ESG (Environmental/Social/Governance) Investing Filters – We Must Clean the Lens to Maintain Forward Momentum

Q2 2020 hedge fund letters, conferences and more

Credits: Cover photo; Forbes. ESG investing link circa 2016 self-authored post PRI (Principles of Responsible Investing), 2016 Singapore Conference and Raconteur; Responsible Investing 2020 Archives; The Sunday Times.

Introduction

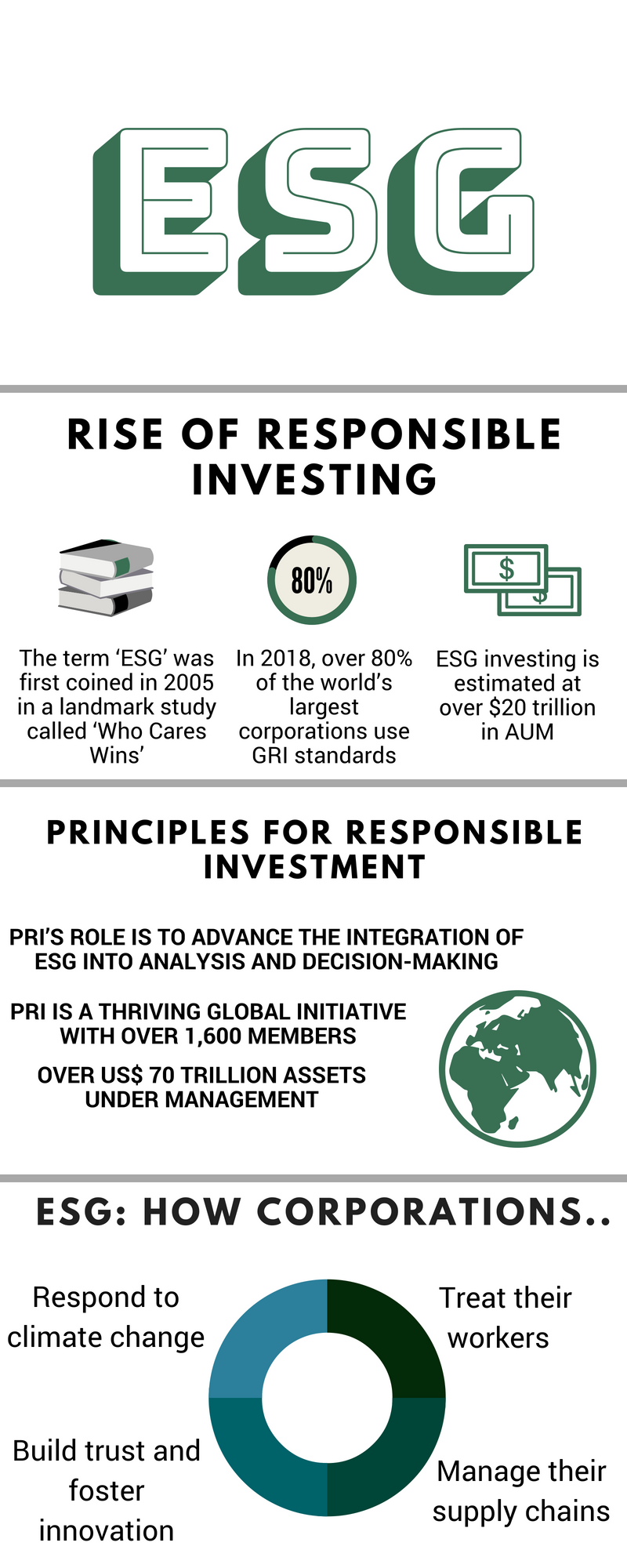

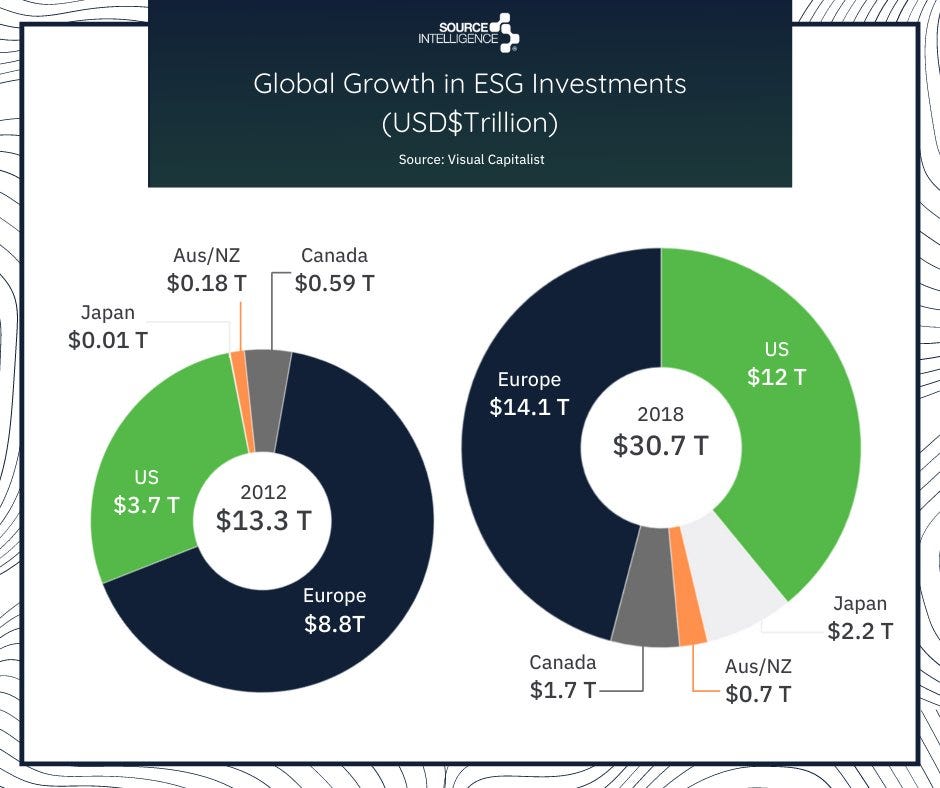

We need to collectively improve all facets of the ESG investment mega-trend in support of multi-cycle, long-term value creation. With 1 of every 4 dollars currently invested at stake ($2–3/4 or 1/2 to 2/3rds’, within 5 years, at the current ESG trajectory), there is palpable urgency. Globally, it is estimated US$45 trillion in assets under management adhere to a sustainable investment approach, which are inclusive of ESG principles. The Global Sustainable Investment Alliance (2019) estimated this figure at US$30 trillion as recently as 2018 (breakdown by geography below). The Principles for Responsible Investing (PRI), the largest global network of institutional asset managers employing ESG principles now has > 2,500 signatories representing US$85 trillion in AUM, roughly equivalent to current US GDP. A full 85% of S&P index companies report on ESG issues presently, up from 11% in 2011.

Like with every gold rush, the initial swell in interest from all players in the global investment ecosystem often leads to short-cuts being taken and work- arounds, in the absence of true expertise/data. This article reviews some of the key ESG issues of the day including; ESG scoring, data challenges, and a brief review of the ESG credentialing issues becoming evident. The end investor, whether it be a pension fund, sovereign wealth fund, insurance company or ETF fund manager should be in the driver’s seat as the ESG autobahn traffic swells. Investors have the fiduciary duty to ensure that the data, assessment tools and professionals involved in optimizing their choices are not just up for the task, but that they can add alpha over non-ESG screening peers. Investor’s relative and absolute investment performance is clearly exposed to ESG factors, regardless of the degree they employ active strategies over passive, in-house management versus 3rd party manager, or private versus public markets.

Blackrock and Scottish Widows pension fund have collaborated to launch The Climate Transition World Equity Fund, a new portfolio dedicated to helping the transition to a low carbon economy. Scottish Widows will contribute £2 billion initially as they look to offer their customers more sustainable investment choices. Due diligence is required in vetting any ESG labeled funds as they are self-identified as such. A deep dive into material weightings should be undertaken to ensure “bad actors” are kept to a minimum, if not explicitly excluded.

