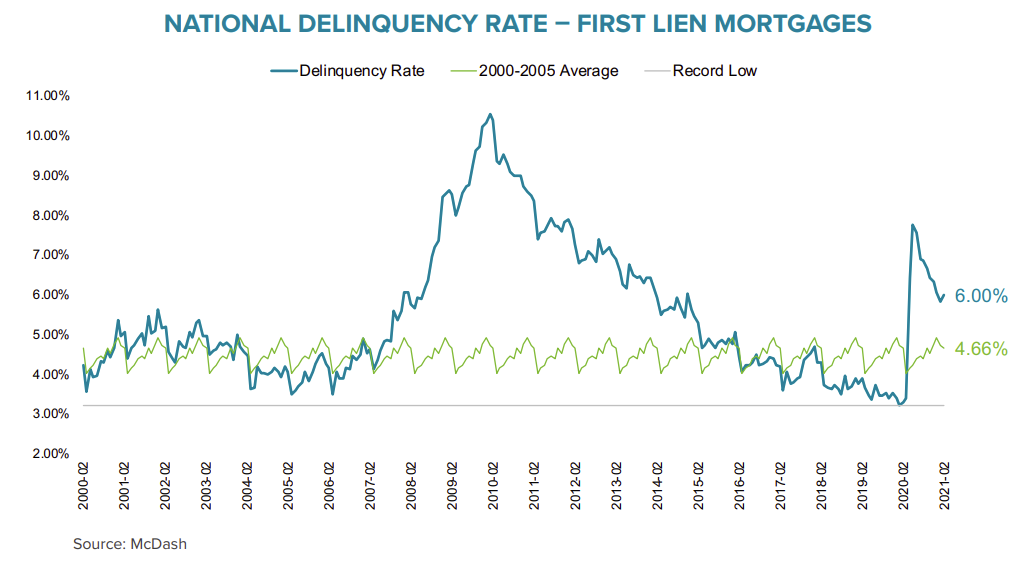

This gives a total of 6.32% delinquent or in foreclosure.

Today, the Data & Analytics division of Black Knight, Inc. released its latest Mortgage Monitor Report, based upon the company’s industry-leading mortgage, real estate and public records datasets. This month, with the U.S. housing market remaining extremely hot by any historical measure, the report looks at home price appreciation over the past year and how that’s impacted affordability. According to Black Knight Data & Analytics President Ben Graboske, incredibly low levels of for-sale inventory, coupled with still historically low interest rates, continue to put upward pressure on home prices and tighten affordability.

“Our repeat sales-based Black Knight Home Price Index shows February’s annual price appreciation at 11.6%, the fastest growth rate in more than 15 years,” said Graboske. “Likewise, the daily home sales data tracked by our Collateral Analytics group found a nearly 16% year-over-year increase in the median sales price in February. Multiple years of constrained housing inventory and historically low interest rates have helped fuel this fire to the point where nearly 75% of the 100 largest U.S. markets have seen annual home price growth of 10% or higher. What’s more, Collateral Analytics’ Market Conditions Report shows the housing markets in 75% of ZIP codes rated either ‘Strong’ or ‘Hot’ based on underlying market metrics. Only 7% are characterized as ‘Normal.’

“Of course, upward pressure on home prices has also served to tighten affordability, and with rates on the rise, affordability concerns are coming into sharper relief. It now takes 20% of the median income to make the monthly payment on the purchase of an average-priced home, back up to the five-year average after several years of low interest rates mitigating the impact of rising prices on affordability. Housing is now the least affordable it’s been – factoring in interest rates, home prices and income – since mid-2019. Any hopes of 2021 bringing an influx of homes to the market and lessening pressure on prices appear to be dashed for now, as new for-sale listings were down 16% and 21% year-over-year in January and February, respectively. Rather than an influx of homes on the market, we’re now 125,000 fewer new listings in the hole compared to the first two months of 2020 and trending in the wrong direction. With higher interest rates and a continuing shortage of inventory, it will be important to keep a careful eye on both home prices and affordability metrics in the coming months.”

emphasis added

Click on graph for larger image.

Click on graph for larger image.

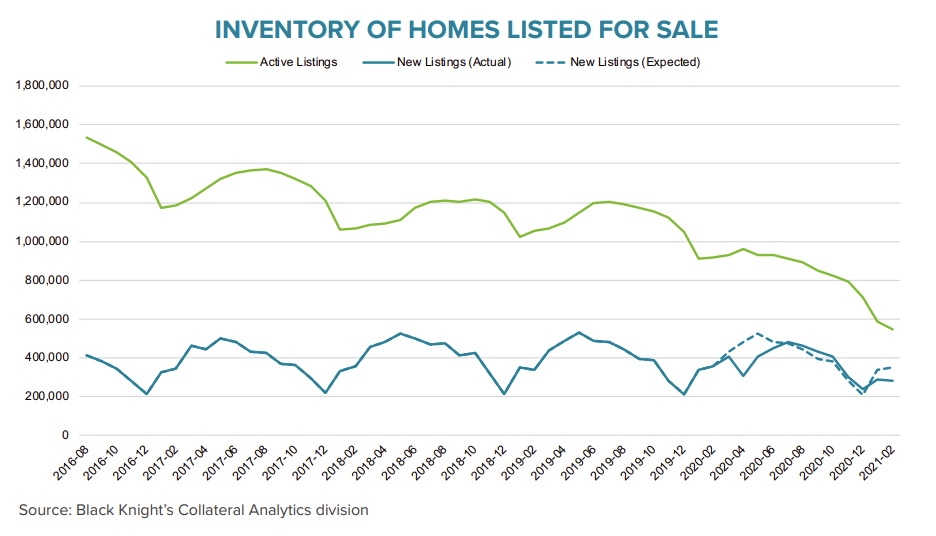

Here is a graph from the Mortgage Monitor that shows Active Inventory and New Listings.

From Black Knight:

• Entering 2021, the number of homes listed for sale was down 32% year-over-year and had fallen to its lowest level on record, according to Black Knight’s Collateral Analytics division

• The hopes that early 2021 would bring much-needed inflow of inventory to a market starved for supply have been dashed so far, with new listing volumes coming in well below pre-pandemic levels

• In fact, the number of homes listed for sale in January was down 16% from the year prior, while new listings in February were down 21%

• Rather than an influx, we now have 125K fewer listings than over the first two months of 2020 and are trending in the wrong direction with inventory down 40% year-over-year

And on delinquencies from Black Knight:

And on delinquencies from Black Knight:

• After eight consecutive months of improvement, the national mortgage delinquency rate rose in February from 5.85% to 6.0%

• Delinquency rate increases were seen broadly across portfolios, geographies and asset classes

• Despite the rise, 30-day delinquencies remain 19% below pre-pandemic levels, while there are still 5X (+1.7M) as many 90-day delinquencies as there were in February 2020

There is much more in the mortgage monitor.