Bronte Capital’s Amalthea Fund commentary for the second quarter ended June 2020, discussing their previously largest shorted stock, Wirecard and the losses that stem from it.

Q2 2020 hedge fund letters, conferences and more

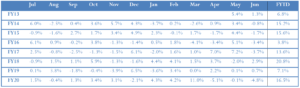

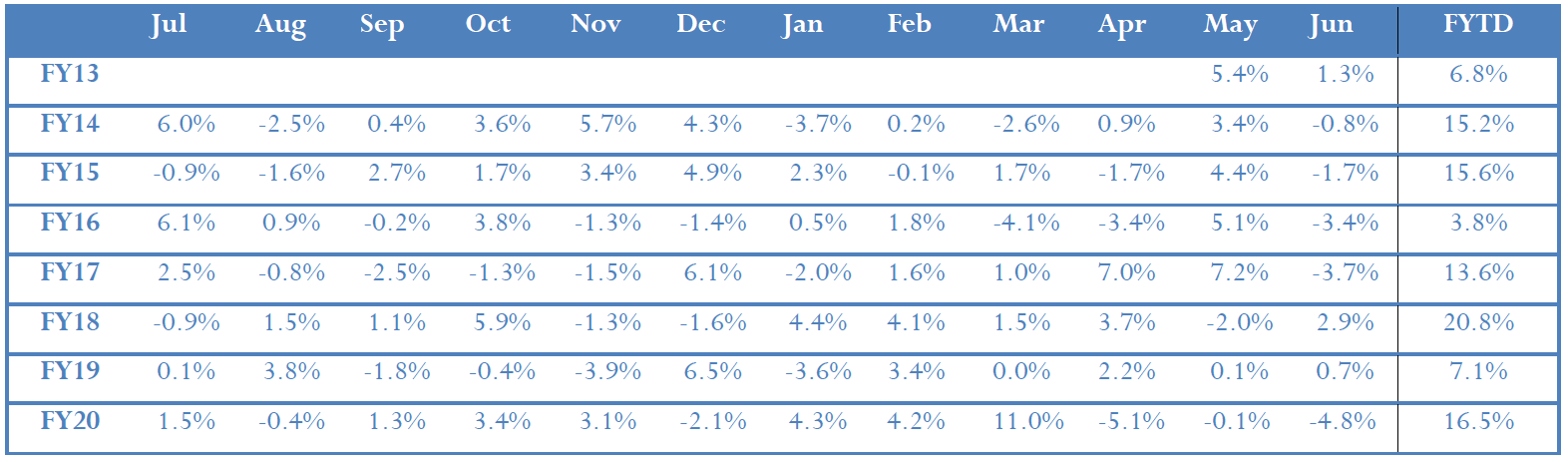

The fund was down by 4.84% in June whereas the globally diversified MSCI ACWI index (in $A) fell by 0.53%. Over the course of the last financial year Amalthea grew by 16.46%, outpacing the 3.91% gain in the ACWI. We write extensively this month on our performance and positioning over the last quarter.

End of Financial Year: The fund’s accountant, Ernst & Young, will be calculating the annual distribution the fund will make (see over).

The distribution is based on realised gains that are generally taxable whereas the gains that are reported to you each month include unrealised gains. The fund is up for the year and has realised significant gains so, at this stage, we anticipate making a distribution.

In the event that there is a distribution you will receive (we anticipate in early August):

- An annual tax statement;

- A distribution statement; and

- If you have elected to re-invest, a contract note detailing the number of additional units issued in the fund

If a cash distribution is determined and you have elected not to re-invest in the fund, then the payment will be made to your previously nominated bank account within approximately 2 business days of these documents being issued.

Once the distribution is determined the fund will also issue a second June 2020 holding statement. But unlike the one sent with this letter this second one will be “ex-dividend” i.e. it will show your holdings at 30 June 2020 after allowing for the distribution from the fund.

Quarterly Review

Our last quarter was arguably the worst quarter in the history of our firm. It was – to be fair – a bad quarter after several good quarters. But it’s worth a thorough explanation of what went wrong, where we are and why we think we are managing your money sensibly.

In our last quarterly letter, we were deeply bearish about the world (we remain so). We decided to position the portfolio as such. To quote:

Looking forward, we are not taking outsized bets where we do not have an edge and where we think the range of outcomes skews towards the downside. If we could buy hedges cheaply we would be willing to take (much) larger positions. But the sort of protection we bought for very low prices in February is only available at nose-bleed prices now.