Word Games

“ESG”, “responsible investing”and “sustainable investing” are the three most common used umbrella terms in the space and can largely be thought of as equivalent. ESG investors like Blackrock typically assess ESG factors based on non-financial data on environmental impact (e.g. carbon footprint, carbon intensity, waste management, and energy efficiency), social impact (e.g. human rights, labor standards, diversity) and governance attributes (e.g. financial accounting reporting practices, board composition, and executive compensation). No definitive, comprehensive list of ESG issues has been agreed.

In a sign of the growing importance of such non-financial disclosures, Blackrock’s Investment Stewardship Team voted their shareholding in Volvo AB in June 2020 to oust the chief of the Swedish manufacturing giant for poor climate risk disclosures and a lack of progress on climate related matters. Blackrock’s votes were not enough to carry, but clearly a shot across the bow to companies (over 50 have seen a similar message conveyed by the world’s largest money manager) not taking ESG, in particular their climate stewardship, seriously enough.

Title elevation has been a partial result; Chief Sustainability Officer, Global Head of Sustainability, Head of Green and Sustainable Finance and Head of Sustainability Integration to name a few. Thousands more carry the title ESG Analyst of course but this is to be expected as the scope and diligence of task in enormous. This is especially true are more firms move to report on a broader scope of exposures.

Acronyms and a lexicon of terms seemingly crafted by Dr. Seuss do not help the cause on message clarity or a broad construct adoption metric. The terms are both related and nested like Russian dolls, but the resultant confusion only serves to stunt the advancement of real, measurable change on the continuum of sustainability, responsible investing and the evolution of socially responsible investing; #ESG, #EthicalInvesting #GreenInvesting, #ImpactInvesting, #ResponsibleInvesting, #SRI, #SociallyResponsibleInvesting, #RI, #ResponsibleInvesting, #SI, #SustainableInvesting, #CSR, #CorporateSocialResponsibility, #ValuesBasedInvesting, #GreenFinance, #GreenBonds, #CleanEnergy, #NetZero, #CarbonFree, #CarbonBubble, #ClimateBonds, #PositiveScreening, #NegativeScreening, #CarbonFootprint, #ProxyVoting, #RenewableEnergy, #SustainableandResponsibleInvesting, #Stewardship, #ThematicInvesting, #TransitionRisk, #PhysicalRisk, #Values-basedInvesting, #SDGs, #SustainableDevelopmentGoals, #SustainabilityBonds, #SocialBonds, #EnterpriseRiskManagement, #ERM, #EnterpriseRiskManagement, #PRI, #PrinciplesofResponsibleInvesting, #CarbonSink, #GRI, #GloballyResponsibleInvestment.

#Greenwashing is a term you will hear often, whereby especially with respect to the “E” in ESG; false or exaggerated claims are made regarding just how well a given firms investments are aligned with sustainability goals (Climate Action is #13 of the United Nations 17 Sustainable Development Goals). The Task Force on Climate Related Disclosures (TCFD) offers some guidance in this regard; they recommend firms disclose Scope 1 (direct emissions), Scope 2 (indirect emissions from the generation of purchased electricity, steam, heating and cooling consumed by the reporting company) and, where appropriate Scope 3 (all other indirect emissions that occur in a company’s value chain) emissions. The term also applied to some of the less effective Corporate Social Responsibility (CSR) programs which fall under the “S” category.

