This was well above consensus expectations, and this was the highest sales rate since 2007. Clearly low mortgages rates, and low sales in March and April (due to the pandemic) have led to a bounce back in sales in May and June (and probably in July).

New home sales are counted when the contract is signed, whereas existing home sales are counted when the transaction closes. So new home sales performed better than existing home sales in May and June (on a year-over-year basis). Based on mortgage applications and regional pending home sales reports, there will be a further pickup in existing home sales in July, and builder reports suggest there will probably be a further pickup in new home sales too.

Important: No one should get too excited. Many years ago, I wrote several article about how new home sales and housing starts (especially single family starts) were some of the best leading indicators for the economy. However, I’ve noted that there are times when this isn’t true. NOW is one of those times.

Currently the course of the economy will be determined by the course of the virus, and New Home Sales tell us nothing about the future of the pandemic. Without the pandemic, I’d be very positive about this report.

The longer the pandemic lasts, the more long term damage to the economy – and, if the pandemic worsens and persists – that will eventually negatively impact housing. The outlook for housing depends on the outlook for the pandemic.

Earlier: New Home Sales increased to 776,000 Annual Rate in June.

Click on graph for larger image.

Click on graph for larger image.

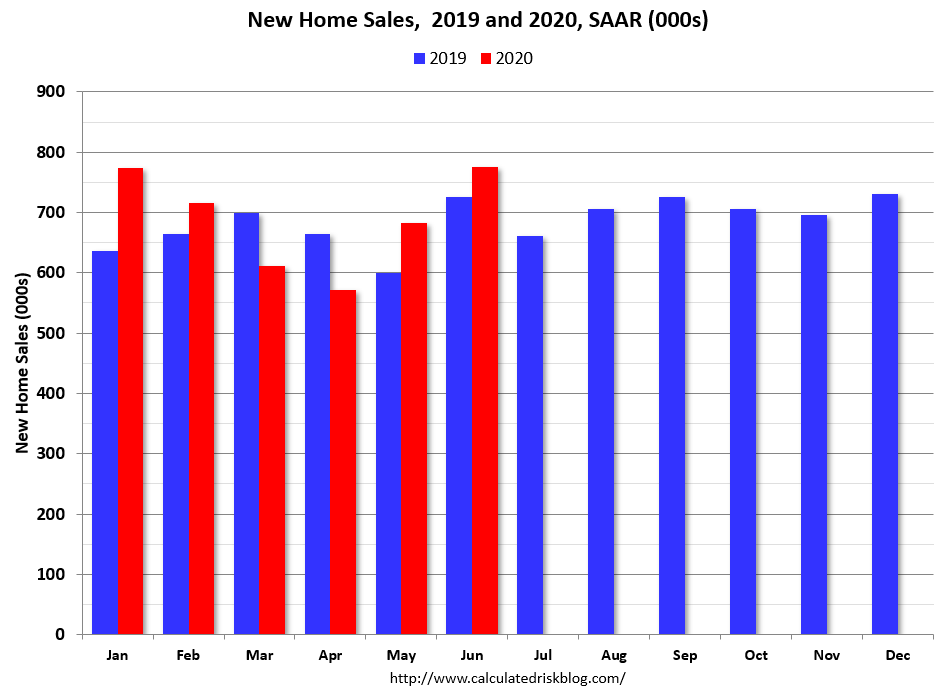

This graph shows new home sales for 2019 and 2020 by month (Seasonally Adjusted Annual Rate).

New home sales were up 6.9% year-over-year (YoY) in June. Year-to-date (YTD) sales are up 3.2%.

