Whitney Tilson’s email to investors discussing Berkshire Hathaway’s second-quarter earnings; it feels like deja vu all over again; it may be time for bank stocks to trade higher; the lowest-ever u.s. junk bond yield; your worst 1%.

Q2 2020 hedge fund letters, conferences and more

Berkshire Hathaway’s Second-Quarter Earnings

1) My longtime friend and former partner, Glenn Tongue, is the ax on Berkshire Hathaway (BRK-B).

So, as I do every quarter, I asked if he’d share his thoughts on Berkshire Hathaway’s second-quarter earnings report (here are links to the press release and 10-Q). Here’s what Glenn sent me:

Berkshire Hathaway reported second-quarter earnings on Saturday morning. Given the global effects of COVID-19, there was surprisingly little action of note during the quarter.

One of the headline items was that the company repurchased $5.1 billion of its stock during the quarter. While not huge in the context of Berkshire’s $508 billion market cap and its cash balances of $143 billion, it was by far the biggest quarterly repurchase ever, more than double the $2 billion in the fourth quarter of last year.

Given that CEO Warren Buffett didn’t have the company repurchase any of its stock in March, when it hit a multi-year low under $240,000, or April, as the stock market rallied, it’s noteworthy that he got more aggressive in May and June. Buffett’s bullishness regarding his own stock appears to have continued subsequent to the end of the quarter, as it appears that the company repurchased an additional $2.4 billion of stock in July.

Berkshire was a large net seller of stocks during the second quarter, purchasing only $800 million of equity securities while selling $13.6 billion. While we don’t yet know for sure what was sold during the quarter, Buffett reported in May that he sold all of Berkshire’s airline holdings in April. Other equity sales appear to have come from some of the many bank stocks Berkshire owns, though Buffett in recent weeks (starting on July 20) has invested more than $2 billion in Bank of America (BAC), adding to Berkshire’s already-large position. One enormously bright spot for the company was the performance of its largest position by far, Apple (AAPL), which soared 43% during the quarter.

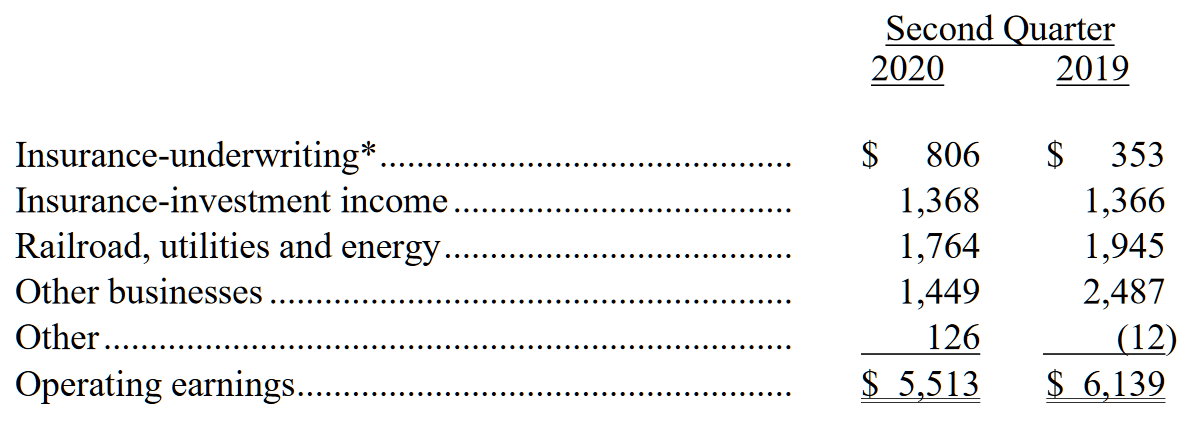

Berkshire Hathaway’s total operating earnings in the second quarter fell 10% year over year, from $6.1 billion to $5.5 billion. This is not surprising, given the broad-based global slowdown resulting from COVID-19. Here is the breakdown by segment (in millions):

Berkshire’s stock has declined 6% year to date versus a 3.4% gain for the S&P 500 Index, a disparity that I think is unwarranted. While Berkshire did not take advantage of the opportunities that the market presented in March to the degree that I would have hoped, the company is incredibly safe, has solid growth prospects, and the stock is cheap.

I agree with your estimate, Whitney, from your July 16 e-mail that Berkshire’s intrinsic value, conservatively calculated, is $386,000 per A share, 21% above current levels.

Thank you, Glenn!

Deja Vu: Buffett and Berkshire

2) Another longtime friend, Doug Kass of Seabreeze Partners, also weighed in on Buffett and Berkshire:

It Feels Like Deja Vu All Over Again

The rising criticism of Warren Buffett is hilarious, foolish, and has an historic precedent

Late into the dot-com boom, in the second half of 1999, Warren Buffett was universally criticized for his lack of exposure in high-growth technology stocks and for his concentration on banks and consumer non-durable companies.