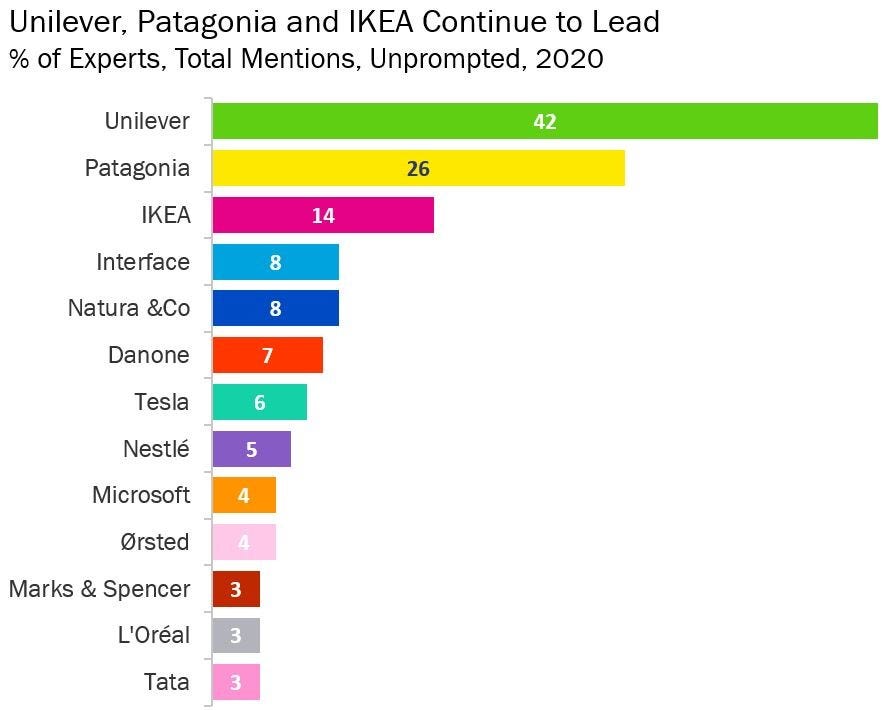

GlobeScan/SustainAbility 2020 Sustainability Leaders Survey

Citibank has announced plans to measure and disclose carbon emissions from their loans and investments, joining Bank of America and Morgan Stanley in collecting and disclosing exposures in the Scope 3 category.

The concerns to date have been with the double counting of carbon offsets which potentially has the effect of under reporting in overall emissions. There are plans to tackle this double counting issue, Article 6 of the Conference of the Parties on Climate Change (COP) 26, to be held in Dublin, Ireland in November 2021.

Credentials

1.) Sustainability and Climate Risk (SCR™) Certificate; Global Association of Risk Professionals (GARP). New certificate for 2020, Cost US$650, inclusive of study materials. 100–130 hours of preparation expected. 3 hour exam, 80 multiple choice questions. GARP annual dues US$150, membership covering Financial Risk Manager (FRM®) and ERP® Energy Risk Professional (ERP®) charterholders. GARP membership is not required, but the SCR fee is $100 lower for members.

2.) Chartered Financial Analyst (CFA®), UK – Certificate in ESG Investing. 130 hours of expected preparation time. Started in 2019, exam has 100 questions, 2 hours and 20 minutes. £470 fee covering exam and certification. CFA Institute annual dues are US$275 for Chartered Financial Analyst ® charterholders and candidates. Local CFA Chapter dues are an additional $175, making total annual fees $450 for most. Membership is not required to retain your ESG certificate upon passing, it should be noted.

3.) Chartered Socially Responsible Investment Counselor (CSRIC™). Offered jointly by the College for Financial Planningand US SIF: The Forum for Sustainable Investment. Study time 90–135 hours (est.).US$1,300 fee, annual fee US$95.

4.) Fundamentals of Sustainable Accounting (FSA™) Credential. Offered by the Sustainability Accounting Standards Board (SASB). Two levels of exams, 1,400 signed up for level 1, > 450 have achieved the FSA credential. 25 hours of preparation per exam level. $450 fee for level 1 exam. It is uncertain why the FSA had to be broken into 2 levels/exams, given the 100 hour + estimated preparation time for other ESG/Sustainability offerings.

5.) Frankfurt School of Finance & Management:

i.) Certified Expert in Climate & Renewable Energy Finance (CECRF™)

ii.) Certified Expert in Climate Adaptation Finance (CECAF™)

iii.) Certified Expert in Sustainable Finance (CESF™)

6.) Certified ESG Analyst (CESGA®). The European Federation of Financial Analyst Societies (EFFAS). €1,500. Pricey indeed.

Credential summary

The push for credentials is partially due to legislation/regulation in Europe. MiFID II, is a cornerstone of the EU’s regulation of financial markets, with an aim to improve protection for investors. MiFID II legislation obliges advisors to question clients of their ESG preferences as part of their due diligence/fact find.

None of the listed ESG programs are intensive enough to imply Subject Matter Expert (SME) status upon completion, despite the implication of some of the certificate titles. All bring a higher level of awareness to practitioners in an expanding space.