Alas there is a corollary. Our potential for very high profits at the moment is also low.

We then added a sentence that haunts us:

If the market roars back, we are going to feel like we have missed out.

Alas the market did roar back, and we feel like we (meaning you) have missed out. The last quarter was our worst relative quarter in the history of the firm. Nothing about the quarter was threatening, as we live to play another day. But nothing was pleasant either.

Australian dollar-denominated clients might not see it that way. We are down a meaningful amount measured in Australian dollars, which reflects the rapid fall of the Australian dollar in March (flattering our results) and the rapid rise since (hurting our results). Really we are, broadly speaking, flat – but flat in a market in which everyone else was getting rich.

If we were doctors, we would observe that we followed the Hippocratic Oath: “first do no harm”. But we would then tartly observe that we did no good either.

A comment on where we are with markets

Our bearish positioning is informed by our view that markets, particularly the US market, are historically expensive. We could be wrong in this view, so let’s explore it.

Bulls will point out that the price-to-earnings (PE) ratio of the US market is well within historic norms. Sure, they say, we have an above-average PE ratio—but it was much higher in (say) the tech bubble and at other market tops. Moreover, the market is supported by historically low interest rates and easy monetary policy.

Interest rates are indeed low. If you believe that interest rates stay at zero forever then stocks whose earnings are unlikely to decline much (such as say The Coca Cola Company) should be valued at very high PE ratios.

But there’s the rub: businesses whose earnings are not going to decline much deserve such a valuation. Looking from the top down reveals the risk.

We think – instinctively – that the aggregate earnings capacity of US business is at risk.

It is trite to say that income inequality is at very high (even historically high) levels in the USA. That is obvious to all and is a fundamental driver of American politics.

It is also obvious to say that the proportion of GDP taken in taxes – especially taxes on business is at a historic low. The US was running massive deficits even in 2019’s very good economy.

The corollary is that profit share is at historic highs, indeed, astonishing highs. Almost everywhere you look in the US you see companies that earn more than you would expect. Our personal favorite is Lamb Weston, which makes wholesale potato chips (fries to Americans) delivered to restaurants that wind up on your plate/hips. The 2019 operating margin of Lamb Weston is almost 18 percent. The operating margin of Apple, by comparison, is under 25 percent. The idea that a company whose sole job is to buy potatoes from farmers, chop them up, freeze them and deliver them to restaurants can earn margins even close to Apple is astonishing.

But what we see for Lamb Weston we see right across American society.

The American market is at above-average multiples of massively-above-average profits. Competition should usually drive down profit share, and democratic politics has – at least in theory and cyclically – some kind of redistributive effect.

If you ask us the risk to US profits is to the downside. We are far more worried about the earnings than the price-to-earnings ratio. Weak earnings (post COVID) should be sufficient to push the market down.

Ways in which we are wrong on this

The main problem with this argument is that inequality continues to increase and profit share (absent this virus) continues to rise. Privately we made the argument a few years ago that profit share was at a massive multi-generational high – but then profit share rose further. At least part of that was the government deliberately reducing the tax take on profits under the guise of “tax reform”. But profit share seems to rise for reasons independent of that as well.

Warren Buffett has been wrong on this too. In a famous article in 1999 Buffett made the argument that the stock market was expensive. He argued that after-tax profits as a percent of GDP were unlikely to exceed the 1929 high and that people projecting high rates of profit growth for decades were wrong. To quote:

[In dismissing the argument that corporate profitability in relation to GDP must rise.] You know, someone once told me that New York has more lawyers than people. I think that’s the same fellow who thinks profits will become larger than GDP. When you begin to expect the growth of a component factor to forever outpace that of the aggregate, you get into certain mathematical problems. In my opinion, you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%. One thing keeping the percentage down will be competition, which is alive and well. In addition, there’s a public-policy point: If corporate investors, in aggregate, are going to eat an ever-growing portion of the American economic pie, some other group will have to settle for a smaller portion. That would justifiably raise political problems–and in my view a major reslicing of the pie just isn’t going to happen.

The money quote – from Warren Buffett of course is that:

… you have to be wildly optimistic to believe that corporate profits as a percent of GDP can, for any sustained period, hold much above 6%.