Warren got the last laugh, as he is likely to again in the upcoming market cycle.

Of course the current critics (many who should really know better) fail to mention that Berkshire’s investment in Apple only a few years ago was the largest by far on a cost basis in the company’s history. Berkshire currently owns 251 million shares at a cost of about $140/share ($35 billion). This equates to an unrealized gain of over $75 billion – marked to market.

I would end by stating that Buffett’s net worth is above $70 billion – and that is after making large charitable contributions of his shares – making him the fourth-wealthiest person in the world.

Again, the criticism – especially from those trading cryptocurrency miner Marathon Patent Group (MARA), Chinese electric vehicle maker Kandi Technologies Group (KNDI), and the rest of the shiny objects admired by speculators – is laughable and is testimony to the state of the market and to the opinions from those in the cheap seats who think they know more than the smartest long-term investor in history.

Bank Stocks Are Very Attractive

3) Sharing another of Doug’s recent missives, I agree with him that bank stocks are very attractive here and I own seven of them in my personal account:

It May Be Time for Bank Stocks to Trade Higher and Break Out of the Recent Trading Range

-

- 2Q2020 may have represented a peak build in loan loss provisions and a peak in relative underperformance of bank industry share prices

- I share Warren Buffett’s confidence in the banking space

Bank stocks have underperformed the broader market by nearly 3,500 basis points in 2020 as credit costs associated with the COVID-19 shutdowns have weighed on the group.

I have argued that the industry’s capital bases (and substantial liquidity from, among other things, remarkable year-over-year deposit growth), coupled with continuing core earnings growth, are exceptionally strong and adequate to digest and absorb continued, but moderating, credit losses.

I continue to believe in this case, and so does The Oracle of Omaha, who recently added to his already-large Bank of America (BAC) holdings.

For several months I have suggested that while the current rate and credit pressures and uncertainties would weigh on bank stocks, the intermediate-term outlook was quite strong.

However, with the differential in performance (mentioned above) and with growing consensus of economic expectations, valuations have grown much more compelling over the near term and there is growing evidence that the worst of the credit experience may be behind the industry – following the large and conservative second quarter reserve builds.

Second quarter banking industry results underscored my view that non-interest (fee-based) income represents an increasing proportion of the sector’s profits. So despite ever-lower interest rates and a flattening yield curve, the adverse impact on profitability is less than many believe.

Markets respond to rates of change and importantly, and in all likelihood (and based on recent bank disclosures), second quarter loan reserve builds may have represented cycle highs as most banks are getting closer to loan loss reserve adequacy.

Position: Long C (large), WFC (large), BAC (large), JPM (large)

Thank you, Doug!

4) This blurb by Bloomberg columnist Matt Levine resonated with me.

The Art of Playing Defense

5) Picking up where I left off in yesterday’s e-mail, with another excerpt from my upcoming book, The Art of Playing Defense:

Your Worst 1%

It’s important to understand that you aren’t judged for the way you behave 90% or even 95% of the time, but rather on your worst 1% – or even 0.01%.

To my knowledge, David Sokol had never done anything unethical in his long career before his fateful purchase of Lubrizol’s stock ruined him. That’s all it took.

I made thousands of trades in my two decades as a hedge-fund manager that were, to my knowledge, all ethical and proper, but if even one hadn’t been, I could have been ruined as well.

One misjudgment is all it takes, so it’s critical to avoid gray areas. Never go near the line. Be ultra-conservative when it comes to your integrity and reputation.

This applies in every area of life. You can be a kind and generous person almost all of the time, but if you make one blatantly racist or sexist remark (even if you’re not racist or sexist), that’s how you will be remembered.

Even if you’ve been faithful to your spouse for decades, if you go to Vegas one weekend, get drunk, and have a one-night stand, you’ve likely wrecked your marriage forever in a single night.

Once you understand this, the implications should be sobering. Everyone makes mistakes, but in some areas, you simply can’t afford to make any.

There are many things you can do to avoid this kind of calamity. First, mistakes are far more likely if you’re sleep deprived or under physical, mental, or financial duress so, if at all possible, avoid taking important actions or making big decisions during these times.

Be careful who you associate with, both personally and professionally. Their behavior and reputation will rub off on you and vice versa.

And never assume that something is private or off the record. Other than perhaps the most intimate conversations with your closest friends and family, assume that everything you write and say is being recorded and could be made public. E-mails, in particular, live forever, so it’s best to assume that someday they will be read by a hostile journalist, regulator, investigator, or lawyer. It’s happened to me a few times and it’s no fun.

Best regards,

Whitney

The post Berkshire Hathaway’s Second-Quarter Earnings appeared first on ValueWalk.