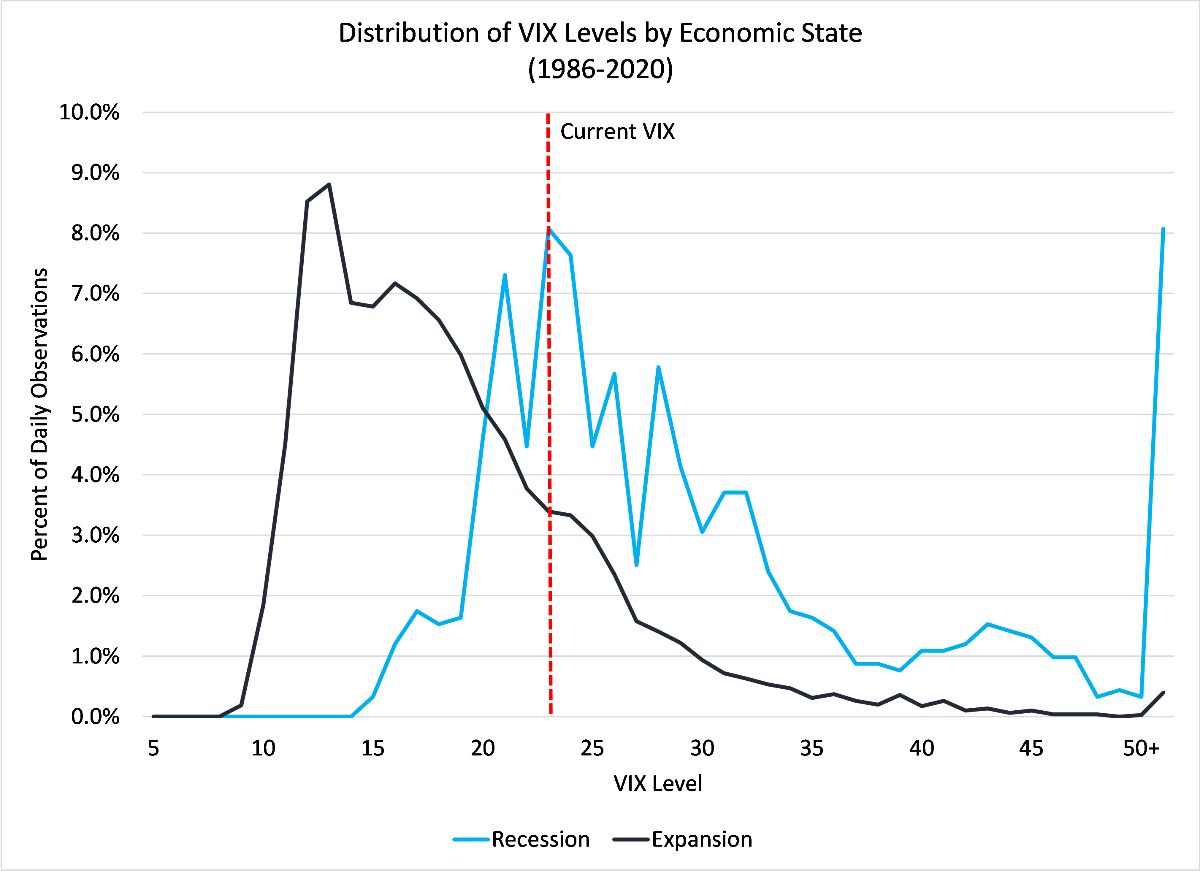

Volatility has certainly earned its stripes in the past six months. From a low of 11.75 in January to a peak of 86 in March and back to a current level of ~23, it’s been a wild ride. While it is hard to remember a period when the VIX maintained its current levels around 23, this is in large part due to the extended period of economic expansion following the GFC. If we disaggregate the distribution of the VIX into “Recession” and “Expansion” based on NBER designation, the current VIX level is exactly the mode of recessionary levels.