Warren was wrong. After tax profits have remained above 6 percent of GDP for some time. He (incorrectly) thought that competition would fix that.

He also argued that democracy would ultimately fix that even if the competition wouldn’t. Politics he thought would not accept endlessly rising income inequality. He was wrong on that too.

Lack of competition as the way we are wrong

The most obvious way that we are wrong is that Warren Buffett assumes (and we implicitly assume) that competition will drive down profit share. One counter-argument is that US industry is increasingly dominated by companies against whom it is very hard to compete. For example, how do you compete with Google?

We have tried to immunize ourselves against a fall in profit share (a fall that has not come) by seeking out and owning companies that are very hard to compete against.

But competition hasn’t worked generally. How else do you explain Lamb Weston’s astonishing profitability? Our friend Jonathan Tepper wrote a book on why, with one of the key reasons being the abrogation of any government responsibility to police competition. Tepper argues that industry consolidation has gone too far. Deciding he can’t change the debate, he has started a fund manager to exploit these competition reductions.

We will be watching Prevatt Capital closely but, to be fair, we still do not understand why someone hasn’t tried to compete and earn super-normal margins processing potato chips.

The virus and being wrong

More pertinently the response to the virus has been for the US market to go straight up. We think this is silly but – as per usual – we sought out people on the other side of the trade. It is pretty clear that profits are going to be down hard this year, though bulls argue profits are going to be up sharply in the future. The virus, they contend, is extremely income-inequality exacerbating. Originally the virus was a problem of rich people who travel and people who hung around with rich people who travelled. The virus skewed up-market and people called it a great equalizer.

That did not last. Upper income people are able to social-distance and often work from home. They have resources. The poor (especially in America) are forced to work and cannot socially distance. They live closer together too. In Australia the biggest outbreaks are in low-end government-supplied housing in Victoria. In America the virus also skews poor.

Some bulls we have discussed this with argue that coming out of this the increased inequality will persist. The poor will be even more poor and marginalized, and, given resistance to government mandated health programs, they also think a vaccine when one comes will have lower compliance. The poor will be diseased too.

That sounds terrible but they then argue it is a good thing. Income inequality will be permanently higher. Corporate profit share will go up. Buy stocks.

Given the market moves it is hard to argue against.

The other argument for buying stocks right now

The other main argument for buying stocks right now is that inflation is coming. The Fed and other central banks are printing amounts of money that are simply jaw-dropping. The argument is that this will result in inflation and so you better start owning real assets immediately because nominal assets are going to be smashed. In this world you buy Coca Cola (because it has pricing power) and highly indebted companies (because their debts will be wiped out) but avoid owning banks.

We are (emphatically) not macro-economists so this argument is harder for us to dismiss. Moreover, while some segments of the market support this idea (e.g. the gold price has been strong), others have rejected it sharply (e.g., ten-year bond yields under 0.7% do not portend imminent inflation).

The gold argument was widely heard after the financial crisis, when almost every hedge fund manager we admire was bullish gold and believed in inflation. The gold price went to USD1800 per ounce, stayed high for about two years, yet the inflation never came. Gold lost a third of its value. Whether the argument is right or wrong this time remains to be seen. We remain short gold-mining frauds, but we have hedged our net gold position to a much larger extent than historically as we are worried about this argument.

Our test of whether we are right

We are particularly expert at finding scummy stocks with small market caps ($100 million to $1 billion) pushed by people with less than salubrious records. It is the core to our short book.

Such themes have included:

- crappy gold stocks exaggerating their deposits

- crappy Chinese companies claiming massive businesses in China via fake accounts

- crappy shale oil stocks exaggerating their deposits

- crappy biotech stocks with non-viable cures for obscure medical conditions

- crappy marijuana stocks run by serial stock promoters claiming to successfully “brand” weed or to develop condition-specific medical marijuana

There is always a bull market going on somewhere in crappy stocks. Even at the height of the financial crisis there was a bull market in gold-stock frauds.

We can lose badly on a crappy short if it goes from 10 to zero via 100. Bull markets in crappy stocks can cost us (meaning you) money even if we are right.

So we have always managed the risk by keeping individual stock exposure low and diversifying the sectors. We have almost always found somewhere to be short where, eventually, we are making money. And usually we can find a sector where we do not even have to wait very long.

