“Inflation is not going to be transitory,” the chief economic adviser at Allianz SE said in an interview on Bloomberg TV’s The Open show … “I have a whole list of companies that have announced price increases, that have told us they expect further price increases, and that they expect them to stick,” El-Erian said.

First, transitory doesn’t mean that price increases won’t “stick”. It means that year-over-year (YoY) inflation will decline back to the Fed’s target of 2%.

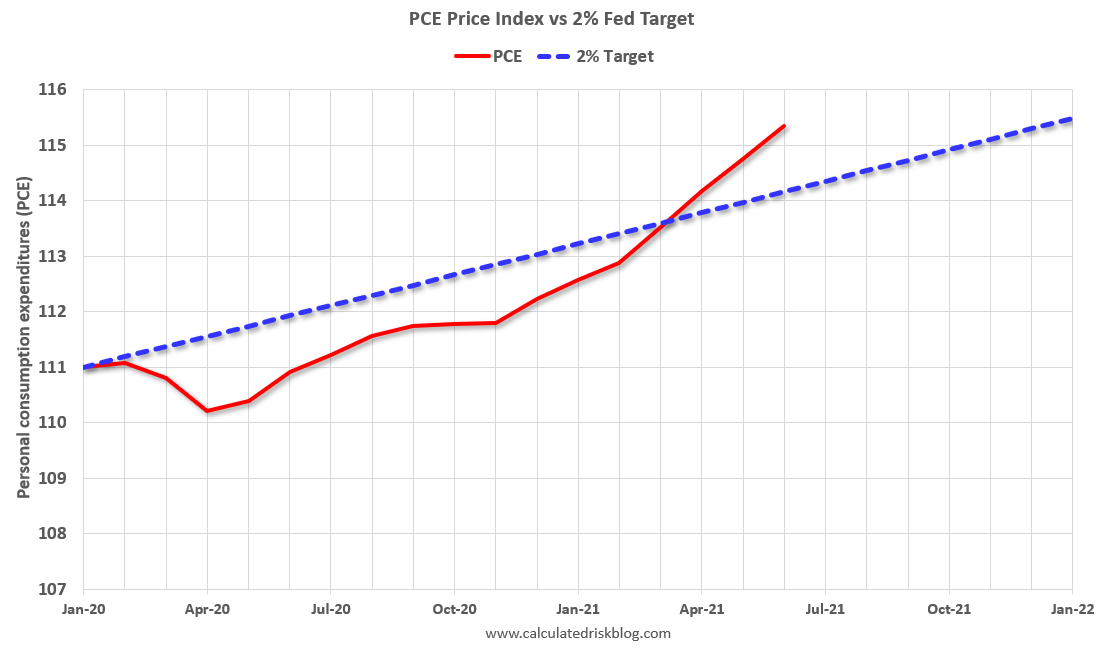

The first graph shows the PCE price index since January 2020 (before the pandemic), and the dashed blue line is the Fed’s target of 2%.

Click on graph for larger image.

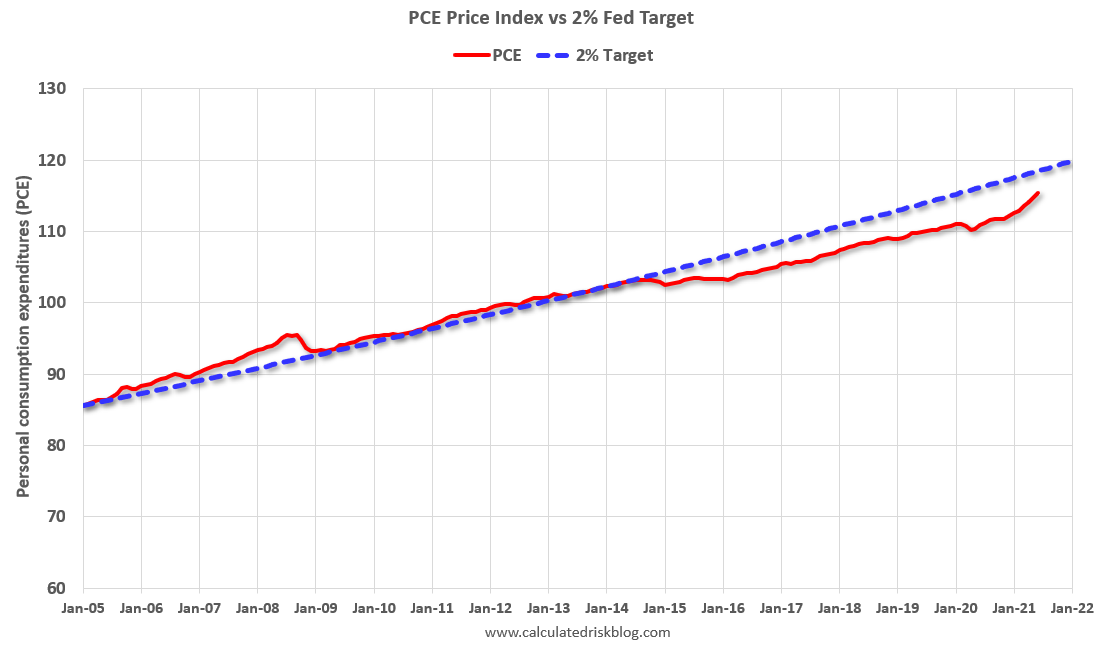

Click on graph for larger image.

As I’ve mentioned before, there was some deflation at the beginning of the pandemic, and this has increased the YoY change (base effect). There is some transitory inflation from supply chain issues, and surging rents will probably push up Owners Equivalent Rent (OER) over the next year.

The second graph is from January 2005 (just an arbitrary date).

The second graph is from January 2005 (just an arbitrary date).

This shows that inflation has been below target for years. If we were doing price targeting (we aren’t) we would be looking for more price increases.

The graphs for core PCE inflation show the same pattern.

The question is not will some prices “stick”, but rather will YoY inflation ease back towards the Fed’s target? Or will inflation stay at the current 4.0% (PCE YoY in June)?

My sense is inflation will ease back towards the Fed’s target.