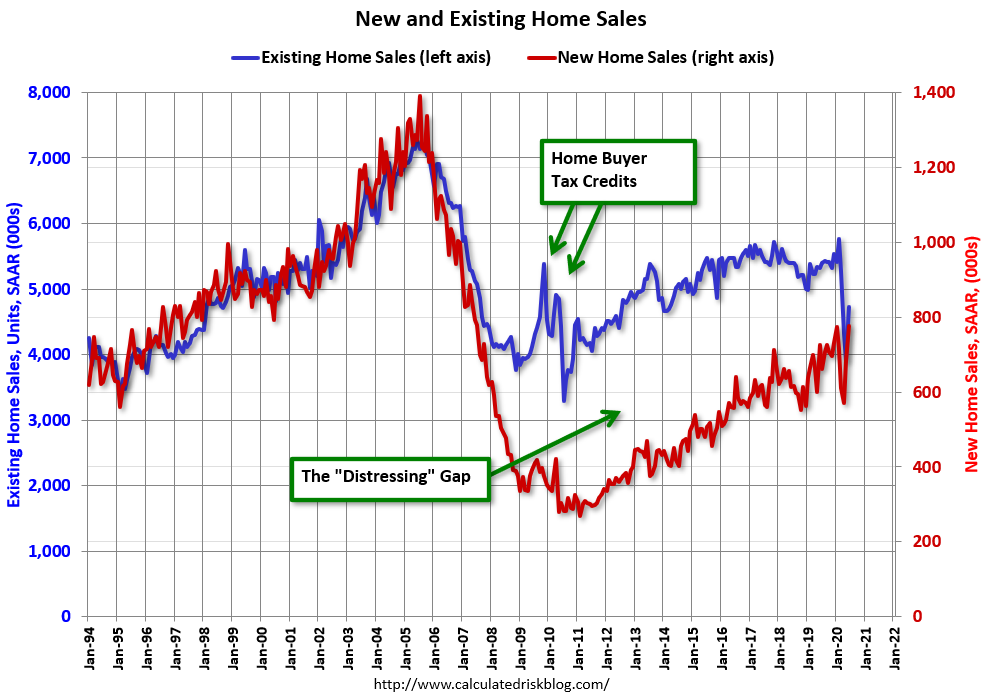

And here is another update to the “distressing gap” graph that I first started posting a number of years ago to show the emerging gap caused by distressed sales.

The “distressing gap” graph shows existing home sales (left axis) and new home sales (right axis) through June 2020. This graph starts in 1994, but the relationship had been fairly steady back to the ’60s.

The “distressing gap” graph shows existing home sales (left axis) and new home sales (right axis) through June 2020. This graph starts in 1994, but the relationship had been fairly steady back to the ’60s.

Following the housing bubble and bust, the “distressing gap” appeared mostly because of distressed sales.

Now the gap is mostly closed (with help from the pandemic).

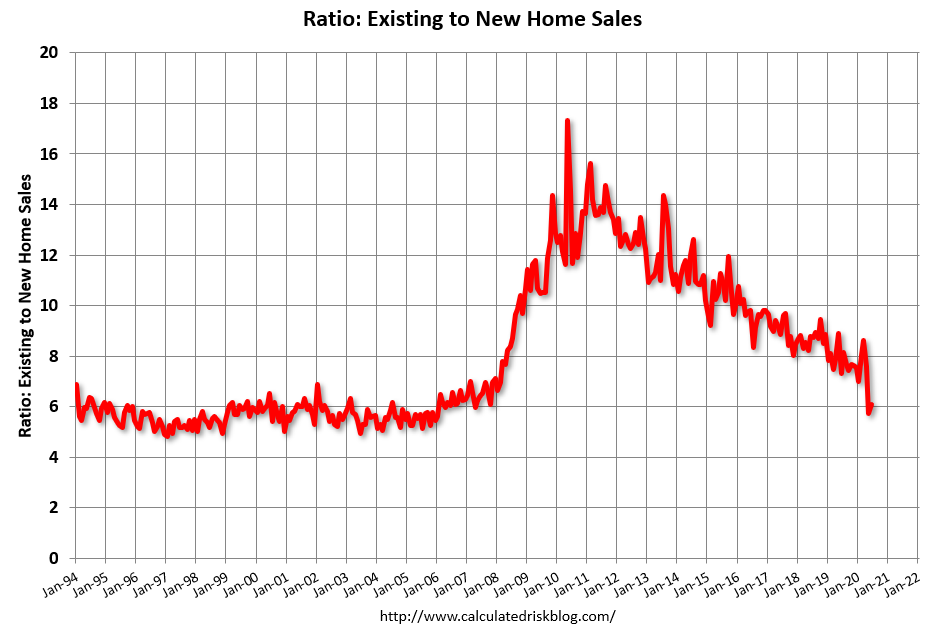

Another way to look at this is a ratio of existing to new home sales.

Another way to look at this is a ratio of existing to new home sales.

This ratio was fairly stable from 1994 through 2006, and then the flood of distressed sales kept the number of existing home sales elevated and depressed new home sales. (Note: This ratio was fairly stable back to the early ’70s, but I only have annual data for the earlier years).

In general the ratio has been trending down since the housing bust – and was close to the historical ratio before the pandemic.

Note: Existing home sales are counted when transactions are closed, and new home sales are counted when contracts are signed. So the timing of sales is different.