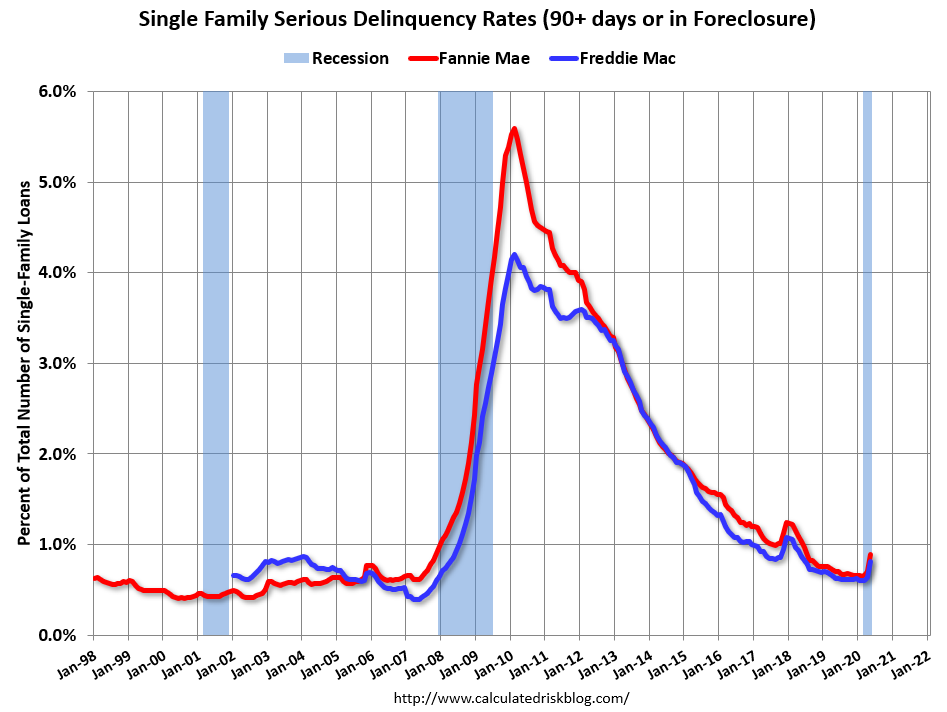

This is the highest serious delinquency rate since June 2018.

These are mortgage loans that are “three monthly payments or more past due or in foreclosure”.

The Fannie Mae serious delinquency rate peaked in February 2010 at 5.59%.

Click on graph for larger image

Click on graph for larger image

By vintage, for loans made in 2004 or earlier (2% of portfolio), 3.09% are seriously delinquent (up from 2.64% in April). For loans made in 2005 through 2008 (3% of portfolio), 5.22% are seriously delinquent (up from 4.41%), For recent loans, originated in 2009 through 2018 (95% of portfolio), only 0.53% are seriously delinquent (up from 0.38%). So Fannie is still working through a few poor performing loans from the bubble years.

With COVID-19, this rate will increase significantly in June and July (it takes time since these are mortgages three months or more past due).

I believe mortgages in forbearance will be counted as delinquent in this monthly report, but they will not be reported to the credit bureaus.

This is very different from the increase in delinquencies following the housing bubble. Lending standards have been fairly solid over the last decade, and most of these homeowners have equity in their homes – and they will be able to restructure their loans once they are employed.

Note: Freddie Mac reported earlier.