Access to data is the biggest challenge ESG investors face when called upon to make comparative investment choices. Like in so many facets of our modern life, data is the oxygen of ESG analytics. The most robust data set is available for public (listed) equities, with all other categories under-researched. There is a bias towards larger companies as the small ones lack the staffing bench and data budget of bigger firms. Emerging markets data is spotty versus developed markets, for similar reasons. Firms like MSCI, Sustainalytics and S&P Global are scrambling to solidify leadership in the provision of the data and tools the throngs of customer sets require to be top quartile ESG ready (other providers include; Morningstar, FactSet, Bloomberg, and Robeco).

Reporting

There is little standardization in reporting. Most corporation self-report using self-selected ESG metrics. Data inputs are rarely audited, making validation and comparisons difficult (across both time period and companies). 3rd party ESG scoring is done largely by firms using their own data and methodologies, leading to a wide deviation in resultant ratings.

The “Big 3” Blackrock, Vanguard and State Street have been vocal in this area. Blackrock’s Chairman Larry Fink has asked companies to use SASB (Sustainability Accounting Standards Board) metrics for their ESG and sustainability reporting (77 standards in total, with guidance for firms that operate in multiple industries). Thus far in 2020 the SASB notes 279 companies are reporting to their standard, up from 118 for all of 2019. SASB has 150 investors using its metrics in their investment process. On the face of it, this would appear to be a step in the right direction. Conflicts abound with so many oligopolistic industries abound. (Bloomberg LP founder and majority owner Michael Bloomberg is chairman emeritus of the SASB.)

The ongoing valuation of intangible assets should be improved as ESG and sustainability metrics clearly have a bearing on both the trend and absolute value (e.g. brand value). More than 80% of the value of the S&P is now attributable to intangible assets versus traditional plant and equipment and other hard assets.

ENVIRONMENTAL:

The contribution a reporting entity makes to climate change through greenhouse gas emission curtailment, along with waste management and energy efficiency. With ongoing efforts to reduce global warming, given its harmful effects on the planet, decarbonizing has become the mantra.

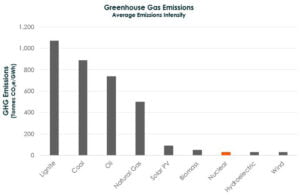

Energy Mix Challenges

ESG investors consider renewable energy not just a sound idea, but a moral imperative. Many of the “E” targets and much of the data is on greenhouse gas (GHG) emissions; the reporting, reduction, control and mitigation of same.

A full 40% of China’s electricity production is from coal fired plants. Japan relies upon coal for over 33% of their power generation, with renewables barely moving the needle. Pre-Fukushima (2011) Japan was 40% nuclear powered but capacity has only slowly been brought back on stream as a skeptical populace grimace. Germany turned anti-nuclear post Fukushima (8 of 17 reactors have been shut down since, with all remaining to be shuttered by 2022) and now gets 40% of their power from lignite (brown coal) which has a 20–35% carbon content! S. Korea have seen their nuclear energy share fall from 30% in 2016 to 23% in 2018 coincident with coal moving to 42% from 39% (renewable power generation was 4.9% in 2018 for reference). Globally, nuclear power makes up 10% of the world’s energy mix. France has the highest percentage nuclear globally at 72%. France is slated to fall below 50% nuclear by 2035 as 14 reactors go offline over the intervening period. There are currently 447 global active nuclear reactors (99 reactors or 40% in the USA, providing 20% of the USA energy needs). New reactors planned in China, India, UAE and Russia will see tremendous growth in the absolute amount of nuclear power produced globally over the coming decades, despite the noted plant furloughs. UAE’s first of 4 enormous 1400MW nuclear reactors (Unit #1) at Barakah Nuclear Power Plant just went into operation in 2020, providing carbon free energy to the nation’s electrical grid for the first time in history (the 1st operating nuclear plant in the Arab world). Mega reactors are the trend, but Advanced Small Modular Reactors (SMRs) are gaining traction, with several underway in Argentina, China and Russia. Canada is also studying the potential role of SMRs.

