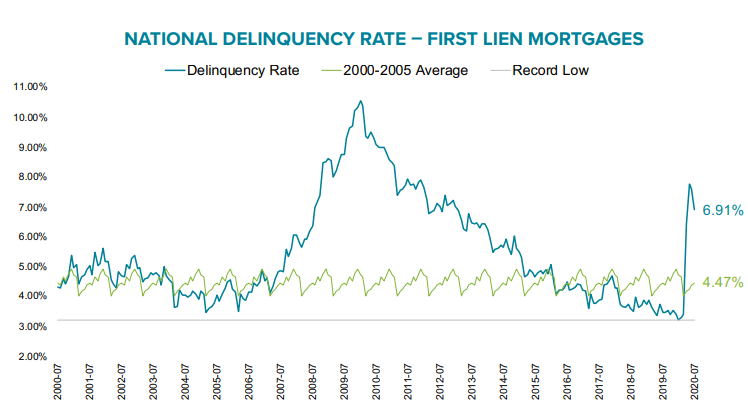

This gives a total of 7.40% delinquent or in foreclosure.

Today, the Data & Analytics division of Black Knight, Inc. released its latest Mortgage Monitor Report, based upon the company’s industry-leading mortgage performance, housing and public records datasets. This month, Black Knight looked at both Q2 2020 origination data as well as interest rate locks thus far in Q3 2020 to get a sense of how the lending market has fared in the era of COVID-19. As Black Knight Data & Analytics President Ben Graboske explained, a period of record-low interest rates has provided a much-needed backstop to the impact of shutdowns, unemployment and economic uncertainty.

“Despite the nation being under pandemic-related lockdowns for much of the quarter, a record-breaking surge in mortgage originations occurred in Q2 2020, driven by the record-low interest rate environment,” said Graboske. “Nearly $1.1 trillion in first lien mortgages were originated in Q2 2020, which is the largest quarterly origination volume we’ve seen since first reporting on the metric in January 2000. Refinance lending grew more than 60% from the previous quarter and more than 200% from the same time last year, accounting for nearly 70% of all Q2 originations by dollar value. At the same time, purchase lending declined 8% year-over-year as the traditional spring homebuying season was impacted by COVID-19-related restrictions. However, mortgage loan rate lock data – a leading indicator of lending activity – suggests that the homebuying season was simply pushed forward into the third quarter.

“Purchase locks in Q3 2020 have already made up for the losses of a COVID-impacted Q2 – and then some – based upon normal seasonal expectations. In fact, rate locks are suggesting that we could see Q3 purchase lending break typical seasonal trends and rise by 30-40%, which would push us to a new record high. Likewise, while Q2 refinance activity was record-breaking, refi lock data suggests Q3 refinance volumes could climb even higher. Locks on refinance loans expected to close in the third quarter, assuming a 45-day lock-to-close timeline, are already up 20% from Q2. With market conditions as they are and given the recent delay of the 50 basis points fee on GSE refinances until December, we would expect near-record low interest rates to continue to buoy the market. After all, there are still nearly 18 million homeowners with good credit and at least 20% equity who stand to cut at least 0.75% off their current first lien rate by refinancing.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.

This graph from Black Knight shows the surge in first lien originations in Q2.

From Black Knight:

Nearly $1.1T in first lien mortgages were originated in Q2 2020, the largest quarterly origination volume on record since Black Knight began reporting the metric in January 2000

• The surge in lending was driven by record-low interest rates fueling a flurry of refinance activity

• Refinance lending was up more than 60% from Q1 2020 and more than 200% from the same time last year, accounting for nearly 70% of all first lien originations by dollar value, as compared to 39% in Q2 2019

• Despite significant impacts from the pandemic – most acutely felt in May’s closing volumes – purchase lending was only down 8% from the year prior

And here is a graph from the Mortgage Monitor that shows the National Delinquency Rate.

And here is a graph from the Mortgage Monitor that shows the National Delinquency Rate.

From Black Knight:

• Overall mortgage delinquencies fell by nearly 9% in July, pushing the national delinquency rate down to 6.9%

• While this represents significant improvement, there are still nearly 2M more borrowers delinquent on mortgage payments than there were in February prior to the impacts of COVID-19

• At 860K, 30-day delinquencies have fallen 14% below their pre-pandemic levels, suggesting that the initial wave of COVID-19-related delinquencies has subsided

There is much more in the mortgage monitor.