Texas factory activity expanded in August for the third month in a row following a record contraction in the spring after the onset of the COVID-19 pandemic, according to business executives responding to the Texas Manufacturing Outlook Survey. The production index, a key measure of state manufacturing conditions, came in at 13.1, down slightly from July but still indicative of moderate growth.

Other measures of manufacturing activity also point to expansion this month. The new orders index advanced three points to 9.8, and the growth rate of orders index surged more than 10 points to 11.8. The shipments index rose from 17.3 to 23.3, while the capacity utilization index inched down but remained positive at 10.9.

Perceptions of broader business conditions improved in August. The general business activity index turned positive after five months in negative territory, coming in at 8.0. The company outlook index registered a third consecutive positive reading, shooting up 11 points to 16.6, its highest reading in nearly two years. The index measuring uncertainty regarding companies’ outlooks remained positive but retreated to 8.2.

Labor market measures indicated solid growth in employment and workweek length. The employment index pushed up from 3.1 to 10.6, suggesting more robust hiring. Twenty-three percent of firms noted net hiring, while 13 percent noted net layoffs. The hours worked index pushed up five points to 10.5.

emphasis added

This was the last of the regional Fed surveys for August.

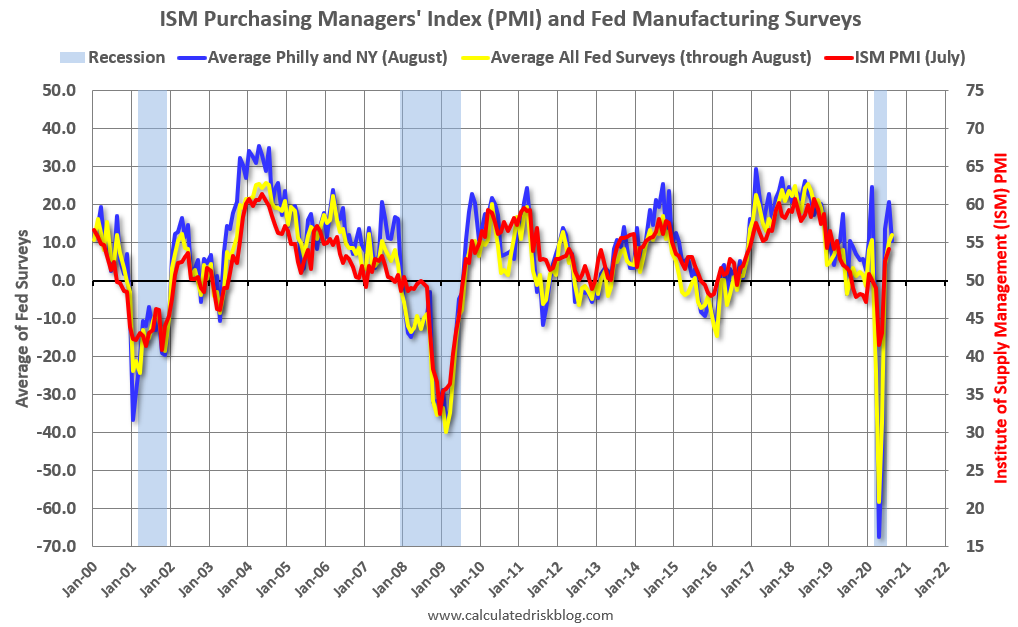

Here is a graph comparing the regional Fed surveys and the ISM manufacturing index:

Click on graph for larger image.

Click on graph for larger image.

The New York and Philly Fed surveys are averaged together (yellow, through August), and five Fed surveys are averaged (blue, through August) including New York, Philly, Richmond, Dallas and Kansas City. The Institute for Supply Management (ISM) PMI (red) is through July (right axis).

The ISM manufacturing index for August will be released on Tuesday, September 1st. The consensus is for the ISM to be at 54.5, up from 54.2 in July. Based on these regional surveys, the ISM manufacturing index will likely be at about the same level in August as in July.

Note that these are diffusion indexes, so returning to 0 (or 50 for ISM) means activity is not declining further (it does not mean that activity is back to pre-crisis levels).