Hirschmann Partnership letter to investors for the year ended December 31, 2020.

Q3 2020 hedge fund letters, conferences and more

Dear Partner,

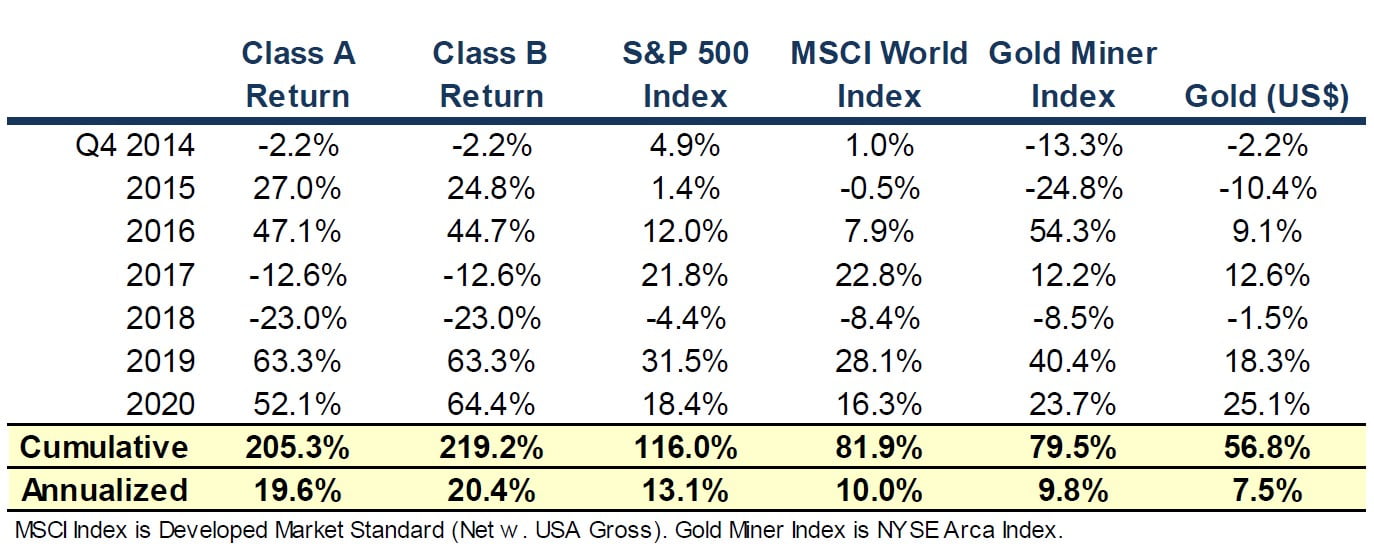

In H2 2020, Class A appreciated 21.0% v. 23.4% for the S&P 500. Updated results, net of all fees, for the Hirschmann Partnership (the “Fund”) are shown below:

As a reminder, the share classes are identical except for their performance allocation. For Class A, the performance allocation is 25% of the profit above a 6% hurdle rate. For Class B, it is 33% of the profit above the S&P 500 return. Neither has a management fee.

Although the Fund has appreciated ~160% over the past two years, our gold mining equities (GMEs)1 remain incredibly undervalued. Our GMEs are trading at $200 per gold reserve ounce versus the $1600 per reserve ounce that Warren Buffett’s Berkshire Hathaway recently paid for Barrick Gold.2 That valuation differential should narrow dramatically and thus the Fund should trounce its benchmarks over the long-term even if gold prices falter.

More likely, gold prices won’t falter. Instead they should surge as the late-innings bubbles in bonds, China, US equities and US real estate burst. If so, the Fund should appreciate more than 500%. While temporary underperformance is possible, our eventual gains will almost certainly be worth the wait.

