Logica Absolute Return Fund commentary for the month ended December 2020.

Q3 2020 hedge fund letters, conferences and more

- Logica Absolute Return – Up/Down Convexity – No Correlation

- Logica Tail Risk – Max Downside Convexity – Negative Correlation

December 2020 Performance*

Logica Absolute Return +0.4%

Logica Tail Risk -0.6%

S&P 500 +3.3%

VIX +2.2 pts

Year To Date Performance*

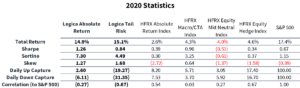

Logica Absolute Return +14.9%

Logica Tail Risk +15.1%

S&P 500 +17.4%

*Returns are Gross of fees to illustrate strategy performance.

Logica Absolute Return Fund, LP returned +0.13% (net) for December 2020

Summary: Equity markets continued their strong performance in December, but volatility found a floor which contributed to positive returns for the month. Markets bear an increasing resemblance to late stage 1999, with total short interest outstanding nearing record lows.

“Just the facts, Ma’am”

As discussed below, we continue to believe markets are fragile and expensive. While short covering and optimism continues to drive increasingly inelastic markets higher, we continue to carry a sizeable Put load with a recognition that protection is both necessary and difficult to find.

“The first step towards getting somewhere is to decide you’re not going to stay where you are.” – J.P. Morgan

All of us at Logica hope that you, your colleagues, and your families remain healthy and optimistic for 2021. We wanted to take this opportunity to express our gratitude at your interest in our work and bring you up to date on our accomplishments over the last year.

2020 started with the launch of Logica Absolute Return as equity markets around the world accelerated to new all-time highs and a long volatility approach appeared to make little sense. In March, that narrative was challenged, and the utility of long volatility became obvious. In that confusing time, we made a novel statement:

“If we are right and we are unlikely to see substantive changes to the market structure, then the unavoidable conclusion is that markets could aggressively reprice higher as money flows into passive strategies; this becomes particularly true if the United States is engaged in a pattern of aggressive stimulus… As substantive changes are not likely to be made, we are forced to expect more of the same.” Policy in a World of Pandemics, March 26, 2020

This observation turned out to be truer than even we could have forecast, with global markets rapidly returning to their pre-Covid trend lines and exceeding them to a near record degree:

Ironically, while our broad forecast panned out, the degree to which the recovery exceeded expectations, and the related rapid decline in volatility alongside the market’s violent recovery, opened the door to a challenging summer for long volatility investing. Who would have known that a best possible period, immediately followed by a worst possible period, would mark our Fund’s first year out of the gate!

From our perspective, this was altogether a positive, giving us both the opportunity to shine where we do our best — market implosions — and get better at navigating these challenging markets. As we highlight in this letter, we do not believe that the events of early 2020 will be unique.

“Enthusiasm just creates bubbles; it doesn’t keep them from popping..” – Adora Svitak

As 2020 gave way to 2021, we managed to find a bit of a floor in equity volatility which set the stage for a modest gain in the month of December. This is obviously welcome. However, we continued the unusual pattern of VIX up, S&P up. While overall, 2020 maintained the pattern of negative correlation between the VIX and the S&P 500, relative to its 40-year history this was certainly an extreme year.

In fact, 2020 was the first year since the aftermath of the DotCom bubble and the restructuring of the S&P 500 from market-cap weighted to float-weighted (which eliminated unintended excess buying of stocks with high levels of insider ownership) in which we saw a sustained pattern of elevated volatility created by higher single stock volatility rather than correlation spikes. While single stock volatility began to rise in 2017, setting the stage for the XIV implosion in February 2018, 2020 has sustained these unusually high volatility levels. Like the 1998-2000 time period, we have seen an unprecedented increase in valuations which has extended further into the end of 2020. Starting valuations in 2021 are the highest in recorded history.

In a further nod to the 1998-2000 allegory, we have seen a strong bias towards larger, higher quality companies (e.g. AAPL, MSFT, etc) give way to an enthusiasm for small, more speculative companies that represent “the future.” Prior periods of rapid recovery of small stocks versus their style equivalent large brethren have not been particularly favorable for a continuation. The possible exception of December 2016 is worth noting.

Does the Rise in Passive Investing Contribute to this?

A recently released whitepaper by Hao Jiang of Michigan State University provides a clue why this occurs:

In this paper we study theoretically and empirically how the growth of passive investing impacts stock prices…Flows raise disproportionately the prices of large capitalization stocks in the S&P500 index relative to the prices of the index’s small stocks… an increase in the measure of non-experts, which triggers asset purchases, generates a larger percentage price increase for the assets in high noise-trader demand. An increase in the measure of non-experts that is accompanied by an equal decrease in the measure of experts generates an even stronger effect in the same direction.

The relationship between noise-trader demand, volatility and price impact is easiest to understand in the case where an asset is in such large demand that experts must short it in equilibrium. A positive shock to the asset’s expected dividends causes the asset’s price to rise. The experts’ short position thus becomes larger and carries more risk. As a consequence, experts become more willing to unwind their position and to buy the asset. Their buying pressure amplifies the price rise, resulting in high volatility per share.

Jiang, Vayanos and Zheng, December 2020

In other words, a positive shock to expected dividends, e.g. a COV-19 vaccine, results in aggressive short covering of riskier and shorted positions that causes prices to rise much more than would be expected in a non-passive index dominated environment – a perfect explanation for the behavior we have seen since the dramatic stimulus introduced in March 2020. However, once the short covering has been completed, the demand for these “non-expert/noise trader” dominated stocks deteriorates and the passive forces reassert themselves. Current short interest is near the lowest on record after nearly $275B of shorts have been covered in the last nine months.

