Euclidean Technologies commentary for the second quarter ended June 2020, titled, “Quantifying Margin of Safety.”

Q2 2020 hedge fund letters, conferences and more

Although having recovered a good deal since the March lows, value strategies like Euclidean’s continue to suffer disproportionately during the pandemic. I am reluctant to assign a cause to why one part of the market is performing better than another, but the pain experienced by small-cap value funds during COVID-19 is likely due to the fact that investors see large companies as more impervious to the economic fallout of the pandemic (warranted or not). With that said, history clearly reveals that our style of investing would have outperformed over long periods of time. And nonetheless, there would have been similar periods of underperformance.

To give perspective on the current situation, I’d like to share a thought experiment I recently read that was posted as a tweet by Matt Tracey (@MattTracey13). To paraphrase it, imagine that you are standing in 2007 after value strategies in general have had a very strong run lasting many years. For example, the S&P 500 over the period January 2000 to December 2007 had an annualized return of just 1.7% whereas Euclidean’s simulated performance over the same period was over 20% annualized. Knowing that the performance of all styles of investing wax and wane over time, you may think that value approaches will be less likely to continue to outperform in the years to come. That is, in the years 2008 and beyond. If you are about to newly deploy capital, you may yearn for a more attractive entry point. But if asked to describe that entry point, how might you respond? You might want to see a combination of:

- A long period of value underperforming.

- Historically wide valuation spreads (as they were in 1999 at the outset of the last best entry point).

- Especially sharp recent underperformance of value strategies.

- A rising frequency of “is value dead?” headlines.

- A lot of justification for massive premiums on growth companies.

- No real evidence that the extent of the underperformance can be explained by company fundamentals.

Again, being in 2007, if an oracle could tell you that every one of these conditions would exist in a little over a decade, presumably you would be yearning to deploy your capital into a value strategy in 2020. Nonetheless, value strategies are some of the least popular approaches to investing right now. Recency bias is the well-documented cognitive bias that attributes greater importance to the most recent events even when they are statistically less significant than the long-term trends. The above thought experiment illuminates the power that recency bias holds over us. By projecting ourselves into a different time and imagining how we’d feel then, we realize how much more we are influenced by our experiences in the recent past than by an objective outside view. I think this is a valuable perspective to have when thinking about how small-cap value investing will perform over the next decade.

A New Approach To Systematic Value Investing

As many of you are aware, Euclidean has for some time been conducting research into a new approach to systematic value investing. This approach uses machine learning to forecast future operating earnings rather than using current earnings to evaluate companies as potential investments. In addition, this approach quantifies the uncertainty in these forecasts to avoid investments with more uncertain earnings outlooks. We recently authored an academic paper on this research that was accepted for publication and presented at the International Conference on Machine Learning (ICML). Furthermore, we have transitioned fully to using this new approach to systematic value investing in Euclidean Fund I. All new investments since March have been made using this new deep learning based model. We have discussed this research in several prior letters but I believe it is worth reviewing now that it is driving our live investment process. So, how does this new model work?

Forecasting Uncertainty At Euclidean

In prior research, we used deep learning to forecast companies’ future earnings, then we used those forecasted earnings in a traditional factor model. Specifically, we trained a deep neural network to forecast companies’ future earnings before interest and taxes (EBIT) for the following year. We then calculated the ratios of companies’ forecasted EBIT to their enterprise values (EV) and sorted the universe of companies by this ratio (EBIT/EV). Companies with the highest ratios would be thought of as the best “value stocks,” and we showed that simulated portfolios based on forecasted EBIT performed better than models based on a company’s trailing 12-month EBIT.

Although these results were encouraging, we knew that making point forecasts of a company’s future earnings left out important information that could facilitate better investment decisions. Our models had no way to express how much confidence we should have in each individual company’s forecast. After all, two companies with very similar earnings point forecasts may represent different kinds of opportunities, with very different risks. We might expect future earnings to be more predictable for an established utility than for a new company or for a company operating in a highly cyclical industry. Moreover, we might expect the range of likely future earnings to be different for the same company at different times, perhaps becoming more difficult to predict following a large acquisition, the expiration of a patent, or as the economy moves from a period of stable growth into a time of change.

Just as weather forecasters use data to construct an uncertainty cone around the projected path of a hurricane, we set out to develop a process to estimate the distribution of a company’s future earnings. This probability distribution has both a mean and a variance. Therefore, when attempting to quantify the uncertainty in a forecast, we no longer forecast a specific value for future earnings. Instead, we train deep neural networks to learn the mean and variance of possible future values. With the mean and variances in hand, we can construct “earnings cones” (or credible intervals) in which actual earnings will fall within a set percentage (e.g., 75%) of the time.

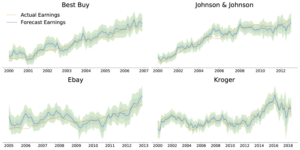

Sample outputs generated from our deep neural networks for individual companies are shown below. The orange lines show the actual trailing 12-month EBIT for each company at each point in time. The blue lines show what our model’s mean forecasts were, one year ahead of the company’s actual results at each point in time. The shaded areas around the blue lines show the model’s calibrated (1) credible intervals (hereafter, credible intervals) around each mean forecast. The darker shaded area is one standard deviation from the mean, and the lighter shaded area is two standard deviations. The total shaded interval around the mean contains approximately 80% of the company’s actual earnings.