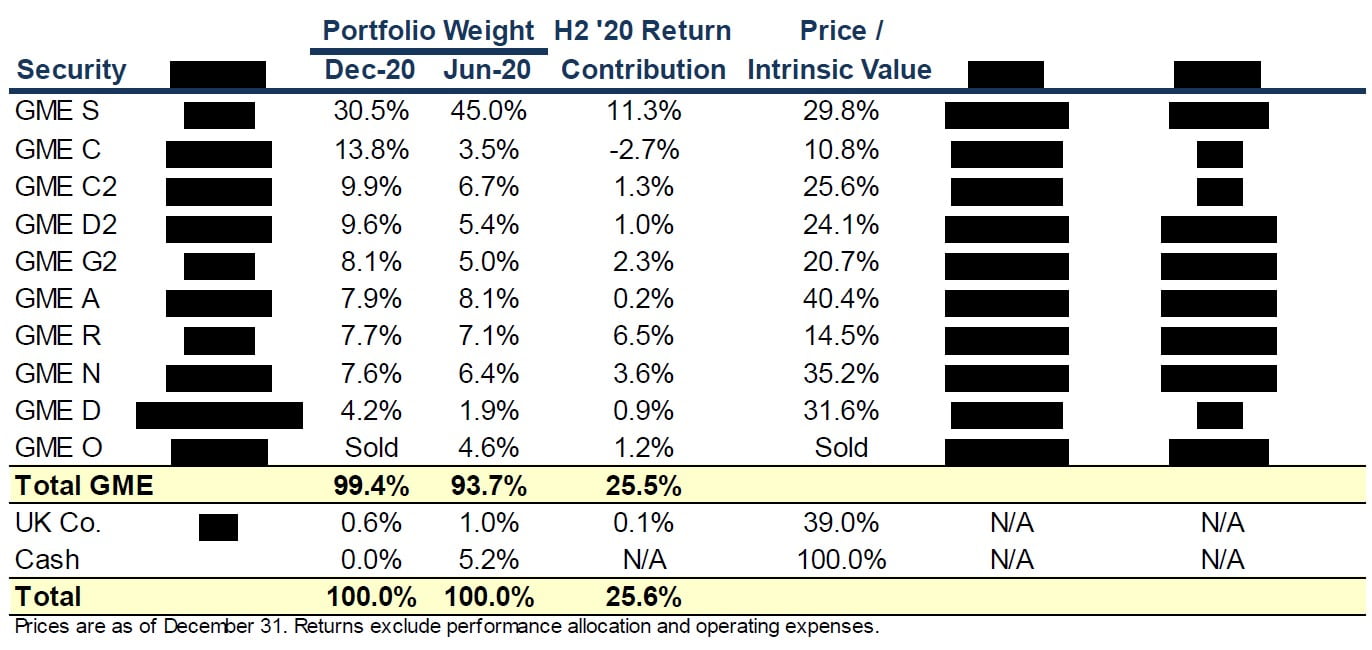

Hirschmann Partnership Portfolio Detail

Our portfolio is summarized below:

GME S (“S”) appreciated as it [REDACTED]. S remains a large position due to its high expected return and low long-term risk.

GME R and GME N appreciated, probably due to their low valuations and [REDACTED]. GME N also [REDACTED].

GME C (“C”) [REDACTED]. The Fund should ultimately earn a high return on its C investment as C converges with its intrinsic value.