On US exchanges, though, this time is different: every category of scummy stocks is rising simultaneously. This is treacherous for us, and requires us to be extraordinarily careful managing risk.

Such broad-based enthusiasm for dross is also a measure as to whether the market is rationally expensive or crazy. If inflation were the driver there wouldn’t be a generalized bubble in crazy stocks, just very high prices for companies like Coca Cola that can increase their prices when inflation comes. But when there is a crazy-strong market for genuinely drossy stocks we conclude the market is just high.

Just how tough is it for our strategy?

We are short a diversified pile of crappy stocks. Our job is to find every rotten egg in the world and short a little bit of each of them. On the short book we will make mistakes. We will for instance accidentally short a good egg. More likely we will short a bad company and it will announce a (fake) cure for COVID-19 and the stock will go up a lot and we will lose money even if the stock eventually collapses. But, if diversified enough, this should even out over time. We manage our short book so we can handle (but not enjoy) a market where the worst stocks have rallied hardest. But we still do not like periods where “crap flies”.

But, as noted above, almost every category of scummy stock is going up simultaneously and that is truly difficult for us. We are okay – as we said, doing no harm – but on a day-to-day basis it feels like something is thumping us every day. And at least on the short book, there is nowhere to hide. (With a few salubrious exceptions.)

Biotech alas has to get singled out for special mention. As we have said before biotech is the scammiest sector of all. It makes Perth-based small cap gold mining stocks promoted at Gold Coast investment conferences (to pick an Australian example) look entirely righteous and honest.

We short biotech stocks based not on the science predominantly, but on the people. There are people in the industry with a twenty-year history of hyping stocks for money. When they hype stocks again we short the company. We are short literally dozens of biotechnology stocks all the time, and on average it works, but regularly enough one comes up with a big announcement (for example something that might work on a rare disease and make them a lot of money). The stocks invariably go for a wild ride. And as long as our position is small enough it tends not to worry us.

These days however it is really easy to hype a biotech stock. Just say you have something that might work for COVID-19. That is usually good for a 50-100 percent move in the stock and we have seen some 600 percent moves. Alas – and this was an artefact of our process – we were short, ex-ante, many small cap stocks that announced a substantial COVID-19 breakthrough. This isn’t luck. It is easier to say you have a COVID-19 breakthrough than to actually have one – and the management of these companies have a history of aggressive promotion. But, from the perspective of a short-seller, it hasn’t been pleasant. And we at least have to allow for the possibility that one of these companies might have a COVID-19 breakthrough. It is unlikely, but good things sometimes happen to bad people. It is more likely though that they will continue to hype false breakthroughs, and from a risk management perspective that also has to be dealt with.

Historic parallels

This appears to be the most extreme “crap flies” market we have seen in our professional career. But our early life had a sharper example: in the latter period of dot-com. In the dot-com boom it got to the point that real tech companies that made actual money were valued lower than the ones whose only metrics were “eyeballs.” While profits could be measured, pre-revenue companies allowed the holder to fantasize about the money that they might make in the future.

It was more extreme in Australia. At least American technology investors had some real companies from which to choose. Australia tech stocks were, for the large part and to use a stock market technical term, steaming piles of horse manure.

This was when Simon met John on a stock chat board called “The Chimes.” We mostly wondered in disbelief about the valuations being put on now-obscure Australian technology stocks.

You will need an encyclopedic knowledge of Australian stock promotes from the dot-com era to remember these, but they had names like Davnet, Spike Networks, Cape Range Wireless, Liberty One and Voicenet. The quality end included names like Sausage Software and Solution 6. Many other names we promptly forgot.

At the very high-quality end were companies like One-Tel that at least had a real wireless system and lots of customers. Their slogan was “You’ll tell your friends about One Tel” to which John appended “after you read the accounts”.

Anyway, more or less every day these stocks went up. And the Chimes was (mostly) full of sensible fellows and what John might now call cheap-suited value investors. We did not participate. And to a (very limited) extent we short-sold some of the more nonsense names. And our results whilst adequate would not have been adequate as a professional fund manager. It would have been very hard to maintain clients whilst underperforming a rampant bull market. We were sensible, it worked alright in the end, but it was not saleable as a funds management product.

