While the FHA’s “official” monthly loan performance report for August is not yet available on its website, data from the FHA’s Early Warning System indicates that FHA’s Early Warning System indicate that the serious delinquency rate on FHA-insured single-family loans increased to above 11% in August, an all-time monthly high.

Delinquency rates in the EWS do not match those in the official report, but the two delinquency rates tend to move together over time.

| Delinquency Rate, FHA-Insured SF Loans Official Report |

||||

|---|---|---|---|---|

| Total | 30-day | 60-day | SDQ | |

| 2/29/2020 | 10.85% | 5.16% | 1.65% | 4.04% |

| 3/31/2020 | 11.17% | 5.59% | 1.61% | 3.97% |

| 4/30/2020 | 15.52% | 9.20% | 2.28% | 4.04% |

| 5/31/2020 | 17.27% | 6.37% | 5.99% | 4.91% |

| 6/30/2020 | 17.41% | 4.74% | 3.71% | 8.96% |

| 7/31/2020 | 17.24% | 4.15% | 2.51% | 10.58% |

| Early Warning System, Active Servicers | ||||

| 2/29/2020 | 10.63% | 5.16% | 1.66% | 3.81% |

| 3/31/2020 | 10.74% | 5.36% | 1.62% | 3.76% |

| 4/30/2020 | 15.32% | 9.17% | 2.27% | 3.88% |

| 5/31/2020 | 17.15% | 6.37% | 5.99% | 4.80% |

| 6/30/2020 | 17.17% | 4.65% | 3.70% | 8.82% |

| 7/31/2020 | 17.04% | 4.05% | 2.55% | 10.44% |

| 8/31/2020 | 17.43% | 4.07% | 2.20% | 11.17% |

The official Loan Performance Trends Report includes delinquency data for various subcategories, including (Fiscal) Year “Cohorts. Here are some SDQ data by Fiscal Year endorsement.

| FHA SF Serious Delinquency Rate by Fiscal Year1 Cohort | |||

|---|---|---|---|

| 7/31/2020 | 2/29/2020 | 7/31/2019 | |

| All | 10.58% | 4.04% | 3.78% |

| 2015 | 11.65% | 4.54% | 4.07% |

| 2016 | 11.31% | 4.04% | 3.49% |

| 2017 | 11.79% | 4.00% | 3.15% |

| 2018 | 13.14% | 4.32% | 2.49% |

| 2019 | 12.13% | 1.92% | 0.42% |

| 2020 | 5.09% | 0.08% | |

| 1October of the previous to September of the current year | |||

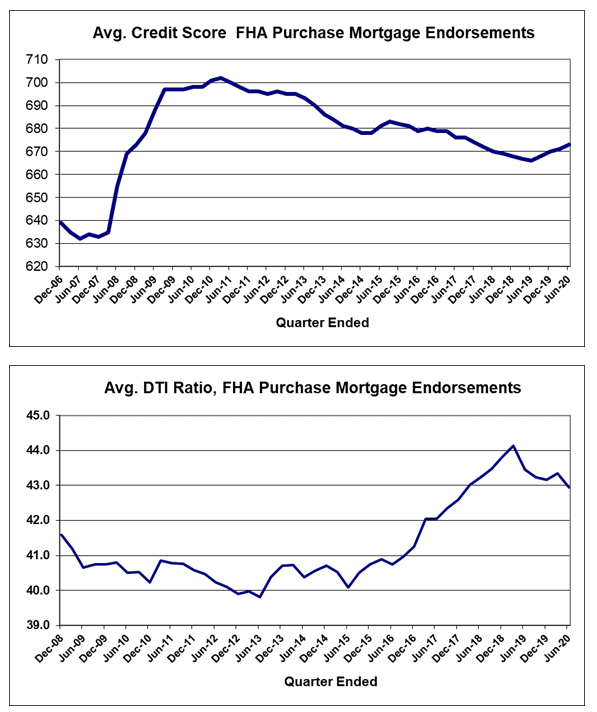

Click on graph for larger image.

Click on graph for larger image.

What is striking about these data is that the years with both the largest increases in SDQ’s and the highest SDQ levels were the 2018 and 2019 “cohorts.” These two years were relatively risky books of business, with lower average credit scores compared to the previous 10 years and substantially higher (and never before seen) average debt-to-income ratios than in the previous 10 years.

The surging FHA serious delinquency rate obviously reflects the huge increase in the number of FHA borrowers adversely impacted by the pandemic’s effect on the economy, and most of these seriously delinquent borrowers are in a FHA loan forbearance program. Given this program, combined with the current moratorium on foreclosures, the surging SDQ does not augur any imminent increase in foreclosures.

It does, however, highlight that a sizable number of homeowners (and, presumably, potential homeowners) have been adversely impacted financially by enough to be unable to make their mortgage payments.

This observation, of course, leads one to ask: why have SF family home sales surged by so much this summer?

Obviously, record low mortgage rates have been a catalyst, but it appears as if there has also been a sizeable, pandemic-related shift in the demand for existing householders who have not been materially impacted financially from the pandemic (1) away from urban areas and into suburban (or even more remote) areas, and (2) away from renting in multifamily units and into single-family detached units There has also apparently been a huge increase in demand for second homes, especially but not solely in beach, mountain, and country “resort” areas.

This “discrete” shift in relative demand, combined with limited supply as fewer than normal households already in single-family homes have been moving and listing their property for sale, has already started to put major upward pressure on prices of single-family detached homes, and in some areas of the country have created almost “bubble-like” conditions.

And this discrete shift in demand has played a massively larger role in the surge in SF home sales than “demographics.”