The US and China still get > 90% of their energy from fossil fuels. The number for Canada is 68%, due in large part to hydroelectric power (60% of Canada’s electricity is produced from hydroelectric power).Canada’s renewable energy “stack” is dominated by hydroelectric power at 68%, followed by biomass at 23%, wind power 5%, 1.7% ethanol, 1% recycled muni waste/landfill and finally solar 0.6%. Countries like Canada are modestly sized in term of their overall GHG emissions, but large in terms of the hydrocarbon resources, many of which must remain untapped in order to reach global CO2 reduction goals. In Canada, the federal government implemented a nation-wide carbon price, beginning at C$20/tonne of carbon dioxide equivalent emissions (tCO2e) in 2019, rising the C$50/t over time. Canada gets 17% of its overall energy from nuclear power from 19 reactors, primarily based in the Province of Ontario.

As California is finding out recently with rolling black out, solar and wind power makes poor substitutes for base load demand. Record temperatures, wildfires and scant wind has not been helping their cause.

New York recently shuttered one of their nuclear reactors at Indian Point, with the last one remaining to be closed in 2021. The amount of power produced by the closed reactor is greater than all the wind and solar energy produced in the entire state of New York. To replace the power lost on the closing of 1 reactor with wind turbine derived power would require 1,300x the land footprint of the Indian Point reactor (which lies 24 miles north of New York City).

Nuclear energy has declined 7% since the mid 1990’s and despite sizeable investment/subsidy wind + solar (Environmental Progress reported wind and solar investment at $2.1 trillion over the 2008–2016 period versus $1.8 trillion in nuclear power over the 1962–2016 period) has not been able to make up the power generation difference.

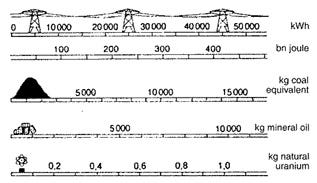

Fuel comparison infographic, note: 10,000 kg oil = 74 barrels oil

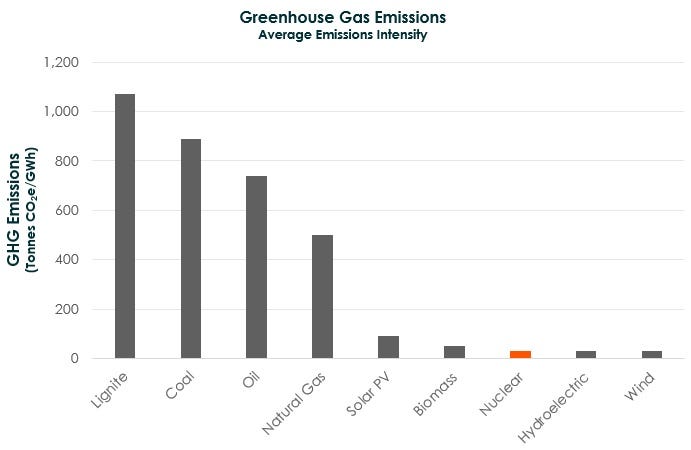

Hard choices need to be made. Nuclear power does not involve the burning of fossil fuels. Few agree on compatibility with ESG principles or nuclear power’s role in the energy transition. Without an increase in nuclear power or a combination of nuclear and geothermal power (where the technology is a work in progress, on a scaled basis) greenhouse gas emission reduction targets are not likely to be met.

Initial estimates are that GHG emissions year over year are -5.5% due to COVID-19. This compares to -1.4% experienced in the depth of the global financial crisis in 2008, as per the Global Carbon Project. The UN Environmental Program estimates that curtailment of -7.6% per year in GHG is required to meet the < 1.5° C Paris Agreement (COP 21 12/2015) target. Clearly, wishing for worse than the C-19 pandemic, on an annual basis, is not the way to get there. Proponents of green energy will likely need to be converted to proponents of fission over time.

Geoengineering

There are several man-made approaches to inducing negative emissions that can potentially be used as carbon offsets. Geoengineering is the large-scale manipulation of the environment with the intent to mitigate global warming from anthropogenic GHGs. Man-made good hoping to offset man-made ills, if you will.