Perhaps it is different this time, but with the incoming Biden administration looking to expand access to low-cost passive investing (including a potential reintroduction of the DoL Fiduciary Rule and, stunningly, a consideration of a required “financial literacy test” for workers to opt out of Target Date Funds), we remain skeptical.

“When much is taken, something is returned.” – Terry Pratchett, Nation, 2008

With the upcoming inauguration of Joe Biden as President of the United States and the Democrat sweep of Georgia, the markets are focused on the ideas of stimulus sweeping the nation. We think it is worthwhile considering the opposite. In March 2021, for the first time since December 2018, we see a confluence of events that create the potential for a significant outflow from equity markets. Like March 2000, we have seen a year of extraordinary gains for many investors in both speculative options and speculative assets like Bitcoin. On options, the introduction of commission-less trading on platforms like Robinhood have led to an explosion of short-dated trading that is taxable at ordinary income rates. Hopefully, none of our investors took their profits on Bitcoin, but the gains here become taxable as well. An informal Twitter poll conducted in late December 2020 suggested that roughly 73% of the investors polled were letting their winnings ride and roughly half had banked profits to pay taxes.

2021 faces not only a significant tax bill for many investors as of April 15th, but we also see the return of Required Minimum Distributions from 401Ks and IRAs. The SECURE Act of 2019 was signed into law in December 2019 and pushed the age for mandatory distributions from 70.5 to 72. This created a roughly eighteen-month window during which aging Baby Boomers were not required to sell from their retirement accounts. March 2021 will be the first required selling since March 2019. Fortunately, this is a minor period where only those who turned 72 in 2020 will be required to take their first distributions. A second distribution occurs in Dec 2021. Both of these periods represent potential net distributions of equities, but the confluence of the March RMD with potential tax selling is certainly worth keeping in mind as market participants grow increasingly giddy with the prospect of stimulus.

2020 – A Breakout Year for Logica

Against a work-from-home backdrop, we were able to proceed with our growth strategy, introducing our first commingled product, the Logica Absolute Return Fund, on April 1st, 2020. The onshore fund was complemented by our offshore variant, Logica Absolute Return Offshore, on November 1st. Firm assets under management have grown rapidly, and as we exit 2020 we have successfully met our short-term goal of growing assets above $100MM, a level that has allowed us to begin making significant investments for product enhancement and infrastructure improvement.

Notable 2020 Achievements

- Launch of LAR and LARO LPs

- AUM growth from $15MM to >$100MM

- New additions to Logica Team – in addition to Michael Green joining us as Chief Strategist in January, we are excited to add Joe Tagliaferro as our Chief Operating Officer and Jeff Press as our Chief Compliance Officer

- Successfully navigated the effect of lockdowns – Logica was able to execute our remote location and disaster recovery protocols and execute against both ongoing business dynamics and growth objectives

Logica in the news

- Since the introduction of Logica Absolute Return, Logica has been privileged to appear in several publications and podcasts. A list of podcasts are available on our website for those with interest.

- Our website traffic has risen from negligible in 2019 to nearly 220,000 unique visits in 2020

- Our most popular research piece, Policy in a World of Pandemics, was downloaded over 17,000 times

- Our white paper “The Illusion of Skill” has been viewed or downloaded over 4,000 times

R&D advances

- Introduction of Logica Absolute Return which extends the Logica strategies from our down-capture focused product to a vehicle capable of capturing market upside as well as downside

- Introduction of “anti-momentum” module (LFB) which added to LAR return for 2020 vs baseline models

- Revisions to the Logica process to better capitalize on increased implied volatility associated with single stock earnings associated with our momentum module (LFT)

- Improved diversification versus traditional momentum factors with a new module built to capture complementary factor exposures (LFD)

- Improved handling of volatility contraction environments with a toggle between single stock call options and index call options tied to implied correlation insights

- Improved capital utilization through integration of futures contracts and options on futures with Logica’s core securities modules

- Increased robustness and depth of our testing framework, resulting in faster and more efficient innovation.

Objectives for 2021

- SEC registration to complement Logica’s existing registration with the state of California

- Continued team build out and AUM growth

- Full deployment of 2020 research insights

- Continue to provide competitive performance

- Return to the office!

Again, thank you for joining us on this adventure and we look forward to an exciting 2021.

Business Update – Logica Absolute Return Offhsore Fund

As previously discussed, Logica has launched the offshore version of the Logica Absolute Return Fund. We are thrilled to announce our first institutional relationships underpinning this launch and look forward to an increasingly favorable environment.

Notes:

- Tracking Biased Weights: Asset Pricing Implications of Value-Weighted Indexing, Jiang et al https://personal.lse.ac.uk/vayanos/WPapers/TBWAPIVWI.pdf

Logica Strategy Details

Note: We have comprehensive statistics and metrics available for our strategies, but only include a select few to highlight what we believe is our most valuable contribution to any larger portfolio.

- If you would like to learn more about our strategies, please reach out to Steven Greenblatt.

- If you would like to speak with Wayne or Mike on their views on Hedge Funds/Investing/Trading and trends they see shaping the industry, please contact Steven Greenblatt at greenblatt@logicafunds.com or 424-652-9520.

- Follow Wayne on Twitter @WayneHimelsein

- Follow Michael on Twitter @ProfPlum99

Logica Absolute Return

2015-2019 stats & grid, reconstitution of live sub-strategies normalized to 16% annualized volatility

2005 to present growth of $1000 chart, simulation

Jan 2020 live with partner capital

Logica Tail Risk

2015-2019 stats & grid, reconstitution of live sub-strategies normalized to 16% annualized volatility

2005 to present growth of $1000 chart, simulation

Jan 2020 live with partner capital

The post Logica Absolute Return Fund December 2020 Commentary: “Just the facts, Ma’am” appeared first on ValueWalk.