Based on builder reports, and recent housing activity, I expect a significant increase in single family starts over the next couple of months.

Earlier: Housing Starts increased to 974 Thousand Annual Rate in May

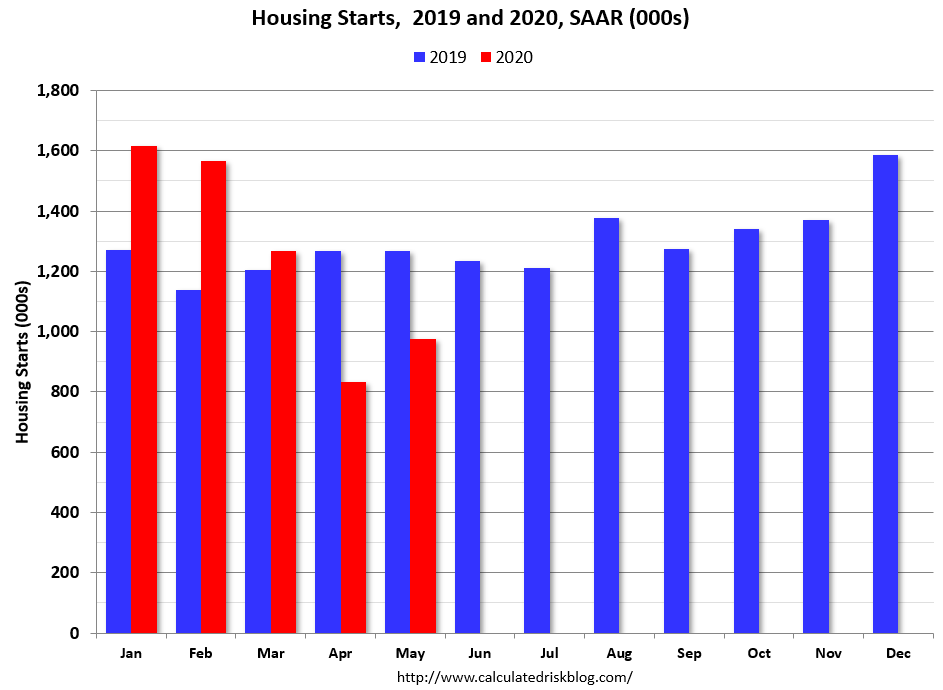

Total housing starts in May were well below expectations, and revisions to prior months were negative (combined).

The housing starts report showed starts were up 4.3% in May compared to April, and starts were down 23.2% year-over-year compared to May 2019.

Single family starts were down 17.8% year-over-year, and multi-family starts were down 33.1% YoY.

This first graph shows the month to month comparison for total starts between 2019 (blue) and 2020 (red).

Click on graph for larger image.

Click on graph for larger image.

Starts were down 23.2% in May compared to May 2019.

Last year, in 2019, starts picked up in the 2nd half of the year, so the comparisons are easy early in the year.

Starts, year-to-date, are only down 2.4% compared to the same period in 2019.

