U.S. hotel performance data for the week ending 4 July showed a slight decline in occupancy from the previous week, according to STR.

28 June through 4 July 2020 (percentage change from comparable week in 2019):

• Occupancy: 45.6% (-30.2%)

• Average daily rate (ADR): US$101.36 (-20.9%)

• Revenue per available room (RevPAR): US$46.21 (-44.8%)Occupancy had risen in week-to-week comparisons for 11 straight weeks since mid-April.

“Demand came in 67,000 rooms lower than the previous week, and beyond that, July 1 was a reopening day for a lot of hotels, further impacting the occupancy equation,” said Jan Freitag, STR’s senior VP of lodging insights. “A rise in COVID-19 cases has led to states pausing or even rolling back some of their reopenings. Beaches have been a big demand driver for hotels, but with many beaches closed ahead of the July 4 holiday, all but two markets in Florida showed lower occupancy than the previous week. Growing concern around this latest spike in the pandemic has further implications for leisure and business demand alike.” emphasis added

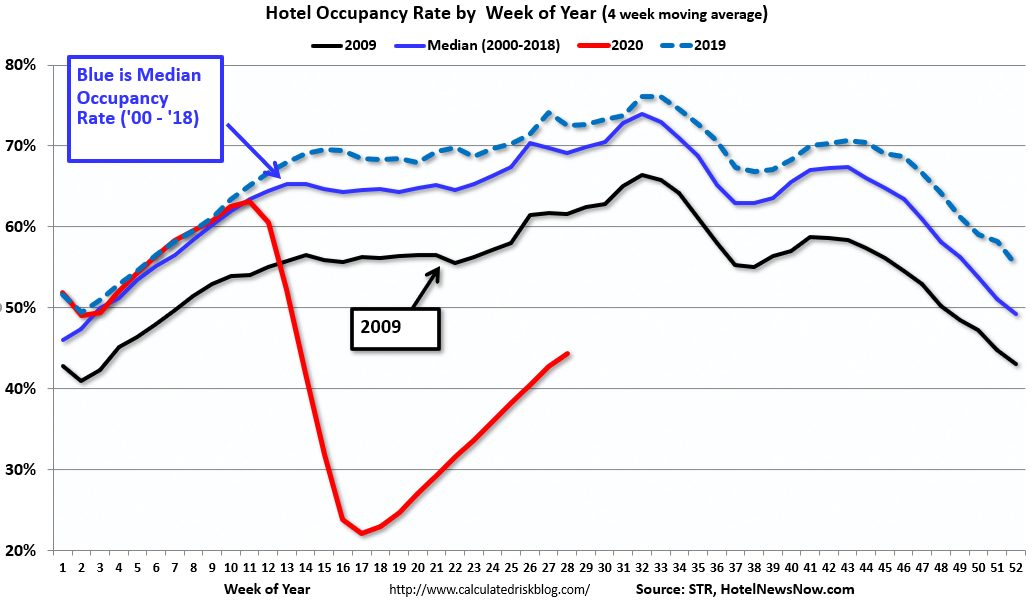

The following graph shows the seasonal pattern for the hotel occupancy rate using the four week average.

Click on graph for larger image.

Click on graph for larger image.

The red line is for 2020, dash light blue is 2019, blue is the median, and black is for 2009 (the worst year probably since the Great Depression for hotels).

Usually hotel occupancy starts to pick up seasonally in early June. So some of the recent pickup might be seasonal (summer travel). Note that summer occupancy usually peaks at the end of July or in early August.

According to STR, the improvement appears related mostly to leisure travel as opposed to business travel.

Note: Y-axis doesn’t start at zero to better show the seasonal change.