How Uncertainty Estimation Improves A Value Factor Model: A Quantitative Approach To Margin Of Safety

Warren Buffett has famously described the principle of margin of safety as follows:

“When you build a bridge, you insist it can carry 30,000 pounds, but you only drive a 10,000 pound truck across it. And the same principle works in investing.”

In investing, this translates to the fact that there is inherent uncertainty in estimating the value of a business. Therefore, if the estimate of a business’ intrinsic value is only a little more than the price it is selling for, then there is very small margin of safely. However, if the estimate is, for example, 50% more than the price it is selling for, then there is a large margin of safety.

Our use of deep neural networks to quantify uncertainty in earnings estimates is employed to directly apply the principle of margin of safety in a quantitative and systematic way. To do this, we take our previous earnings-forecast work one step further by discounting a company’s forecast future EBIT by the forecast variance in the EBIT. By using this more conservative approach, companies with less-certain earnings forecasts (and wider credible intervals) will be ranked lower – and will be less likely to be included in simulated portfolios – than they would in either Traditional Factor Models or our previous simulations using the mean forecast.

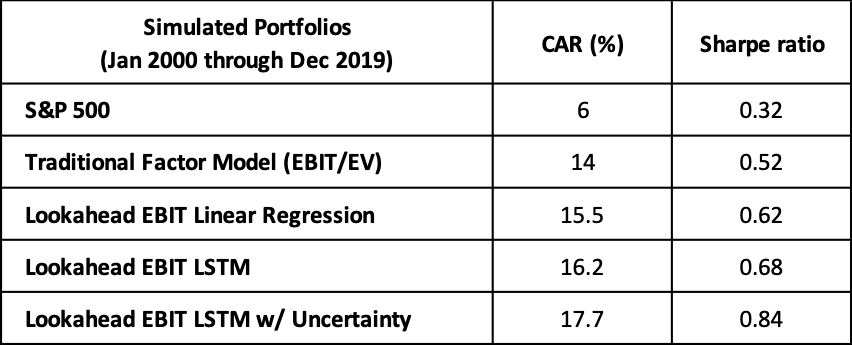

Here are some high-level simulated results, reflecting 50-position portfolios using four different methods for ranking value stocks.

In these simulations (2), the three methods of using forecast, or “lookahead,” EBIT all perform better than the traditional factor model, which uses companies’ trailing 12-month earnings. In addition, using the uncertainty-based earnings forecast cones results in somewhat higher returns and Sharpe ratios than what we previously saw when making point forecasts. The technical details of this model and the experimental results can be found in our ICML paper.

***

We have evolved our investment process over time to incorporate new learning. Even as we stand today, confident in our process and optimistic that the environment will eventually be supportive of our deep-value approach, Euclidean remains devoted to learning. We continue to seek the best methods for uncovering history’s lessons and overseeing a systematic process that reflects what we have found.

Best,

John

The opinions expressed herein are those of Euclidean Technologies Management, LLC (“Euclidean”) and are subject to change without notice. This material is not financial advice or an offer to purchase or sell any product. Euclidean reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

Euclidean Technologies Management, LLC, is an independent investment adviser registered under the Investment Advisers Act of 1940, as amended. Registration does not imply a certain level of skill or training. More information about Euclidean, including our investment strategies, fees, and objectives can be found in our ADV Part 2, which is available upon request.

[1] One of the challenges with uncertainty quantification is uncalibrated prediction intervals. For example, a 90% credible interval may not contain the true value 90% of the time. Therefore, we use the techniques detailed in this paper to calibrate credible intervals.

[2] In these simulations, NYSE, AMEX, and NASDAQ companies were ranked according to the stated criteria. Non-US-based companies, companies in the finance sector, and companies with a market capitalization that, when adjusted by the S&P500 Index Price to January 2010, is less than $100M were excluded from the ranking. The simulation results reflect assets-under-management (AUM) at the start of each month that, when adjusted by the S&P500 Index Price to January 2010, is equal to $100M. Portfolios were constructed by investing equal amounts of capital in the top 50 of companies represented by each value factor and then rebalancing monthly to equally weight the evolving constituents of the top decile. The amount of shares of a security bought or sold in a month was limited to no more than 10% of the monthly volume for a security. The purchase and sale price of a security was based on volume weighted daily closing price of the security during the first ten trading days of each month. Transaction costs are factored as $0.02 per share plus an additional slippage factor that increases as a square of the simulation’s volume participation in a security. Specifically, if participating at the maximum 10% of monthly volume, the simulation buys at 1% more than the average market price or, conversely, sells at 1% less than the average market price. Other than these transaction costs, the simulated results do not reflect the deduction of any management fees or expenses. Historical simulated results presented herein are for illustrative purposes only and are not based on actual performance results. Historical simulated results are not indicative of future performance.

This article first appeared on ValueWalk Premium.

The post Euclidean 2Q20 Letter: Quantifying Margin of Safety appeared first on ValueWalk.