CoreLogic® … today released the Homeowner Equity Report for the first quarter of 2021. The report shows U.S. homeowners with mortgages (which account for roughly 62% of all properties) have seen their equity increase by 19.6% year over year, representing a collective equity gain of over $1.9 trillion, and an average gain of $33,400 per borrower, since the first quarter of 2020.

While the coronavirus pandemic created economic uncertainty for many, the continued acceleration in home prices over the last year has meant existing homeowners saw a notable boost in home equity. The accumulation of equity has become critically important to homeowners deciding on their post-forbearance options. In contrast to the financial crisis, when many borrowers were underwater, borrowers today who are behind on mortgage payments can tap into their equity and sell their home rather than lose it through foreclosure. These conditions are reflected in a recent CoreLogic survey, with 74% of current homeowners with mortgages noting they are not concerned with owing more on their home than it is worth within the next five years.

“Homeowner equity has more than doubled over the past decade and become a crucial buffer for many weathering the challenges of the pandemic,” said Frank Martell, president and CEO of CoreLogic. “These gains have become an important financial tool and boosted consumer confidence in the U.S. housing market, especially for older homeowners and baby boomers who’ve experienced years of price appreciation.”

“Double-digit home price growth in the past year has bolstered home equity to a record amount. The national CoreLogic Home Price Index recorded an 11.4% rise in the year through March 2021, leading to a $216,000 increase in the average amount of equity held by homeowners with a mortgage,” said Dr. Frank Nothaft, chief economist for CoreLogic. “This reduces the likelihood for a large numbers of distressed sales of homeowners to emerge from forbearance later in the year.”

Negative equity, also referred to as underwater or upside down, applies to borrowers who owe more on their mortgages than their homes are currently worth. As of the first quarter of 2021, negative equity share, and the quarter-over-quarter and year-over-year changes, were as follows:

• Quarterly change: From the fourth quarter of 2020 to the first quarter of 2021, the total number of mortgaged homes in negative equity decreased by 7% to 1.4 million homes, or 2.6% of all mortgaged properties.

• Annual change: In the fourth quarter of 2020, 1.8 million homes, or 3.4% of all mortgaged properties, were in negative equity. This number decreased by 24%, or 450,000 properties, in the first quarter of 2021.

• The national aggregate value of negative equity was approximately $273 billion at the end of the first quarter of 2021. This is down quarter over quarter by approximately $8.1 billion, or 2.9%, from $281.1 billion in the fourth quarter of 2020, and down year over year by approximately $13.3 billion, or 4.6%, from $286.3 billion in the first quarter of 2020.

emphasis added

Click on graph for larger image.

Click on graph for larger image.

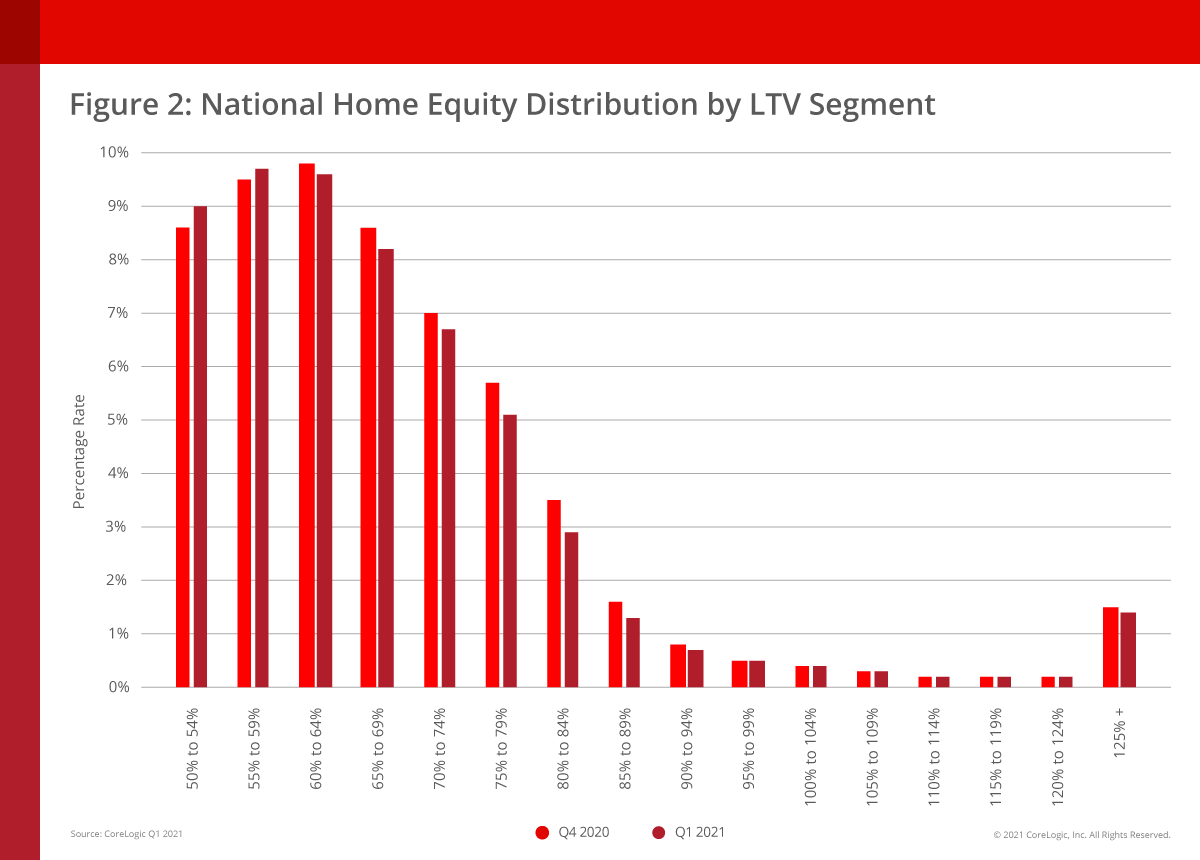

This graph from CoreLogic compares Q1 to Q4 2020 equity distribution by LTV. There are still quite a few properties with LTV over 125%. But most homeowners have a significant amount of equity. This is a very different picture than at the start of the housing bust when many homeowners had little equity.

On a year-over-year basis, the number of homeowners with negative equity has declined from 1.8 million to 1.4 million.