BNPL services are convenient and easily accessible — but consumers need to be wary of getting in over their heads.

Q2 2020 hedge fund letters, conferences and more

Though credit cards are a popular way to pay for items over time, they’re an expensive route to take. The moment you begin to carry a balance, you start accruing interest that’s apt to cost you over time. That’s one big reason buy now, pay later (BNPL) services are gaining popularity. While the BNPL model offers key benefits, there are drawbacks, too.

How BNPL services work

With a BNPL service, you buy something online or in a store, then pay it off in interest-free installments. Generally, there are no tacked-on fees, provided you stick to the payment plan.

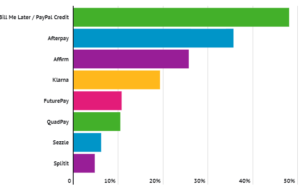

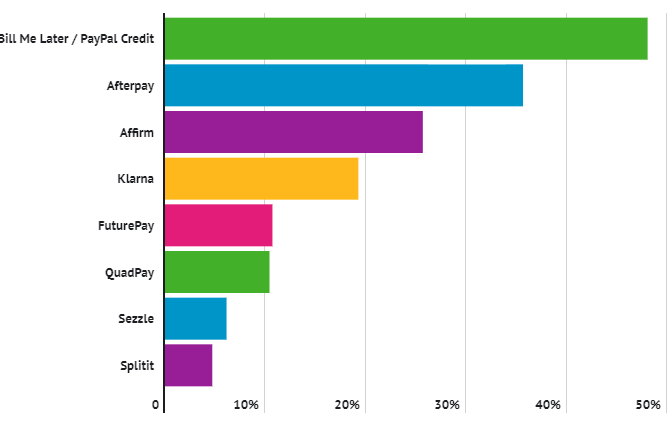

The Ascent, a personal finance brand by The Motley Fool, wanted to learn more about how consumers use BNPL services, so they conducted a survey of 1,862 consumers. Based on those results, these are the most commonly utilized buy now, pay later providers:

Of those surveyed, 37.65% had used a BNPL service. Most fell between the ages of 18 and 54. But that usage is still sporadic, with 27.67% of people using a buy now, pay later service once a year or less, and 21.11% using one every six months. Only 3.85% of those who use a BNPL service do so more than once a week.

The main reasons consumers use BNPL services

The draw of BNPL services is clear: Consumers get to pay off purchases over time without incurring interest. In fact, 39.37% of those who use a buy now, pay later service cite avoiding credit card interest as the reason for going this route. Meanwhile, 38.37% like BNPL services because they allow them to make purchases that otherwise wouldn’t fit into their budgets, and 24.68% like these services because they don’t require credit checks.

The danger of BNPL services actually lies in these so-called conveniences.

The problem with BNPL services

The BNPL model is a great alternative to credit cards in situations where you want a little cash-flow flexibility and know you’ll be able to stick to the repayment terms. But there are downsides to BNPL.

If you fail to stick to your payment schedule, fees and interest apply, and in some cases, the interest on a buy now, pay later purchase will well exceed what your credit card would charge. Also, BNPL services can lead to impulse spending, and they make it easy to go over budget on items you don’t actually need.

Furthermore, while some consumers may regard the absence of a credit check as a BNPL perk, it actually isn’t. Being denied a credit card or line of credit is a sign that you’re not in a strong enough financial position to take on more debt, and the fact that buy now, pay laterservices gloss that over means those who use these services risk wrecking their finances.

The BNPL model also isn’t abundantly clear to consumers. Among those surveyed, only 22.13% say they have a strong understanding of how buy now, pay later services work. And 48.50% of consumers who have never used a buy now, pay later service say they’ve specifically avoided them because of a lack of understanding.

Are BNPL services a good idea for you?

When used correctly, BNPL services are a convenient tool for consumers who need a touch of leeway in paying for purchases. They’re also good for emergency purchases — essential items you need right away, but can’t necessarily pay for in full and don’t want to charge on a credit card.

But be careful when using buy now, pay later for splurges, especially if money is tight or if you’re in credit card debt. Also, pay close attention to the terms of your BNPL agreement before completing a purchase. Each provider sets its own payment schedule (and fees for not keeping up), so be sure you know exactly what you’re getting into.

The post Buy Now, Pay Later Gains Popularity Despite Risks appeared first on ValueWalk.