Another way of considering the current equity volatility environment is by peering into duration. Despite being a year in which we have seen record declines (depth + speed) and record rallies (extent + speed), 2020 barely registers in the duration of elevated equity volatility. As can be seen in the below chart, it would be unusual (but not unprecedented) for this first volatility event to be isolated. In other words, it is likely that we ain’t seen nothing yet.

“He’s never caught one spy untold,

He’s never even caught a cold,

Got his degree from Disney Land,

But he’s the last of the secret agents

And he’s my man”

– Nancy Sinatra, The Last of the Secret Agents, 1967

Secret Agents, Man…

One of the reasons markets have felt so disconnected from our day to day experience in the CoV-19 shut down economy is that we continue to see the gains coming in the nighttime session. Since June 8th (the Powell “60 Minutes” interview), while the S&P 500 is up 1.5% in aggregate as of July 31st, the source of those gains has been radically split. Overnight we have marched upwards while during the day we have headed lower.

We have discussed this dynamic previously and do not want to beat a dead horse, but it is important to understand that something clearly changed in the fall of 2015.

The evidence continues to point towards structured products flowing out of Europe and Asia. A good article that highlights the dynamics of these yield enhancement products, particularly around the March 2020 events can be found here: https://www.straitstimes.com/business/invest/billions-lost-in-structured-notes

And an important quote from the article:

“Investment banks make money from structuring the notes and try to manage their exposure by passing the risk to other parties.”

The mechanics of this are important in understanding the tell-tale sign of derivative driven behavior. When a market that has historically delivered volatility consistent with natural buyer/seller behavior begins to show extremely low volatility, high Sharpe behavior (think S&P 500 in 2017 or S&P overnight since early April), it is often a byproduct of delta and gamma hedging. Volatility compression does not occur naturally.

Another important clue comes from a quiet CME Group announcement in Oct 2015:

CHICAGO, Oct. 16, 2015 /PRNewswire/ — CME Group, the world’s leading and most diverse derivatives marketplace, today announced the launch of S&P 500 Annual Dividend futures and S&P 500 Quarterly Dividend futures. These new contracts will be available for customer trading as of November 16, 2015, pending certification of contract terms and conditions with the CFTC and completion of all regulatory review periods.

http://investor.cmegroup.com/news-releases/

Why would the announcement of dividend futures on the CME matter? Because dividends are typically a surplus in price-linked structured products. If the payout of a structured product references the price of an index (normal), rather than a total return (abnormal), the hedging of future dividend streams becomes an important source of profit for the issuing bank. But as market volatility rises, it becomes increasingly important to hedge out these exposures — volatility can swiftly turn sources of profit into sources of risk. A 2018 white paper from Sarita Bunsupha at Harvard highlights this dynamic:

“In particular, equity derivative products are major sources of dividend supply shocks, resulting in the variation in implied dividends across time and across equity indices. Using issuance data, we show that the implied dividend term structures for major equity indices respond to structural flows from equity structured product issuance.” – Bunsupha et al 2018

So do we see any indication that S&P dividend futures behaved differently than the S&P? Why yes we do… dividend futures were unaffected by the early sell-off, but as hedging needs arose due to index price declines the S&P Dividend futures became increasingly offered. Interestingly, if we match them up next to the overnight action, it certainly seems that we have identified our motivated players.