As the stocks eventually collapsed, we made jokes about it. Liberty One fell and fell. When it hit a dollar we asked “what price Liberty” for which the answer was “one dollar”. Later we asked what price Liberty – but it was gone. You couldn’t buy Liberty for any money, but the liquidator would sell you the ashes.

We should have done better though. These were nonsense and we knew that they were nonsense. Fortunately, we were not short in size when they went up, or we would have been badly hurt. But while we joked about the price of Liberty, we did not short it on the way down, which was a failing we do not wish to repeat.

Today, the biotech end of the market, and some of the promotional gold stocks, and some tech stocks, and some China names are as bad as the stocks on which we learnt our trade on that long-lost stock chat board. And so we are doing a little thinking about that historic parallel.

This led us to a book, Kate Askew’s history of the era titled Dot.Bomb Australia: How we wrangled, conned and argie-bargied our way into the new digital universe. The book details the crazy market where the crappiest stocks (including most of the ones mentioned) barged their way into the collective consciousness. Simon and I watched it real time – but we had forgotten both the intensity of the bubble and the time-frame over which it took place. And the collective amount of wealth generated on the way up. The future Australian Prime Minister (Malcolm Turnbull) got rich backing Ozemail, the Australian equivalent of America Online. It was sold (for cash) to WorldCom. The past New South Wales Premier Neville Wran benefited from the same transaction. Former Prime Minister Paul Keating became a multi-millionaire by backing Lake Technology, another company that has disappeared into obscurity.

The bull market of course went on for a very long time. It was a time in which our then private portfolios underperformed.

Eventually, it came undone. Ultimately there is an infinite supply of stock and an infinite supply of new crappy companies. If selling fraud works well, people will sell more of it. And more still. And that is why the shorts work in the end.

Even reading Kate Askew’s book it is hard to tell whether this market is quite as crazy as say 1999 Australian small cap technology.

Managing your portfolio, not our business

When John and Simon started Bronte, the explicit goal was to manage clients’ money as if it were our own and as if it were all the wealth we would ever have. We would not chase bubbles because everyone else did, and we would not care about relative performance when it was not sensible to care about relative performance.

In 1999 what John and Simon were doing on The Chimes was sensible, but it was not saleable. It worked okay in the end without ever being exciting. Chasing relative performance can create in fund management a conflict between what is best for the clients’ portfolio and what is best for the manager’s business. We put your portfolio first, and we appreciate you entrusting us with it.

That said, it is not without risk. What scares us most is a market where all crappy stocks rise at the same time, across sectors. Then our diversification won’t help us as much.

Even in a well-diversified short book, things can go wrong. Wirecard, for example, didn’t go wrong all at once but it cost us considerable money over a decade and was a drag on performance. It was a winner last quarter, but that was small consolation.

Wirecard stock – the biggest loser in the history of our firm

Wirecard was a payments processor for transactions that PayPal would not clear. That really meant online gambling and pornography. The company had its origins as a merchant card processor for companies that found it difficult to find merchant card providers.

There is some jargon here so we should explain.

In a credit card transaction there are three broad things going on:

a) A card issuer gives credit cards to individuals (for example the National Australia Bank Visa card in my pocket) and takes credit risk against this card. If I default, NAB wears it.

b) A merchant acquirer gives a terminal to a person selling things. They do not take credit risk but they do have some regulatory/compliance risks discussed below.

c) Interchange happens where the fee on the credit card transaction (typically about 1.8 percent of the value transacted) is divided between the issuer bank, the merchant bank and interchange.

The vast majority of transaction revenue typically goes to the issuer bank, as they accept the main risk (credit losses). The division would typically be something like 1.7 percent to the issuer bank, 0.09 percent to the merchant bank and 0.01 percent to fund the costs of the interchange (paid mostly to Visa).

Merchant acquiring is not a very lucrative business, but it is normally a low-risk business. The main risk is that a credit card terminal is used to deliberately run through a bunch of fraudulent or questionable transactions.

That said there are a few types of higher-risk merchant businesses around: those with fraud risk or those likely to receive regulatory scrutiny.

You might be wary for instance of giving credit card terminals to prostitutes because they may run cards through it with the wrong price on it. And it is very hard to verify the transaction took place and the price that was agreed.

But two online businesses stand out as ultra-high-risk clients:

- Online gambling

- Pornography

PayPal for example will not clear funds for either of these activities.