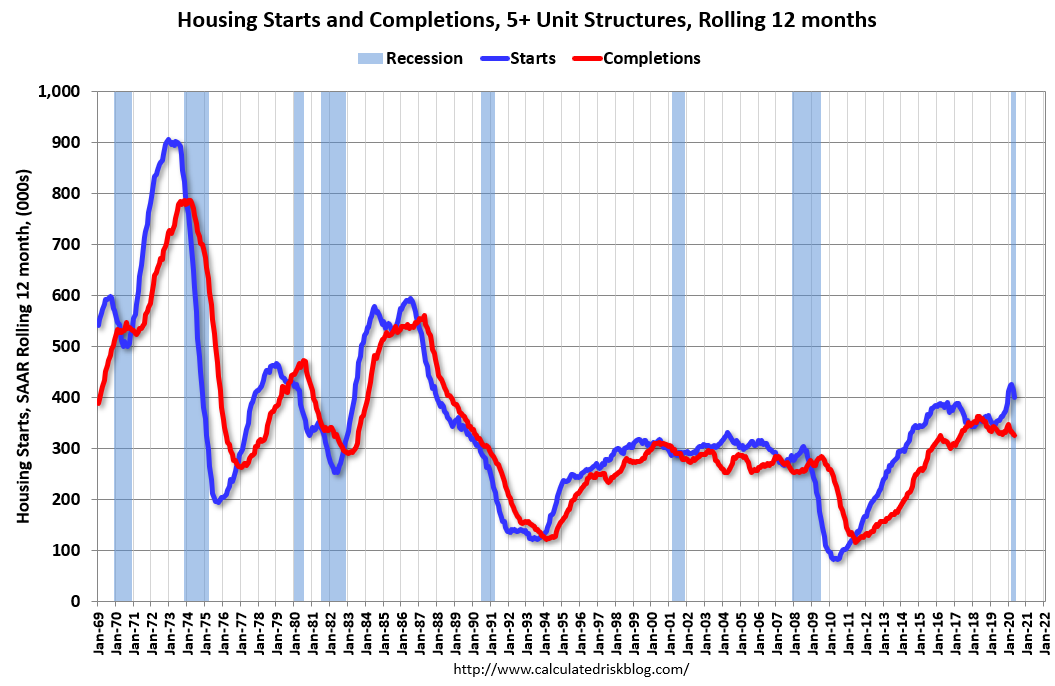

Below is an update to the graph comparing multi-family starts and completions. Since it usually takes over a year on average to complete a multi-family project, there is a lag between multi-family starts and completions. Completions are important because that is new supply added to the market, and starts are important because that is future new supply (units under construction is also important for employment).

These graphs use a 12 month rolling total for NSA starts and completions.

The blue line is for multifamily starts and the red line is for multifamily completions.

The blue line is for multifamily starts and the red line is for multifamily completions.

The rolling 12 month total for starts (blue line) increased steadily for several years following the great recession – then mostly moved sideways. Completions (red line) had lagged behind – then completions caught up with starts- although starts picked up a little again lately.

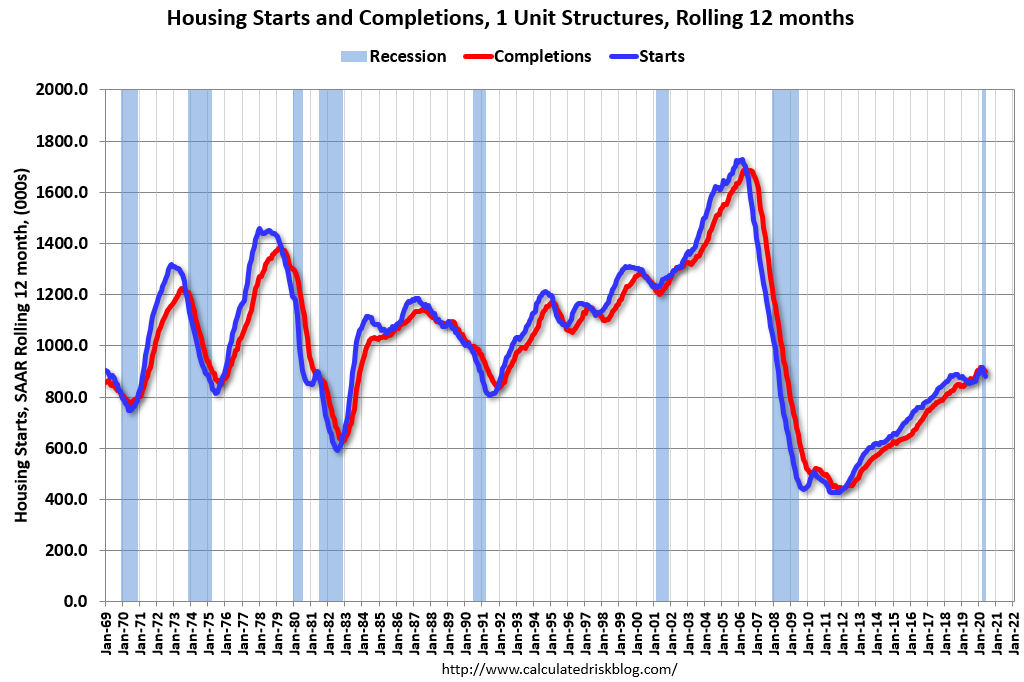

The second graph shows single family starts and completions. It usually only takes about 6 months between starting a single family home and completion – so the lines are much closer. The blue line is for single family starts and the red line is for single family completions.

The second graph shows single family starts and completions. It usually only takes about 6 months between starting a single family home and completion – so the lines are much closer. The blue line is for single family starts and the red line is for single family completions.

Note the relatively low level of single family starts and completions. The “wide bottom” was what I was forecasting following the recession, and now I expect some further increases in single family starts and completions once the crisis abates.