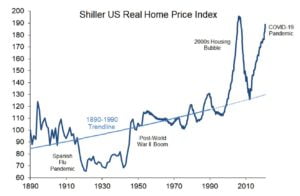

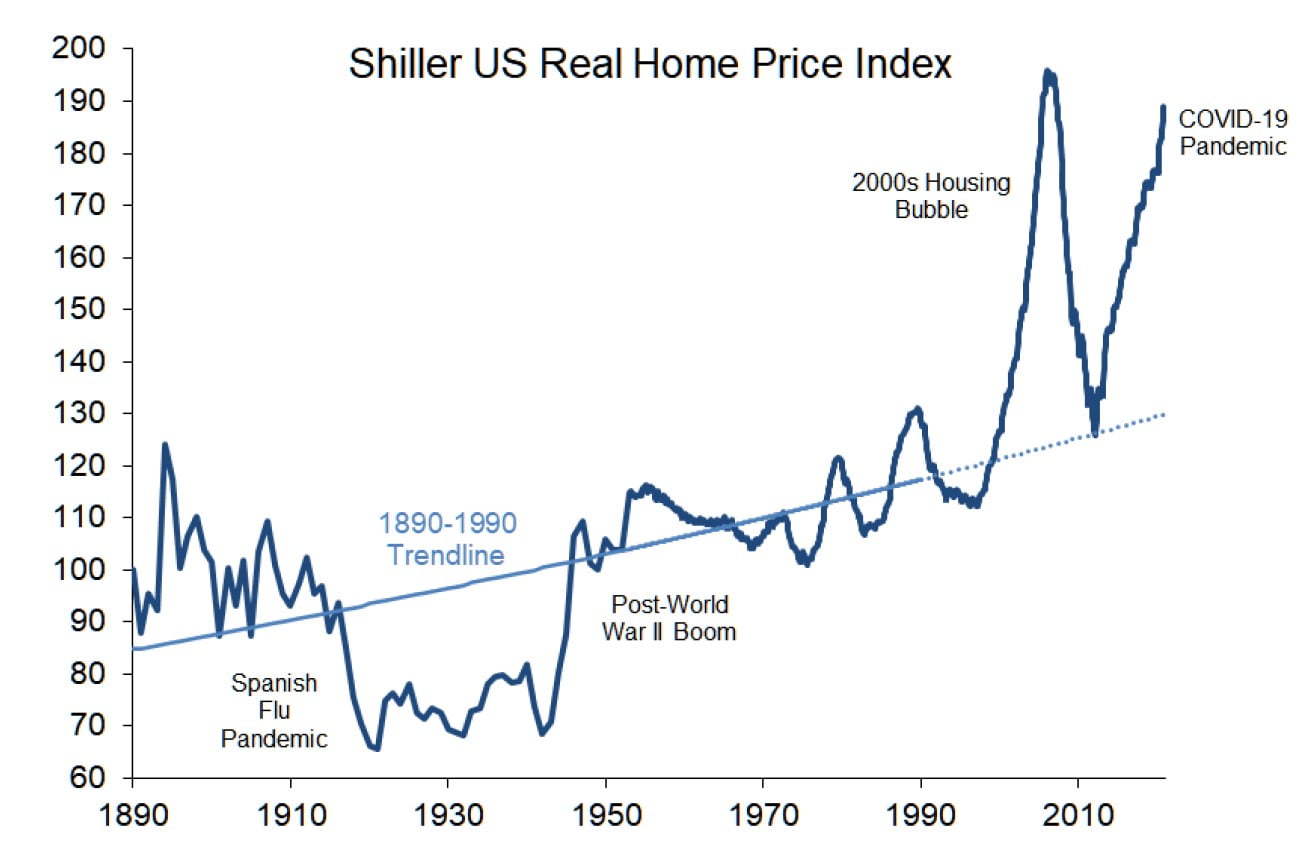

US Real Estate Bubble

As shown below, US residential real estate (RRE) prices are ~50% above their long-term trend and are approaching their 2006 peak. Price-rent and price-income ratios are also far above their historical averages and nearing their 2006 peaks.3

US commercial real estate (CRE), which is roughly half the size of the RRE market, is also severely overvalued. In fact, in early 2020, CRE prices were at an all-time high relative to income.4 While CRE prices have since declined modestly (~8%), CRE cash flow has plunged far more (~30% y/y).5

High RRE and CRE valuations are not justified by low interest rates. As during the 2000s housing bubble, builders are incentivized to churn out new real estate whenever prices are high. Hence new construction will pressure both RRE and CRE prices even if rates remain low. (Single-family housing starts have been steadily increasing for the last decade and even increased in 2020.)6

If new supply doesn’t burst the real estate bubble, higher interest rates should. As discussed in the mid-year 2020 letter, a US government (USG) debt crisis seems inevitable and should cause interest rates to spike. That should cause equity and real estate prices to plunge, which in turn should exacerbate the debt crisis. Our GMEs should then skyrocket.

