From the AIA: Architectural billings in August still show little sign of improvement

Business conditions remained stalled at architecture firms during August as demand for design services continued to decline, according to a new report from the American Institute of Architects (AIA).

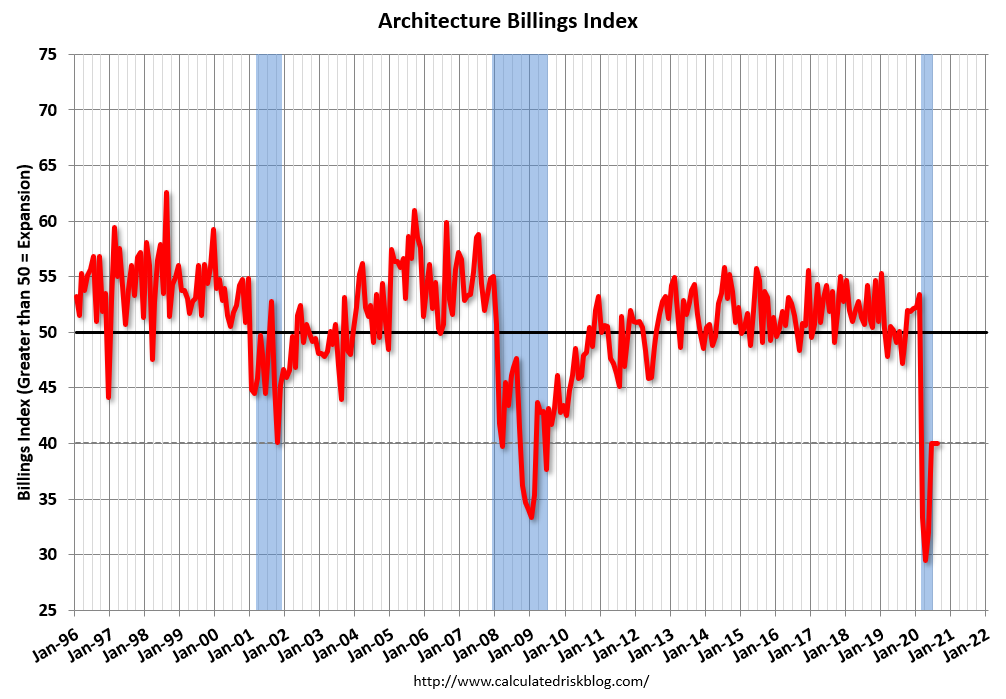

The pace of decline during August remained at about the same level as in July and June, posting an Architecture Billings Index (ABI) score of 40.0 (any score below 50 indicates a decline in firm billings). Inquiries into new projects during August grew for the first time since February, and the value of new design contracts increased to a score of 46.0. As a result, fewer firms reported a decline in August, despite the fact that they remained negative overall.

“Unfortunately, since the start of the COVID-19 pandemic, many architecture firms are finding fewer inquiries that convert to billable projects,” said AIA Chief Economist, Kermit Baker, Hon. AIA, PhD. “While fewer firms reported declining billings in August than during the early months of the COVID-19 pandemic, the fact that the score has been unchanged for the last three months shows that the recovery from this downturn is not progressing at the pace we had hoped to see.”

…

• Regional averages: Midwest (41.7); South (41.6); West (41.3); Northeast (33.9)• Sector index breakdown: multi-family residential (49.4); mixed practice (41.9); institutional (40.2); commercial/industrial (35.5)

emphasis added

Click on graph for larger image.

Click on graph for larger image.

This graph shows the Architecture Billings Index since 1996. The index was at 40.0 in August, unchanged from 40.0 in July. Anything below 50 indicates contraction in demand for architects’ services.

Note: This includes commercial and industrial facilities like hotels and office buildings, multi-family residential, as well as schools, hospitals and other institutions.

This index has been below 50 for six consecutive months. This represents a significant decrease in design services, and suggests a decline in CRE investment through the first half of 2021 (This usually leads CRE investment by 9 to 12 months).

This weakness is not surprising since certain segments of CRE are struggling, especially offices and retail.