Approaches are land-based, ocean-based, atmosphere-based and space-based. The land based approaches to carbon dioxide removal (CDR) have the most potential, afforestation (growing forests where they did not exist) and reforestation (replanting where harvested prior) in particular. Wildfires are a major threat in this category of carbon sink creation as the carbon previously captured in the wood fibre literally goes up in smoke upon combustion with all the carbon released into the atmosphere (with carbon offsets negated, obviously). Carbon Capture & Storage (CCS), another land-based solution, is still high cost with deep underground storage the most viable option at scale. I can see CCS adoption in countries like Canada given the lower population density, but one should never underestimate the power of NIMBY/NUMBY (“not under my back yard”) lobbying efforts, in any jurisdiction.

Atmosphere and space based solutions focus on increasing planetary albedo (the proportion of the incident light or radiation that is reflected by a surface). Solar Radiation Management (SRM) is the broad geoengineering category. I’m challenged to see evidence of the governmental cooperation required to successfully launch such a program as there is no way to limit the effects of stratospheric aerosol application to a limited geography.

Ocean-based approaches involve iron fertilization meant to spawn a plankton bloom that absorbs carbon, eventually forming ocean sediment as the plankton dies off. Experiments gone awry by researchers (Russ George, circa 2012) might cap ocean-based approach advancement for a time on concerns of toxic tides, lifeless waters and increased ocean acidification.

These geoengineering approaches, on the whole, can only be called upon to offset a small amount of accumulated man-made emissions. The “don’t burn fossil fuels in the first place” approach is hence the default driver of aggregate lower emissions going forward.

SOCIAL:

Diversity & Inclusion

The COVID-19 pandemic has highlighted the “S” in ESG as social issues are front of mind for billions of the world’s population; unemployment, growing inequality and growing poverty levels.

Blackrock is at the forefront yet again, Larry Fink has made the commitment to hire 30% more Blacks by 2024. Blacks currently make up 5% of Blackrock’s total payroll, and 3% of their senior officers (Director and above). This would take the percentage to 6.5% which is progress indeed. 15% of the population of the US is Black (working population closer to 6.5%).

Perhaps due to the COVID-19 social unrest seen in 2020, the May 2020 George Floyd’s murder, the #BLM movement, the fact that women were given the right to vote 100 years ago yet women make up only 6% of S&P 500 CEO positions has received little attention (women make up 47% of the US workforce).

GOVERNANCE:

The “G” will not be ignored in the ESG mix either as a number of issues are coming to a head, spurred on by the COVID-19 pandemic. Governance, including internal oversight, culture and aligning stakeholder interest have been the focus of investors, governments, and companies for many decades, since well before ESG was hatched as a concept.

i.) Financial accounting and reporting practices. EBITDA has had a “C” added to it for many companies, stripping out the COVID-19 blip to direct investors attention to the future “normalized” earnings path. Non-GAAP (Generally Accepted Accounting Principles) earnings, like ESG ratings, can not be compared as there is no standardized methods for computing them. As noted, the migration to SASB reporting standards for ESG could improve comparability going forward.

ii.) Role of Board Leadership and Composition. Less old boy’s club, more racial diversity, more women, less board cloning in smaller markets (e.g. Canada).

iii) Anti-bribery and corruption. The low side estimates at 0.7% of global GDP “slippage” $0.6 bln with high side estimates $3.5bln. With the median COVID-19 government support well > 20% of GDP this high-side estimate will likely prove to be on the low side.

iv.) Business ethics. This will be a critical metric as supply chains are re-engineered post COVID-19. There are many environmental facets to be considered in the pivot to autarky (self-sufficiency) from globalization.

v.) Compensation. As a snapshot statistic, CEO to median employee comp: USA 278x, Japan 58x, UK 201x and Germany 136x. Poorly funded pension plans is perhaps a better deficiency to attack near term as we have front-loaded a lot of equity out-performance and locked in paltry fixed income returns (80% of the global bond universe trades < 2% in absolute terms with the spreads on high yield at all time lows, corporate bond issuance $6.4 trillion year to date in 2020, set to eclipsing 2017 record) with the globally co-ordinated COVID-19 response.

Conclusion

Globally, ESG related regulations and disclosure requirements total 1,052 (80% of them mandatory) in 63 discrete countries. The message is clear, ESG is coming for you, meet it head on.

Caleb Gibbons , CFA, FRM

@firehorsecaper

The post ESG Investment Filters – We Must Clean the Lens to Maintain Forward Momentum appeared first on ValueWalk.