A bubble requires both overvaluation based on fundamentals and speculation. It is natural to focus on an asset’s fundamental value, but the real key for detecting a bubble is speculation … Speculation tends to chase appreciating assets, and then speculation begets more speculation, until finally, for some reason that will become obvious to all in hindsight, the “bubble” bursts.

Maybe prices are too high based on fundamentals (due to extremely low supply and record low mortgage rates), but there is very little evidence of speculation (not like the loose lending of the housing bubble).

Ben Carlson discusses lending (and other issues) in Why This is Not Another Housing Bubble.

The lack of wild speculation doesn’t mean house prices can’t decline, but it means that we won’t see cascading declines in prices like what happened when the housing bubble burst. In the 2006 through 2011 period, as prices fell, and teaser rates and other “affordability products” expired – more and more homeowners were forced to sell (or just walk away). That drove prices down 26% nationally from peak to trough, and much more in certain “bubble” cities like Las Vegas (down 62% from peak) and Phoenix (down 56%).

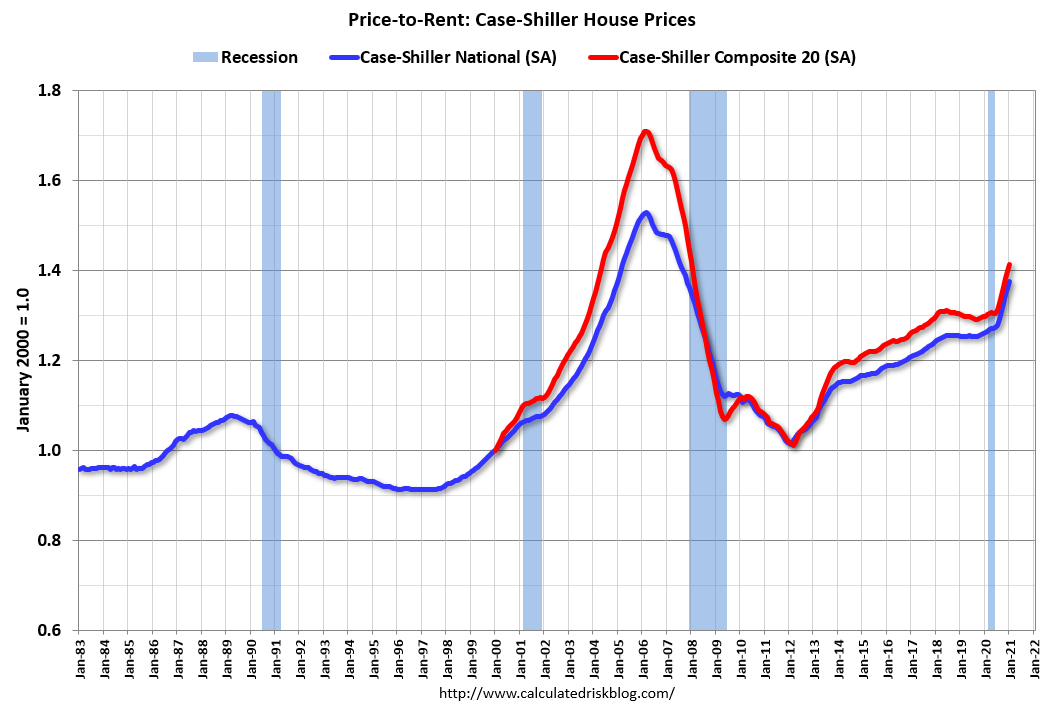

Here is a similar graph using the Case-Shiller National and Composite 20 House Price Indexes.

Here is a similar graph using the Case-Shiller National and Composite 20 House Price Indexes.

This graph shows the price to rent ratio (January 2000 = 1.0). This suggested prices were way too high during the housing bubble, and also suggests prices might be high now – but only about half the housing bubble.

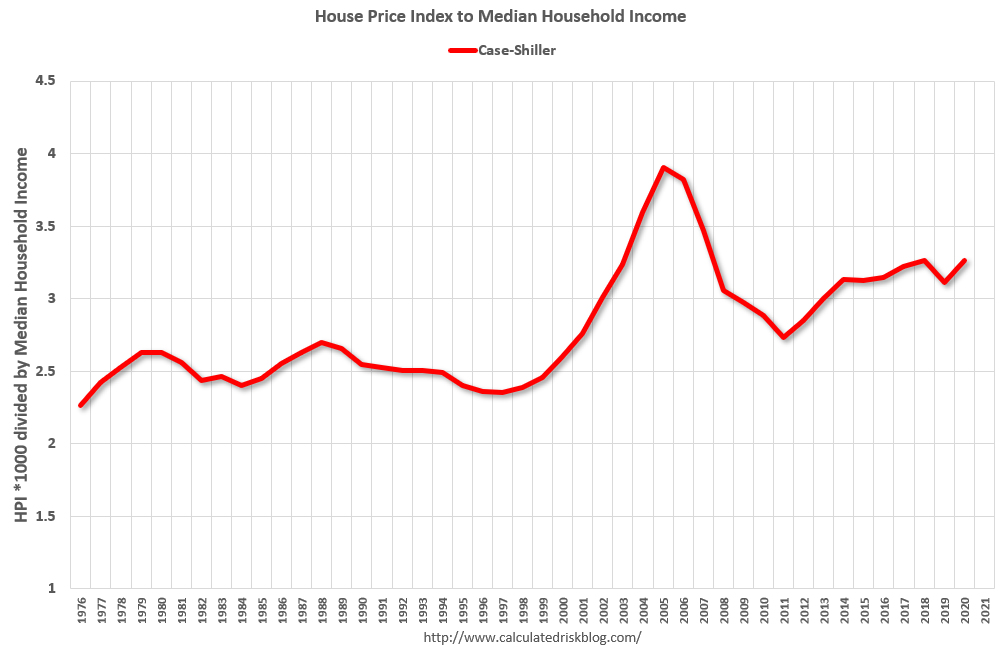

Here is another measure – house prices to the Median Household income.

This graph uses the year end Case-Shiller house price index – and the nominal median household income through 2019 (from the Census Bureau). 2020 median income is estimated at a 5% gain.

This graph uses the year end Case-Shiller house price index – and the nominal median household income through 2019 (from the Census Bureau). 2020 median income is estimated at a 5% gain.

This graph shows the ratio of house price indexes divided by the Median Household Income through 2020 (the HPI is first multiplied by 1000).

This uses the year end National Case-Shiller index since 1976 (December 2020 estimated).