Online gambling was difficult because it was criminal for American citizens and almost everyone who touched it wound up with problems with US regulatory authorities. If you later intended to do US business, it was an area to avoid.

Wirecard’s first business of any size was being a high-risk merchant acquirer. This can be a profitable business because pornographers and the like will pay up for getting access to the credit card network – and fees of 8-10 percent of total amounts cleared are possible. One argument in support of Wirecard’s above-normal profitability was that it worked with sketchy, high-risk merchants.

It’s hard to play in the mud without getting a bit dirty; from just its clientele, we had some suspicions that Wirecard stock was itself sketchy. We then worked out (and confirmed) that an acquisition that they did in Indonesia barely existed. Our thesis (confirmed multiple ways) was that Wirecard profits were (wildly) overstated and that the fake profits were generating fake cash. This fake cash was spent on fake acquisitions.

For a long time Wirecard stock was our largest short. We were oversize because it was a German company, and at the time we had many German longs and very few German shorts so oversizing the position looked sensible from a portfolio management perspective.

Anyway the Wirecard fraud got bigger and bigger and – frankly – more outrageous. The whole thing has now been covered extensively in the Financial Times. But the company and the German regulators eventually decided that short-sellers were conspiring to spread lies about Wirecard and drive the stock down. The German securities regulator (BaFin) even criminally charged two journalists from the Financial Times as well as some short-sellers. One short-seller was convicted and jailed for saying things about Wirecard that were in retrospect shown to be accurate.

The risk of bogus criminal charges for telling the truth about Wirecard was enough reason for us to remain silent as to our views. We never talked widely about the position. The rumor mill (accurately) reported some short-sellers were violently attacked. Kidnapping threats were real.

What was just an interesting German fraud became one of the great battleground stocks of the decade. Being risk-averse people, getting involved in Wirecard was a scrap that we wanted to avoid.

Wirecard stock collapsed this quarter. Approximate two billion Euro is missing, but the truth is that it never existed: that two billion euro was the artefact of previously booked fake profit. The CEO (Markus Braun) has been arrested. The Chief Operating Officer (Jan Marsalek) has disappeared. Airline records say he went through the Philippines, but airport camera records supposedly suggest that he never went through the airport.

Eventually we made a bit on the short. But we will never recover our prior losses.

Over the past decade Wirecard stock declined from 8 Euro per share to complete disgrace via 191 Euro. We talk in meetings with clients about frauds on which we are right going from 10 to zero via 100, and unfortunately this discussion is not theoretical. In such cases we are forced to cover to manage our risk, and we will lose money even if we are right.

You can’t see the Wirecard stock losses in the past decade’s results – but we assure you that they are there. Wirecard is our bête-noir stock, our biggest loser. A loser on which we were eventually right.

If our positions were larger, we could have been permanently impaired by a disaster like Wirecard. We were not because of decent risk management.

Worse, there is likely another Wirecard somewhere in our collection of 200+ shorts, a position that will cost us (meaning you) decent money but on which we are right. Risk management is key to what we do with shorts. We will not compromise on it.

Persisting in the strategy

At the end of the last quarter we were bearish, and we would have liked to be short, but there was no obvious way to hedge the situation if we were wrong. Option volatility was expensive, and we looked for, but did not find, cheap optionality with which to cover the possibility we were wrong.

The situation is similar now. We are distinctly bearish, and we would like to be short. But there is no obvious way to hedge the situation if we are wrong. Option volatility remains expensive. We are as close to neutral as we can be. And again (and this phrase haunts us) if the market continues to rally, we will feel like we have missed out.

We are willing however to change our mind. If, for example, we determine inflation is inevitable we may wind up much longer and full of companies who – like Coca Cola – have inflation resistant businesses.

There is a decent risk that the market continues to rally and our results remain poor. But we will manage your money as we promised – as if it were the only money we will ever have. We will do things that are sensible.

And yes, we will have flat to poor periods again, sad to say. And we will lose money on individual stocks too, like Wirecard, despite our disciplined approach to shorts. But we will remain sensible and longer-term oriented, and we hope you continue to trust us to do that.

John, Simon and the Bronte team.

See the full commentary here.

This article first appeared on ValueWalk Premium.

The post Bronte Amalthea Fund 2Q20 Commentary: WIrecard Stock appeared first on ValueWalk.