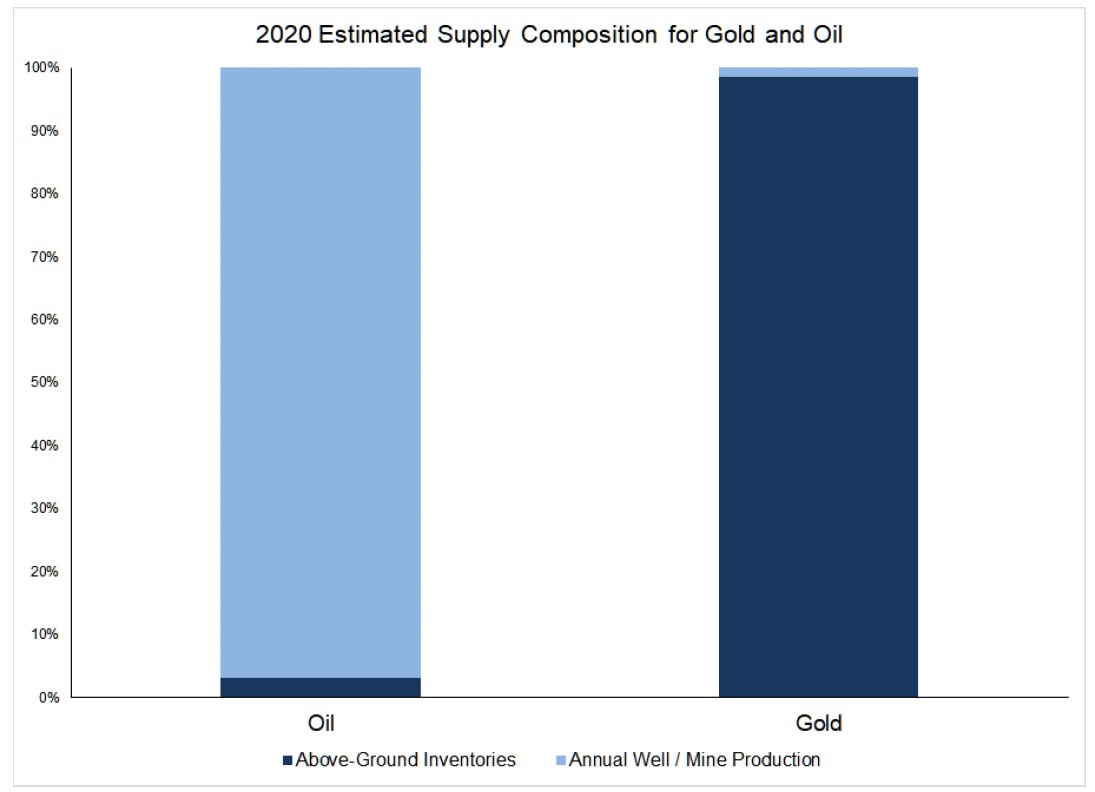

Gold Supply

A gold bear recently argued that gold mine production will reduce gold prices just as shale oil production has reduced oil prices. However, gold mine production, unlike oil well production, is a tiny portion of supply.

Oil is representative of industrial commodities in that nearly all annual production is quickly consumed. As shown in the chart below, the amount of oil that is stored (e.g. in tanks or oil tankers) is small relative to annual production.8 Therefore, oil production influences prices far more than inventories do.

In contrast, nearly all mined gold has been stored for investment as bullion or jewelry.9 10 As a result, global gold inventory has grown steadily over past millennia and is now more than 60 times annual mine production. Thus, annual mine production is a tiny percentage of gold supply and has a correspondingly tiny impact on prices. While mine production is almost guaranteed to increase if gold’s price rips higher, production should remain small relative to gold supply.

Because gold supply doesn’t change much from year to year, investor demand is the primary gold price driver. Although my method for forecasting long-term investor demand is confidential, the takeaway is that gold does not seem overvalued and should go through the roof if any of the aforementioned bubbles burst.

Other

We remain open to new investors, so feel free to distribute the redacted version of this letter.

I am the Fund’s second-largest investor and continue to have most of my net worth invested in the Fund.

I was recently interviewed by Palisades Radio regarding gold, the Fed and the looming government debt crisis.

I also occasionally post articles relevant to the Fund on Twitter and less frequently on LinkedIn. To view Tweets without creating a Twitter account, see this article.

Hirschmann Partnership continues to strive for tax efficiency and has yet to incur any significant short-term capital gains. 2020 tax estimates were distributed in October and December. I expect those estimates to be distributed more promptly in 2021.

Partners will receive several items over the next six months:

- Account statements should be sent this week. [REDACTED]

- 2020 K-1s should be sent by March

- The Fund’s audited financial statements should be sent by May

- The Fund’s next letter should be sent in mid-July

The Fund’s most important competitive advantage will always be its patient clients, so I greatly appreciate your continued support. Please contact me with any questions or comments.

Kind regards,

Brian Hirschmann

Managing Partner

Endnotes

1 GMEs were referred to as gold-linked securities (GLS) in prior letters. I’ve changed the nomenclature solely for clarity. The underlying investments have not changed

2 The GME gold reserve ounce multiple estimate excludes GME N because [REDACTED].

3 Source: Aaron Brown, Bloomberg, Harvard University Joint Center for Housing Studies

4 Source: Altus Group, Cornerstone Real Estate Advisers, David Ling, NAREIT

5 Source: Green Street Advisors, NAREIT

6 Source: Dodge Data & Analytics

8 Source: US Energy Information Administration

9 Source: World Gold Council

10 Jewelry is often called “the poor man’s insurance” due to its investment value

The post Hirschmann Partnership Up 52 Percent In ’20; Warns Of US RE Bubble appeared first on ValueWalk.