This potential relationship raises the frightening prospect that S&P price behavior is not at all linked to the economics of the Corona Virus economy, but rather the risk hedging activities of investment bankers. Not to worry, those investment banks have it under control. SocGen, for example, won “Structured Products House of the Year” in 2019:

“Societe Generale has managed to not just hold its own but also come up with ideas that helped customers switch products in line with the market tide and create solutions that reduced risk… ‘Today, we offer a very diverse offering to our clientele,” says Thomas Decouvelaere, head of structuring for Asia-Pacific at Societe Generale. “We have pioneered successful products across not just equities but fixed income too. We now show our clients 10 structures every day versus one or two a few years ago.”’” Risk.Net Magazine, September 2019 (2)

And obviously the arrow of progress only moves in one direction. Things can only get better as an update informs us:

“After Stunning Losses, SocGen, Natixis Clear Out Executives… At the heart of the French banks’ woes is their embrace of structured products, multilayered synthetic securities linked to stocks and bonds that are popular among retail investors. While they can be far more lucrative than more straightforward trading businesses, they are notoriously volatile.” – Bloomberg, Aug 4, 2020

As the French might say, “Chien chaud!”

“Don’t get too comfortable up in the sky

Your mistakes, they all come with a price”

– We Came As Romans, Tear It Down, 2015

An Update on the Flying Wallendas

Last month we discussed the dynamics of the rebalancing of Target Date Funds. This has begun. As we discussed with several of our investors, the largest dynamic in play is the rebalance into Inflation Protected Bonds. The largest of Vanguard’s TDFs began the process adding 1% into the TIPS market (and likewise beginning to sell equities).

Much like the discussion around structured products in Asia, it is worth asking whether the bid in inflation breakevens (positively correlated with demand for TIPS) might be a byproduct of something other than inflation expectations:

Again, this is fine… it’s not like anyone is seriously considering that rising breakevens convey fundamental information… whoops…

Beveridges All Around

Over the next few days, we’ll start to get the first fundamental pieces of employment information after the relaxation of Paycheck Protection Program (PPP). One of the pieces of information we will be tracking closely is the “Beveridge Curve”, named after William Beveridge. While many economists discuss the Phillips Curve, the putative relationship between Inflation and Unemployment, a strong case can be made that the relationship that really matters is the relationship between Job Openings and Employment. The speed of the employment collapse since March 2020 is unprecedented in modern economics and it has been most interesting to see a recovery in small businesses claiming hardship in filling job openings. After a brief and modest decline, “Jobs Hard to Fill” from the NFIB survey of small businesses turned back up. As we had expected in March with our Policy in a World of Pandemics piece, we have begun to see concern from politicians that the “overly generous” unemployment benefits are keeping Americans from returning to work now that risk markets have returned to highs. Clearly, it will be important to monitor the trend in job openings alongside the reported unemployment rate.

As a comparison, in 2008, we saw a significant decrease in job openings that matched the increase in the unemployment rate. This time, the current level of job openings suggests a sub-4% unemployment rate. While this seems impossible to imagine given the consistent flow of headlines on permanent business closings (https://www.marketwatch.com/story/41-of-businesses-listed-on-yelp-have-closed-forgood-during-the-pandemic-2020-06-25), it is theoretically possible that the bump in household incomes have resulted in many new business opportunities to replace those that have gone. Amazon drivers may have replaced waiters. Only time will tell. In the meantime, you deserve a beverage for making it through yet another Logica monthly letter

Business Update – Logica Absolute Return Offhsore Fund

Logica will be introducing an offshore version of the Logica Absolute Return Fund in the next few months. If you are an offshore eligible investor currently in our onshore vehicle, we will be reaching out to gauge interest in transferring. If you are a new investor interested in our offshore vehicle, please contact Steven Greenblatt for subscription documents.

Logica Strategy Details

Note: We have comprehensive statistics and metrics available for our strategies, but only include a select few to highlight what we believe is our most valuable contribution to any larger portfolio.

- If you would like to learn more about our strategies, please reach out to Steven Greenblatt.

- If you would like to speak with Wayne or Mike on their views on Hedge Funds/Investing/Trading and trends they see shaping the industry, please contact Steven Greenblatt at greenblatt@logicafunds.com or 424-652-9520.

Follow Wayne on Twitter @WayneHimelsein

Follow Michael on Twitter @ProfPlum99

See the full article in PDF format here.

The post Logica Capital July 2020 Commentary appeared first on ValueWalk.